library(tidyverse)

library(tidymodels)

tidymodels_prefer()

library(kernlab)

library(mlbench)

library(caret)

library(knitr)

library(ggcorrplot)

library(skimr)

library(GGally)

library(finetune)

library(lubridate)

library(baguette)

library(patchwork)

library(discrim)

library(reticulate)

library(usemodels)

library(doParallel)

library(naivebayes)

theme_set(theme_bw())Bank Marketing

Introduction

The data is sourced from the UCI ML Repository and can be downloaded here. It is related to the direct marketing campaigns of a Portuguese banking institution. The campaigns were based on phone calls. Multiple datasets are provided, however this analysis focuses on the full dataset (bank-addidtional-full.csv), which is also the latest and has the most number of inputs.

Goal

The classification goal is to predict if the client will subscribe (yes/no) a term deposit (variable y).

Data Dictionary

| Attribute Name | Type | Description |

|---|---|---|

| age | numeric | age of the person called |

| job | categorical | type of job |

| marital status | categorical | married, single or unknown |

| education | categorical | educational attainment |

| default | categorical | has credit in default? |

| housing | categorical | has housing loan? |

| loan | categorical | has personal loan? |

| contact | categorical | contact communication type |

| month | categorical | last contact month of year |

| day_of_week | categorical | last contact day of week |

| duration | numeric | last contact duration in seconds. The duration is not known before the call, so even though this has a strong impact on outcome (duration=0 => y=0), it should be discarded from the model |

| campaign | numeric | number of contacts performed during this campaign for this client (includes last contact) |

| pdays | numeric | number of days passed since client was contacted since the client was last contacted from a previous campaign. 999 means not previously contacted |

| previous | numeric | number of contacts performed during this campaign for this client |

| poutcome | categorical | outcome of the previous marketing campaign |

| emp.var.rate | numeric | employment variation rate - quarterly indicator |

| cons.price.idx | numeric | consumer price index - monthly indicator |

| cons.conf.idx | numeric | consumer confidence index - monthly indicator |

| euribor3m | numeric | euribor 3 month rate - daily indicator. These are European interest rates. |

| nr.employed | numeric | number of employees - quarterly indicator |

| y | categorical | has the client subscribed a term deposit? |

Load Packages

import pandas as pd

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

import sklearn.metrics as metrics

import IPython.display as dsp

from IPython.display import HTML

from sklearn.model_selection import train_test_split

from sklearn.preprocessing import MinMaxScaler, FunctionTransformer, PolynomialFeatures, OneHotEncoder, PowerTransformer, LabelEncoder

from sklearn.compose import ColumnTransformer

from sklearn.pipeline import Pipeline

from sklearn.pipeline import make_pipeline

from sklearn.neighbors import KNeighborsClassifier

from sklearn.svm import SVC

from sklearn.linear_model import LogisticRegression, LogisticRegressionCV, ElasticNet, SGDClassifier, Perceptron

from sklearn.model_selection import cross_val_score, GridSearchCV, KFold, StratifiedKFold, RandomizedSearchCV

from sklearn.calibration import CalibratedClassifierCV

from sklearn.feature_selection import VarianceThreshold

from sklearn.naive_bayes import GaussianNB

from xgboost import XGBClassifier

sns.set_theme()

import warnings

warnings.filterwarnings('ignore')using CSV

using DataFrames

using DataFramesMeta

using CategoricalArrays

using MLJ

using MLJLinearModels

using StatsBase

using BenchmarkTools

using Statistics

using StatsPlots

using PrettyTablesLoad Data

data_bank_marketing = read_csv2("./data/bank-additional/bank-additional-full.csv")data_bank_marketing = pd.read_csv("./data/bank-additional/bank-additional-full.csv", sep=";")data = CSV.read("./data/bank-additional/bank-additional-full.csv", DataFrame);Sample 10 rows

#knitr::kable(as_tibble(head(data_bank_marketing, n=10)))

set.seed(42)

knitr::kable(slice_sample(data_bank_marketing, n=10))| age | job | marital | education | default | housing | loan | contact | month | day_of_week | duration | campaign | pdays | previous | poutcome | emp.var.rate | cons.price.idx | cons.conf.idx | euribor3m | nr.employed | y |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 23 | blue-collar | married | basic.9y | no | yes | no | cellular | may | wed | 52 | 4 | 999 | 0 | nonexistent | -18 | 92893 | -462 | 1.281 | 50991 | no |

| 45 | admin. | married | basic.9y | unknown | yes | no | telephone | jun | thu | 60 | 1 | 999 | 0 | nonexistent | 14 | 94465 | -418 | 4.866 | 52281 | no |

| 41 | technician | single | university.degree | no | no | no | cellular | jul | thu | 537 | 2 | 999 | 0 | nonexistent | 14 | 93918 | -427 | 4.962 | 52281 | no |

| 31 | blue-collar | single | unknown | no | yes | no | telephone | may | fri | 273 | 2 | 999 | 0 | nonexistent | 11 | 93994 | -364 | 4.864 | 5191 | no |

| 36 | technician | single | professional.course | no | no | no | cellular | jun | fri | 146 | 2 | 999 | 0 | nonexistent | -29 | 92963 | -408 | 1.268 | 50762 | yes |

| 50 | blue-collar | married | basic.4y | unknown | yes | yes | telephone | jun | fri | 144 | 15 | 999 | 0 | nonexistent | 14 | 94465 | -418 | 4.967 | 52281 | no |

| 28 | technician | married | basic.9y | no | yes | no | cellular | may | wed | 224 | 1 | 999 | 1 | failure | -18 | 92893 | -462 | 1.281 | 50991 | no |

| 32 | admin. | single | university.degree | no | no | no | cellular | jul | thu | 792 | 1 | 999 | 0 | nonexistent | 14 | 93918 | -427 | 4.963 | 52281 | no |

| 59 | retired | divorced | basic.4y | no | no | yes | cellular | jul | mon | 210 | 3 | 999 | 2 | failure | -17 | 94215 | -403 | 0.827 | 49916 | yes |

| 35 | technician | married | professional.course | no | no | no | cellular | apr | wed | 225 | 2 | 999 | 0 | nonexistent | -18 | 93075 | -471 | 1.415 | 50991 | no |

pd.set_option('display.width', 500)

#pd.set_option('precision', 3)

sample=data_bank_marketing.sample(10)

dsp.Markdown(sample.to_markdown(index=False))| age | job | marital | education | default | housing | loan | contact | month | day_of_week | duration | campaign | pdays | previous | poutcome | emp.var.rate | cons.price.idx | cons.conf.idx | euribor3m | nr.employed | y |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 45 | admin. | single | high.school | no | no | no | telephone | jun | wed | 192 | 6 | 999 | 0 | nonexistent | 1.4 | 94.465 | -41.8 | 4.864 | 5228.1 | no |

| 66 | retired | married | basic.4y | no | yes | yes | telephone | aug | wed | 82 | 3 | 999 | 3 | failure | -2.9 | 92.201 | -31.4 | 0.854 | 5076.2 | no |

| 33 | management | single | university.degree | no | unknown | unknown | cellular | jun | tue | 73 | 1 | 999 | 0 | nonexistent | -2.9 | 92.963 | -40.8 | 1.262 | 5076.2 | no |

| 40 | blue-collar | married | basic.4y | unknown | unknown | unknown | telephone | jul | wed | 135 | 1 | 999 | 0 | nonexistent | 1.4 | 93.918 | -42.7 | 4.962 | 5228.1 | no |

| 43 | services | divorced | professional.course | no | no | no | cellular | may | fri | 196 | 2 | 999 | 0 | nonexistent | -1.8 | 92.893 | -46.2 | 1.313 | 5099.1 | no |

| 36 | blue-collar | married | basic.6y | no | no | no | telephone | may | fri | 189 | 2 | 999 | 0 | nonexistent | 1.1 | 93.994 | -36.4 | 4.857 | 5191 | no |

| 23 | student | single | high.school | no | no | no | cellular | jun | wed | 200 | 2 | 999 | 0 | nonexistent | -2.9 | 92.963 | -40.8 | 1.26 | 5076.2 | yes |

| 27 | technician | single | professional.course | no | no | no | telephone | jun | fri | 112 | 5 | 999 | 0 | nonexistent | 1.4 | 94.465 | -41.8 | 4.967 | 5228.1 | no |

| 32 | technician | married | university.degree | no | yes | no | telephone | jul | wed | 196 | 1 | 999 | 0 | nonexistent | 1.4 | 93.918 | -42.7 | 4.962 | 5228.1 | no |

| 31 | admin. | single | high.school | no | yes | no | cellular | may | thu | 1094 | 2 | 999 | 0 | nonexistent | -1.8 | 92.893 | -46.2 | 1.266 | 5099.1 | yes |

data[1:10,:]10×21 DataFrame

Row │ age job marital education default housing lo ⋯

│ Int64 String15 String15 String31 String7 String7 St ⋯

─────┼──────────────────────────────────────────────────────────────────────────

1 │ 56 housemaid married basic.4y no no no ⋯

2 │ 57 services married high.school unknown no no

3 │ 37 services married high.school no yes no

4 │ 40 admin. married basic.6y no no no

5 │ 56 services married high.school no no ye ⋯

6 │ 45 services married basic.9y unknown no no

7 │ 59 admin. married professional.course no no no

8 │ 41 blue-collar married unknown unknown no no

9 │ 24 technician single professional.course no yes no ⋯

10 │ 25 services single high.school no yes no

15 columns omittedpretty_table(data[1:10,:])┌───────┬─────────────┬──────────┬─────────────────────┬─────────┬─────────┬─────────┬───────────┬─────────┬─────────────┬──────────┬──────────┬───────┬──────────┬─────────────┬──────────────┬────────────────┬───────────────┬───────────┬─────────────┬─────────┐

│ age │ job │ marital │ education │ default │ housing │ loan │ contact │ month │ day_of_week │ duration │ campaign │ pdays │ previous │ poutcome │ emp.var.rate │ cons.price.idx │ cons.conf.idx │ euribor3m │ nr.employed │ y │

│ Int64 │ String15 │ String15 │ String31 │ String7 │ String7 │ String7 │ String15 │ String3 │ String3 │ Int64 │ Int64 │ Int64 │ Int64 │ String15 │ Float64 │ Float64 │ Float64 │ Float64 │ Float64 │ String3 │

├───────┼─────────────┼──────────┼─────────────────────┼─────────┼─────────┼─────────┼───────────┼─────────┼─────────────┼──────────┼──────────┼───────┼──────────┼─────────────┼──────────────┼────────────────┼───────────────┼───────────┼─────────────┼─────────┤

│ 56 │ housemaid │ married │ basic.4y │ no │ no │ no │ telephone │ may │ mon │ 261 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 57 │ services │ married │ high.school │ unknown │ no │ no │ telephone │ may │ mon │ 149 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 37 │ services │ married │ high.school │ no │ yes │ no │ telephone │ may │ mon │ 226 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 40 │ admin. │ married │ basic.6y │ no │ no │ no │ telephone │ may │ mon │ 151 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 56 │ services │ married │ high.school │ no │ no │ yes │ telephone │ may │ mon │ 307 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 45 │ services │ married │ basic.9y │ unknown │ no │ no │ telephone │ may │ mon │ 198 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 59 │ admin. │ married │ professional.course │ no │ no │ no │ telephone │ may │ mon │ 139 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 41 │ blue-collar │ married │ unknown │ unknown │ no │ no │ telephone │ may │ mon │ 217 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 24 │ technician │ single │ professional.course │ no │ yes │ no │ telephone │ may │ mon │ 380 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

│ 25 │ services │ single │ high.school │ no │ yes │ no │ telephone │ may │ mon │ 50 │ 1 │ 999 │ 0 │ nonexistent │ 1.1 │ 93.994 │ -36.4 │ 4.857 │ 5191.0 │ no │

└───────┴─────────────┴──────────┴─────────────────────┴─────────┴─────────┴─────────┴───────────┴─────────┴─────────────┴──────────┴──────────┴───────┴──────────┴─────────────┴──────────────┴────────────────┴───────────────┴───────────┴─────────────┴─────────┘show((data[1:10,:] |> DataFrames.DataFrame), allrows=true, allcols=true ) 10×21 DataFrame

Row │ age job marital education default housing loan contact month day_of_week duration campaign pdays previous poutcome emp.var.rate cons.price.idx cons.conf.idx euribor3m nr.employed y

│ Int64 String15 String15 String31 String7 String7 String7 String15 String3 String3 Int64 Int64 Int64 Int64 String15 Float64 Float64 Float64 Float64 Float64 String3

─────┼───────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────────

1 │ 56 housemaid married basic.4y no no no telephone may mon 261 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

2 │ 57 services married high.school unknown no no telephone may mon 149 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

3 │ 37 services married high.school no yes no telephone may mon 226 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

4 │ 40 admin. married basic.6y no no no telephone may mon 151 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

5 │ 56 services married high.school no no yes telephone may mon 307 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

6 │ 45 services married basic.9y unknown no no telephone may mon 198 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

7 │ 59 admin. married professional.course no no no telephone may mon 139 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

8 │ 41 blue-collar married unknown unknown no no telephone may mon 217 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

9 │ 24 technician single professional.course no yes no telephone may mon 380 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

10 │ 25 services single high.school no yes no telephone may mon 50 1 999 0 nonexistent 1.1 93.994 -36.4 4.857 5191.0 no

Correlations

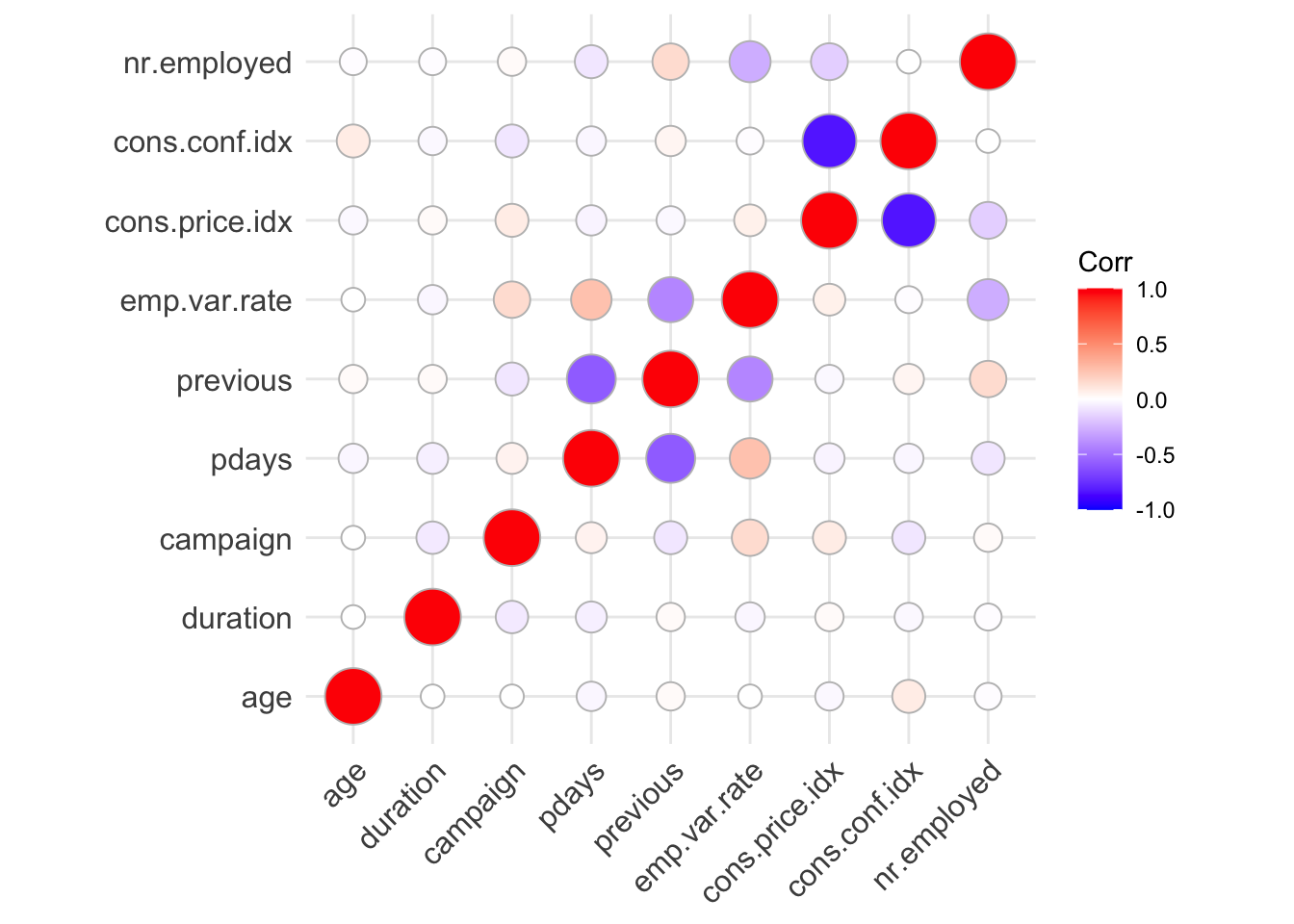

correlations = cor(data_numeric)

knitr::kable(as.data.frame(correlations))| age | duration | campaign | pdays | previous | emp.var.rate | cons.price.idx | cons.conf.idx | nr.employed | |

|---|---|---|---|---|---|---|---|---|---|

| age | 1.0000000 | -0.0008657 | 0.0045936 | -0.0343690 | 0.0243647 | 0.0048933 | -0.0194012 | 0.0803944 | -0.0148194 |

| duration | -0.0008657 | 1.0000000 | -0.0716992 | -0.0475770 | 0.0206404 | -0.0253914 | 0.0204889 | -0.0180911 | -0.0145367 |

| campaign | 0.0045936 | -0.0716992 | 1.0000000 | 0.0525836 | -0.0791415 | 0.1510747 | 0.0759259 | -0.0769437 | 0.0153579 |

| pdays | -0.0343690 | -0.0475770 | 0.0525836 | 1.0000000 | -0.5875139 | 0.2643170 | -0.0426908 | -0.0347775 | -0.0798846 |

| previous | 0.0243647 | 0.0206404 | -0.0791415 | -0.5875139 | 1.0000000 | -0.4169615 | -0.0230420 | 0.0385344 | 0.1494358 |

| emp.var.rate | 0.0048933 | -0.0253914 | 0.1510747 | 0.2643170 | -0.4169615 | 1.0000000 | 0.0552787 | -0.0061387 | -0.2773105 |

| cons.price.idx | -0.0194012 | 0.0204889 | 0.0759259 | -0.0426908 | -0.0230420 | 0.0552787 | 1.0000000 | -0.8435170 | -0.1617969 |

| cons.conf.idx | 0.0803944 | -0.0180911 | -0.0769437 | -0.0347775 | 0.0385344 | -0.0061387 | -0.8435170 | 1.0000000 | -0.0039613 |

| nr.employed | -0.0148194 | -0.0145367 | 0.0153579 | -0.0798846 | 0.1494358 | -0.2773105 | -0.1617969 | -0.0039613 | 1.0000000 |

ggcorrplot(correlations, method="circle")

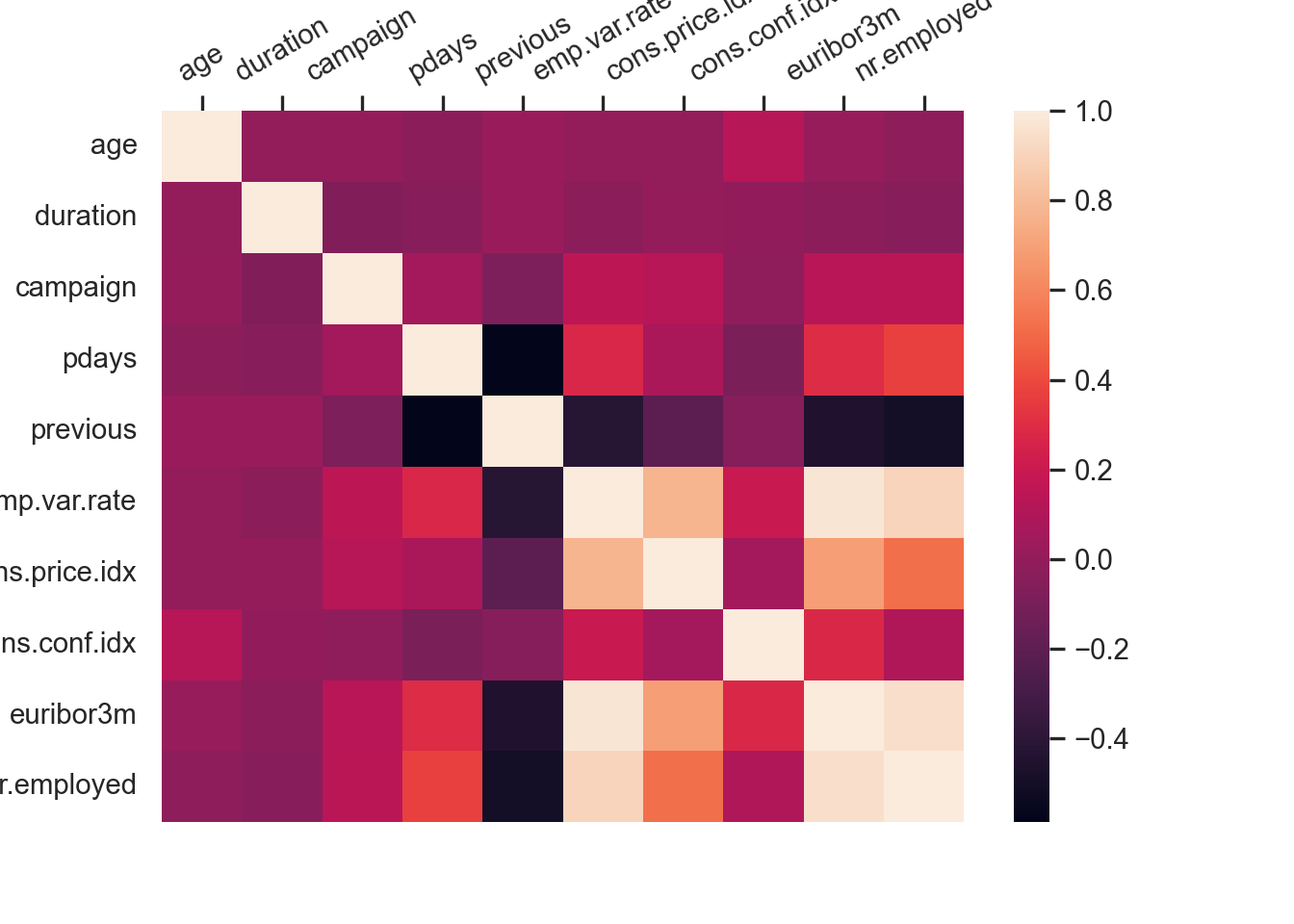

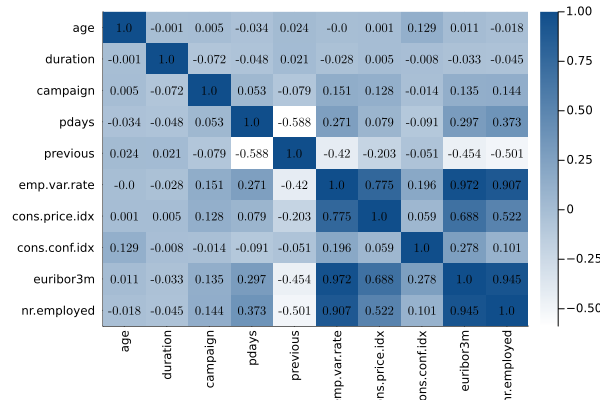

correlations = data_bank_marketing.select_dtypes(include=np.number).corr(method='pearson')

with pd.option_context('display.max_columns', 40):

print(correlations) age duration campaign pdays previous emp.var.rate cons.price.idx cons.conf.idx euribor3m nr.employed

age 1.000000 -0.000866 0.004594 -0.034369 0.024365 -0.000371 0.000857 0.129372 0.010767 -0.017725

duration -0.000866 1.000000 -0.071699 -0.047577 0.020640 -0.027968 0.005312 -0.008173 -0.032897 -0.044703

campaign 0.004594 -0.071699 1.000000 0.052584 -0.079141 0.150754 0.127836 -0.013733 0.135133 0.144095

pdays -0.034369 -0.047577 0.052584 1.000000 -0.587514 0.271004 0.078889 -0.091342 0.296899 0.372605

previous 0.024365 0.020640 -0.079141 -0.587514 1.000000 -0.420489 -0.203130 -0.050936 -0.454494 -0.501333

emp.var.rate -0.000371 -0.027968 0.150754 0.271004 -0.420489 1.000000 0.775334 0.196041 0.972245 0.906970

cons.price.idx 0.000857 0.005312 0.127836 0.078889 -0.203130 0.775334 1.000000 0.058986 0.688230 0.522034

cons.conf.idx 0.129372 -0.008173 -0.013733 -0.091342 -0.050936 0.196041 0.058986 1.000000 0.277686 0.100513

euribor3m 0.010767 -0.032897 0.135133 0.296899 -0.454494 0.972245 0.688230 0.277686 1.000000 0.945154

nr.employed -0.017725 -0.044703 0.144095 0.372605 -0.501333 0.906970 0.522034 0.100513 0.945154 1.000000names = data_bank_marketing.select_dtypes(include=np.number).columns.values.tolist()

hmap=sns.heatmap(correlations,

xticklabels=correlations.columns,

yticklabels=correlations.columns)

hmap.xaxis.tick_top()

plt.xticks(rotation=30)(array([0.5, 1.5, 2.5, 3.5, 4.5, 5.5, 6.5, 7.5, 8.5, 9.5]), [Text(0.5, 1, 'age'), Text(1.5, 1, 'duration'), Text(2.5, 1, 'campaign'), Text(3.5, 1, 'pdays'), Text(4.5, 1, 'previous'), Text(5.5, 1, 'emp.var.rate'), Text(6.5, 1, 'cons.price.idx'), Text(7.5, 1, 'cons.conf.idx'), Text(8.5, 1, 'euribor3m'), Text(9.5, 1, 'nr.employed')])plt.show()

function cor_df(df::DataFrame)

numeric_cols = names(df, Real)

M=Matrix(data[!,numeric_cols])

C=cor(M)

cols=reshape(numeric_cols, 1, (length(numeric_cols)))

(n,m) = size(C)

hm=heatmap(C, fc=cgrad([:white,:dodgerblue4]), xticks=(1:m,numeric_cols), xrot=90, yticks=(1:m,numeric_cols), yflip=true, show = true)

annotate!([(j, i, text(round(C[i,j],digits=3), 8,"Computer Modern",:black)) for i in 1:n for j in 1:m])

return (hm, DataFrame(vcat(cols,C), :auto))

endcor_df (generic function with 1 method)

hm,corr=cor_df(data)(Plot{Plots.GRBackend() n=1}, 11×10 DataFrame

Row │ x1 x2 x3 x4 x5 x6 ⋯

│ Any Any Any Any Any Any ⋯

─────┼──────────────────────────────────────────────────────────────────────────

1 │ age duration campaign pdays previous emp.var ⋯

2 │ 1.0 -0.000865705 0.00459358 -0.034369 0.0243647 -0.0003

3 │ -0.000865705 1.0 -0.0716992 -0.047577 0.0206404 -0.0279

4 │ 0.00459358 -0.0716992 1.0 0.0525836 -0.0791415 0.15075

5 │ -0.034369 -0.047577 0.0525836 1.0 -0.587514 0.27100 ⋯

6 │ 0.0243647 0.0206404 -0.0791415 -0.587514 1.0 -0.4204

7 │ -0.000370685 -0.0279679 0.150754 0.271004 -0.420489 1.0

8 │ 0.000856715 0.00531227 0.127836 0.0788891 -0.20313 0.77533

9 │ 0.129372 -0.00817287 -0.0137331 -0.0913424 -0.0509364 0.19604 ⋯

10 │ 0.0107674 -0.0328967 0.135133 0.296899 -0.454494 0.97224

11 │ -0.0177251 -0.0447032 0.144095 0.372605 -0.501333 0.90697

5 columns omitted)display(hm)

Observations

- There is a negative correlation between cons.conf.idx and cons.price.idx

Numeric Attributes

Age

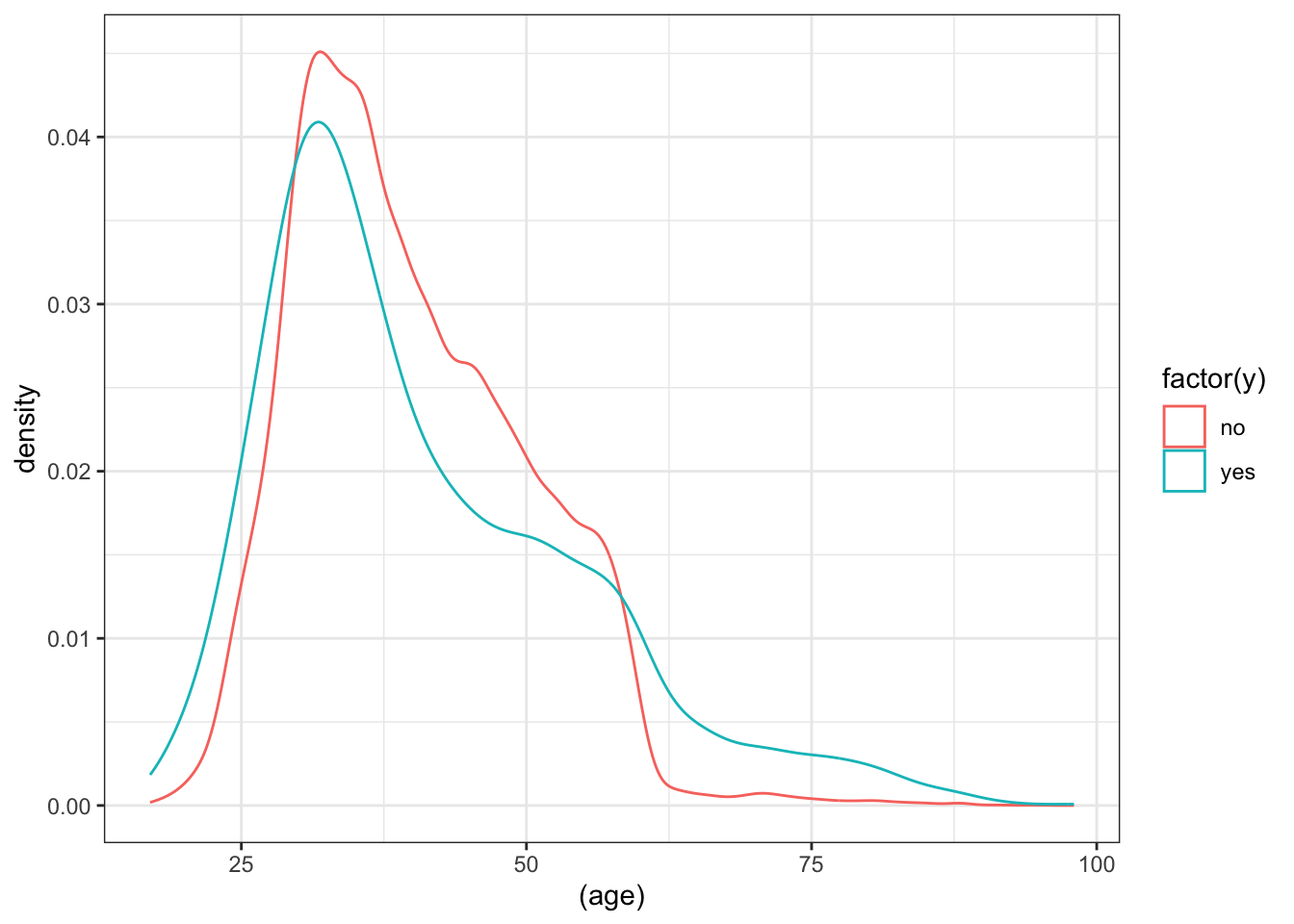

ggplot(data_bank_marketing) + geom_density(aes(x=(age), color=factor(y)))

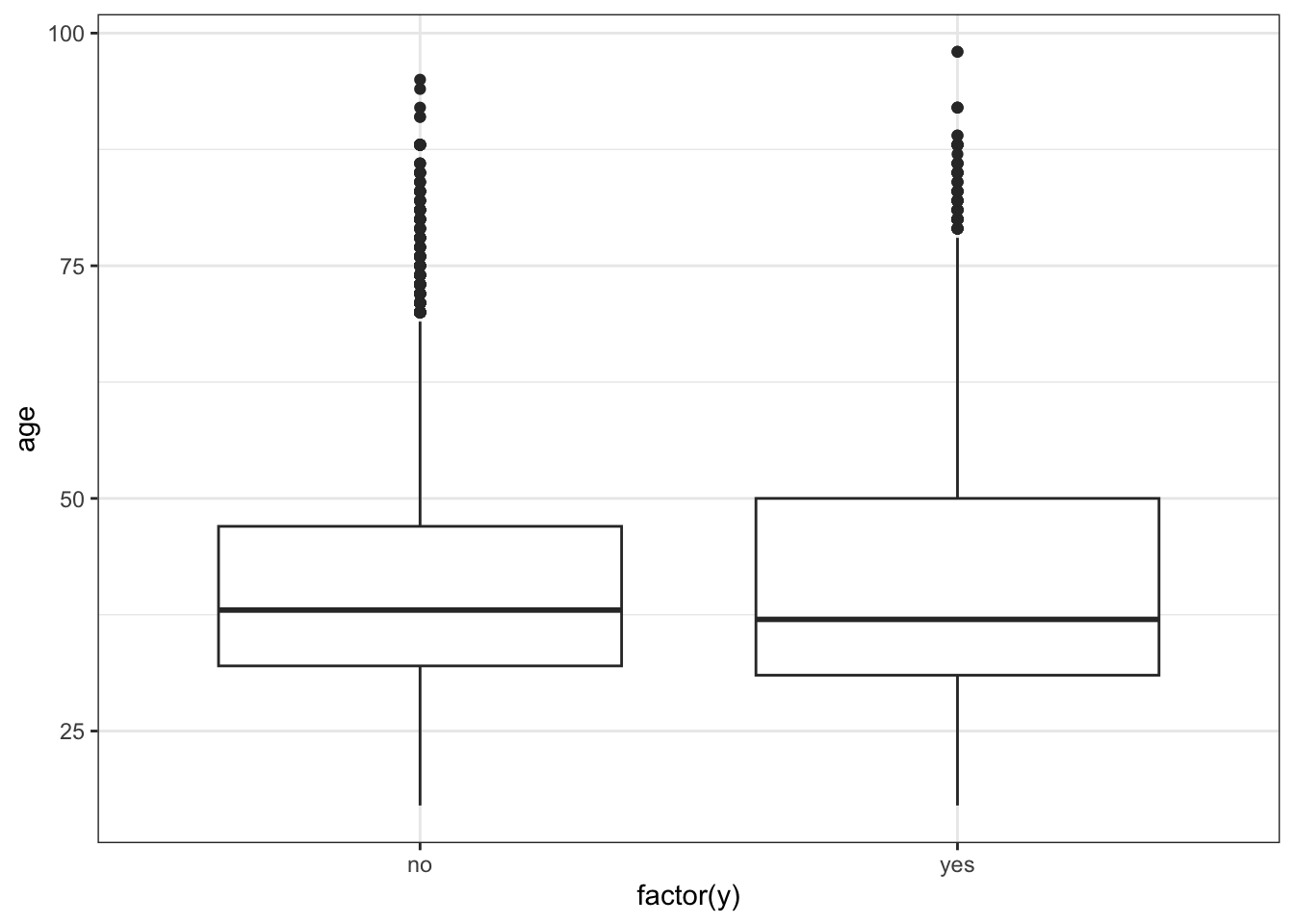

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y = age))

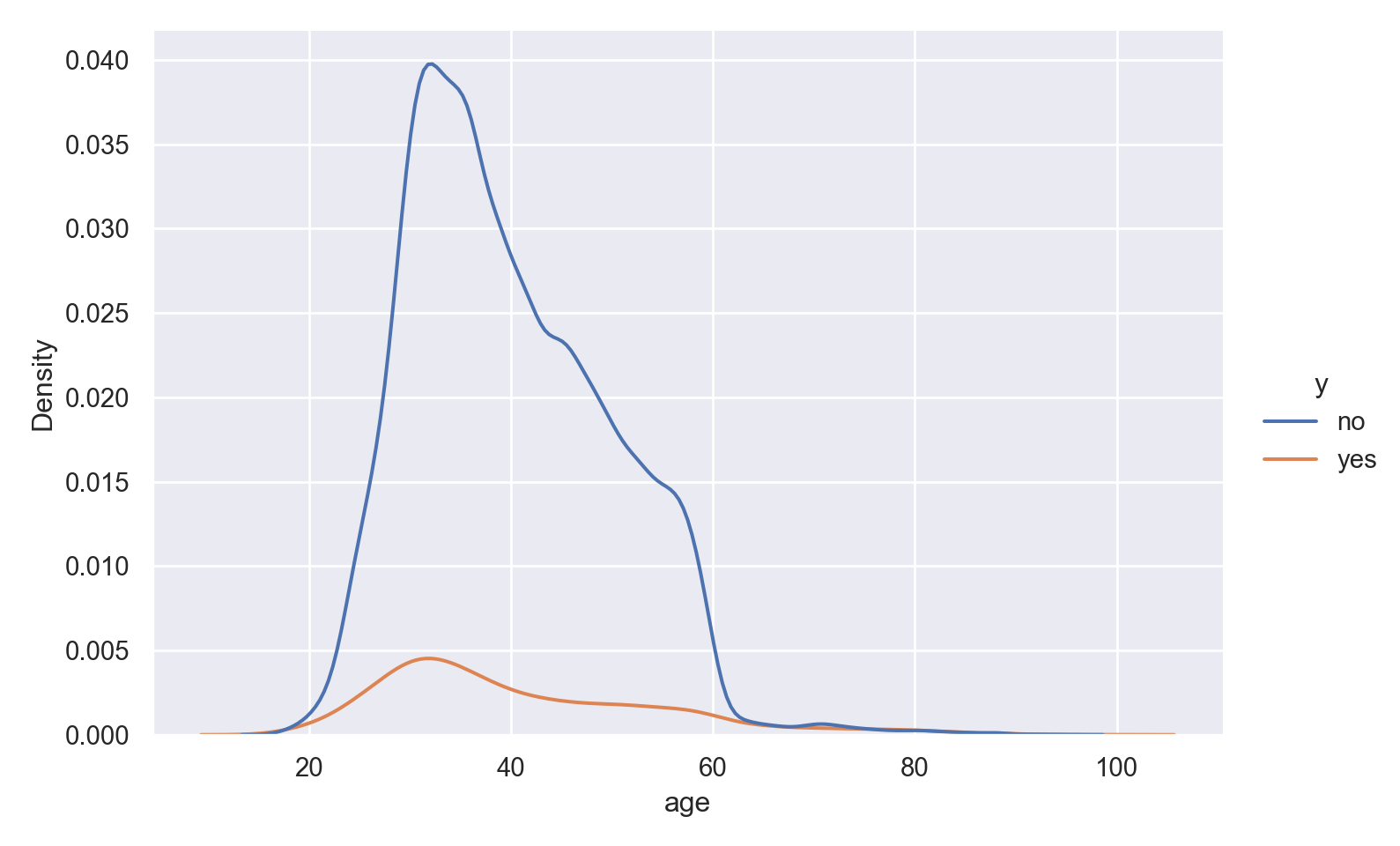

p = sns.displot(data_bank_marketing, x="age", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

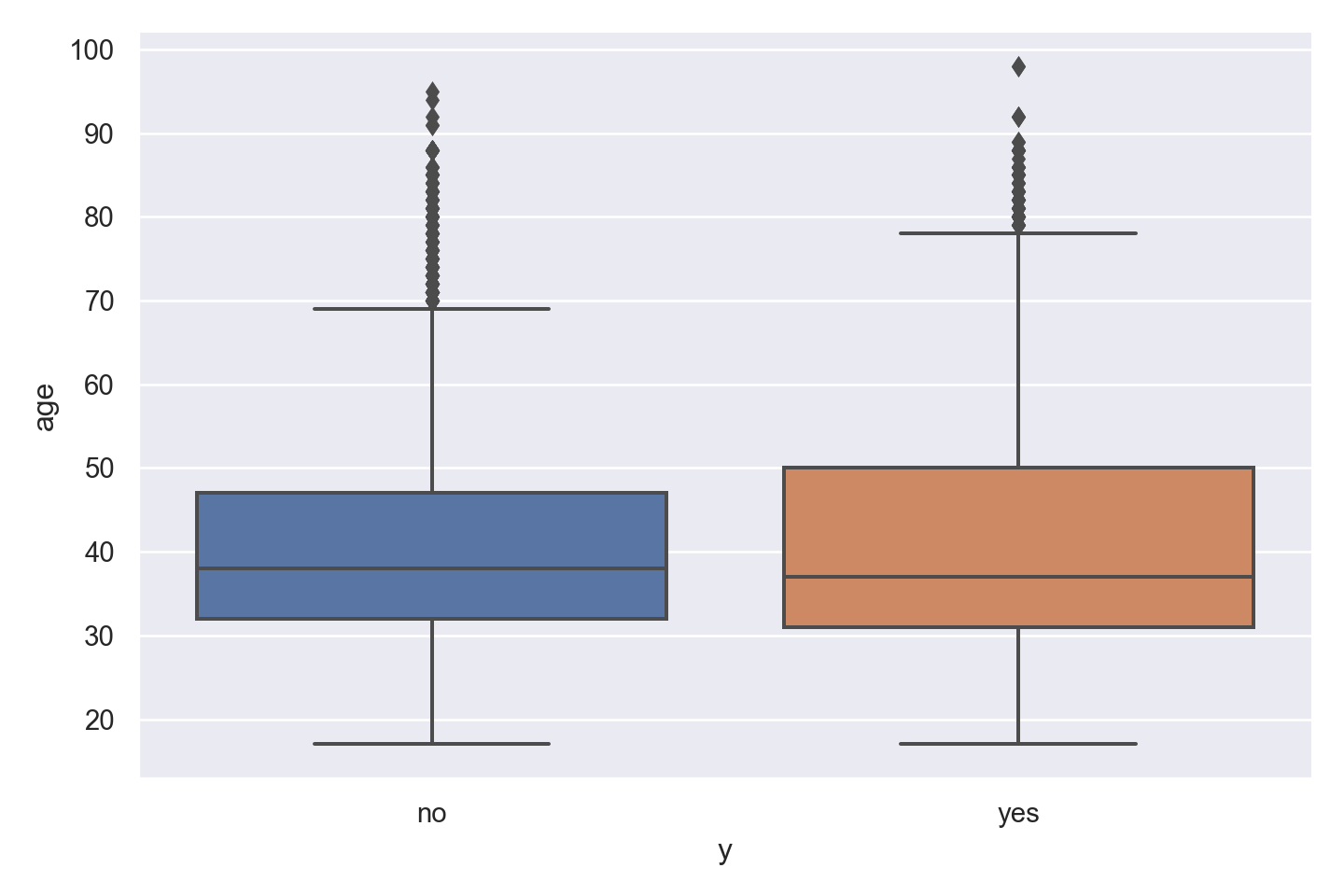

p = sns.catplot(data=data_bank_marketing, x="y", y="age", kind="box", height = 5, aspect = 1.5)

plt.show()

@df data density(:age, group = (:y))

Observations

The data is right (positively) skewed, with more younger respondents.

The density curve indicates higher ‘yes’ outcome for age < 26 and age > 60, which was also seen in the numerical inspection.

The boxplot shows slightly more variation for ‘yes’ outcome, but median value of age is similar for both outcomes, with just a slightly lower age associated with ‘yes’ outcome.

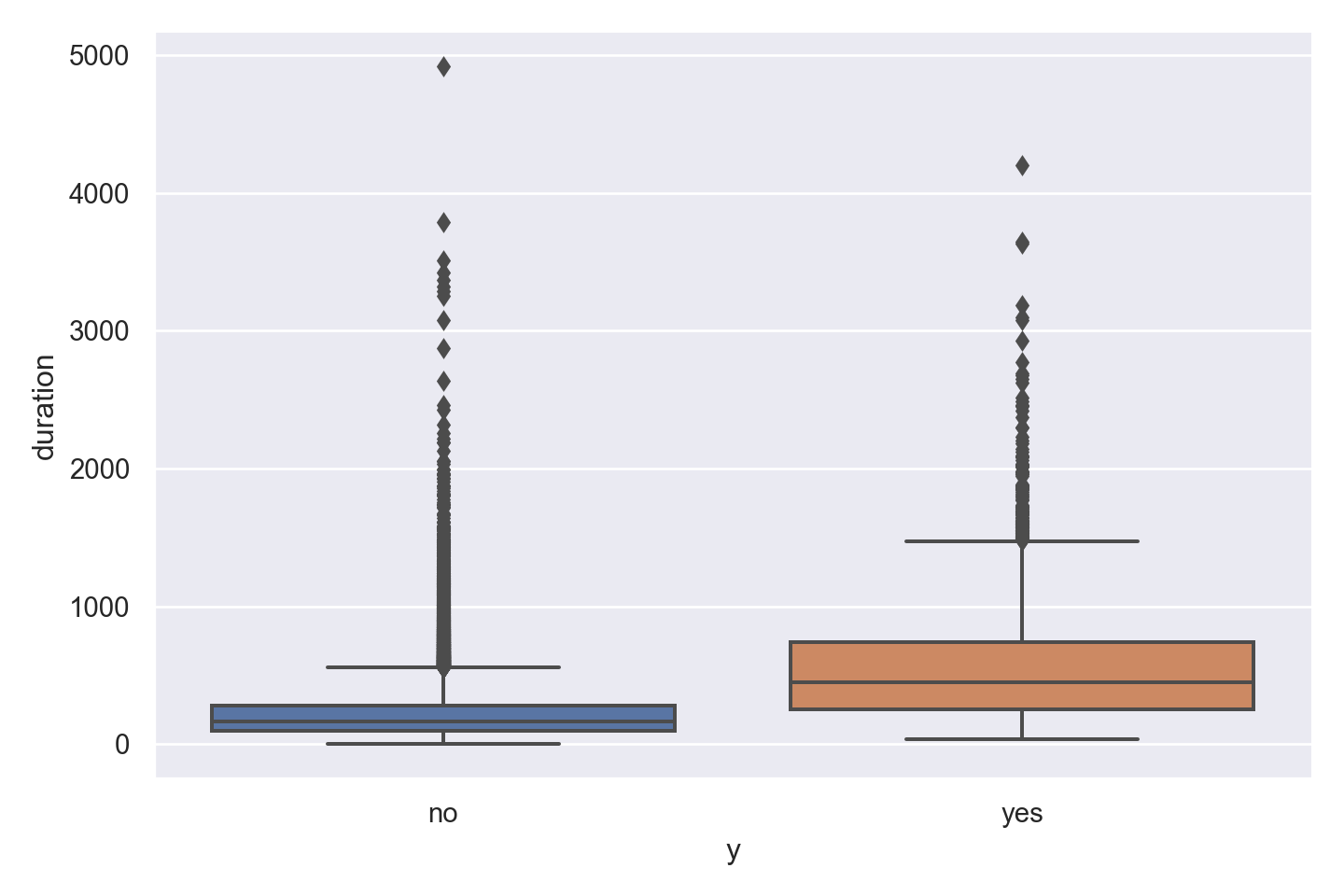

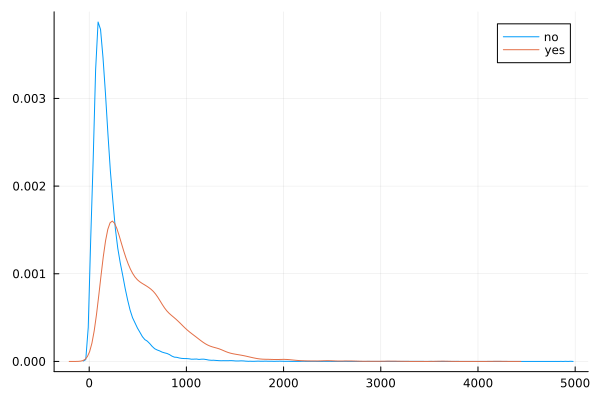

duration

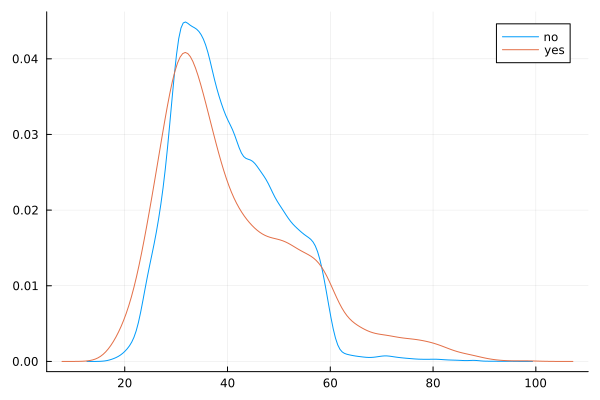

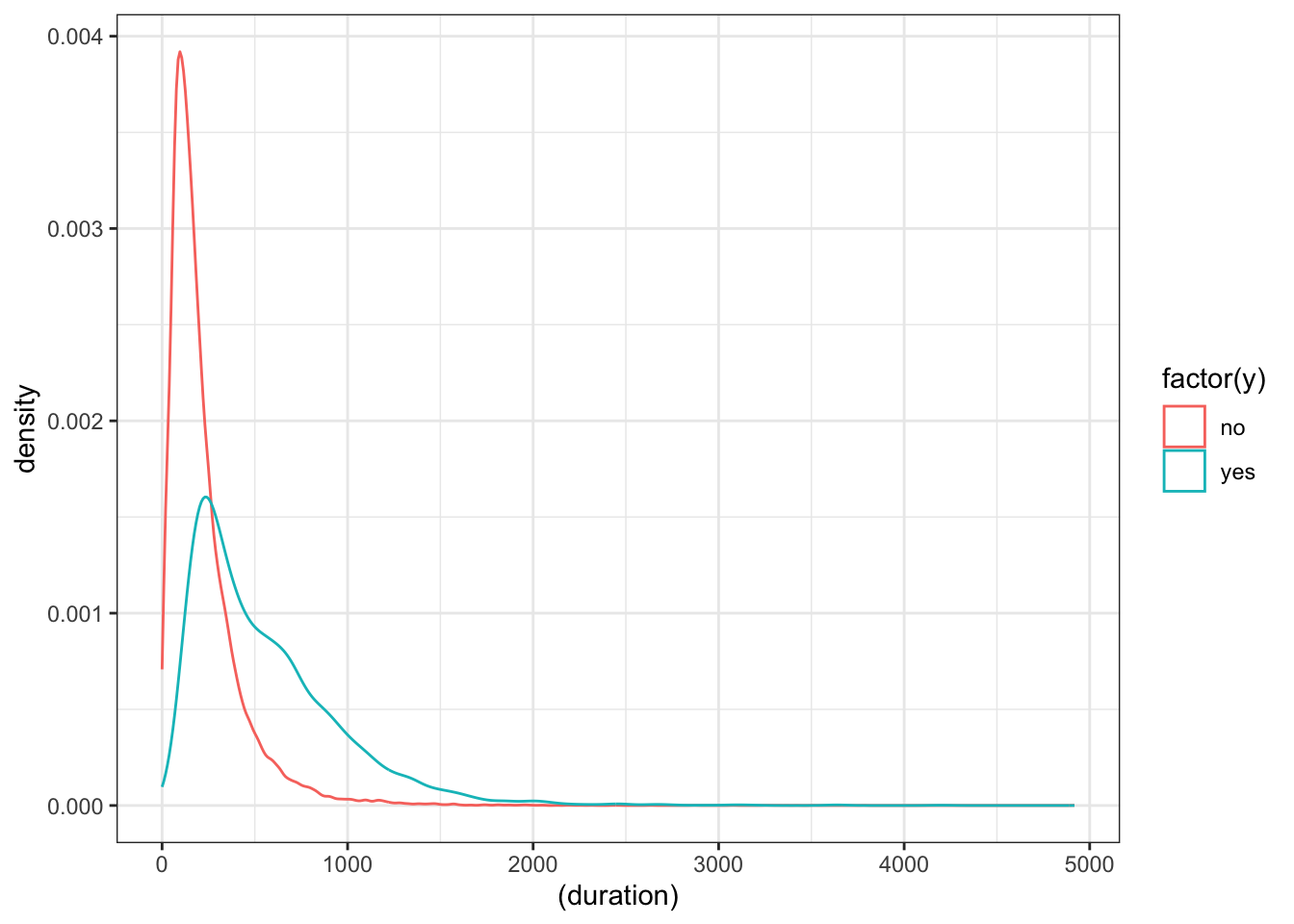

ggplot(data_bank_marketing) + geom_density(aes(x=(duration), color=factor(y)))

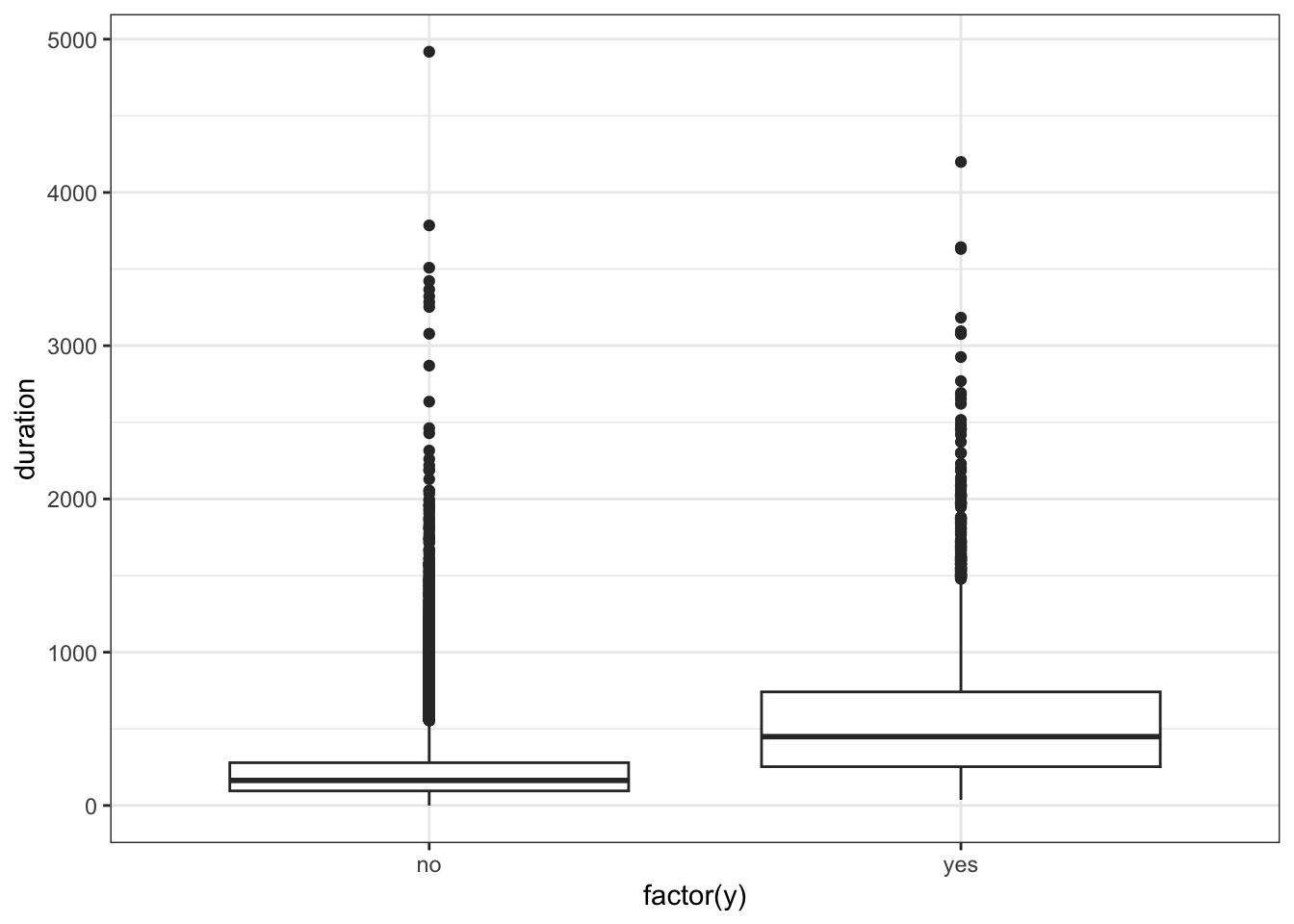

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=duration))

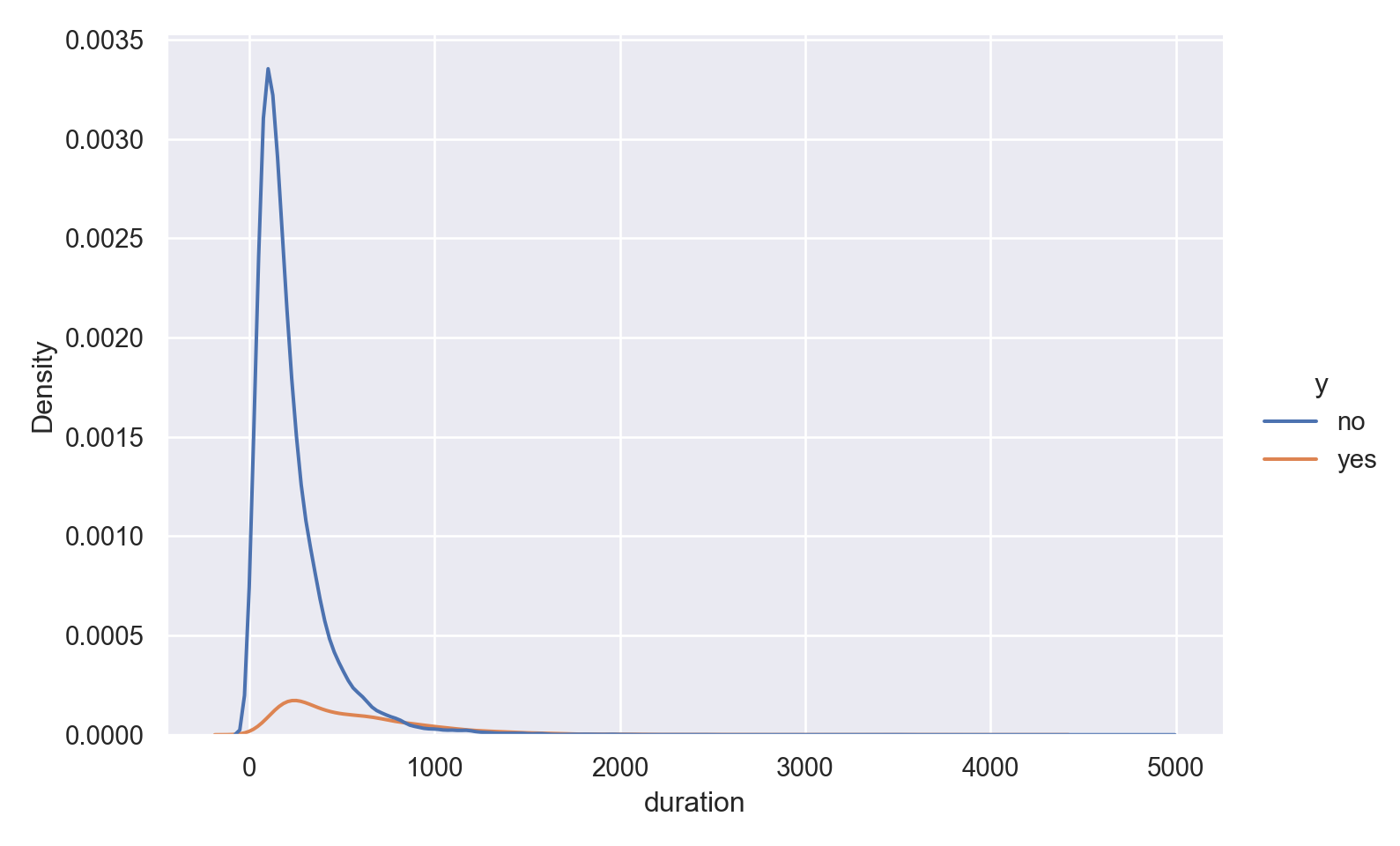

p=sns.displot(data_bank_marketing, x="duration", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

p=sns.catplot(data=data_bank_marketing, x="y", y="duration", kind="box", height = 5, aspect = 1.5)

plt.show()

@df data density(:duration, group = (:y))

Observations

The data is heavily right (positively) skewed, towards low call duration.

As expected, the box plot indicates higher ‘yes’ outcome for higher duration, however as mentioned in the data dictionary, this will not help in predictive modelling as duration is not known before placing a call. It is the result of a ‘yes’ decision, and not its cause.

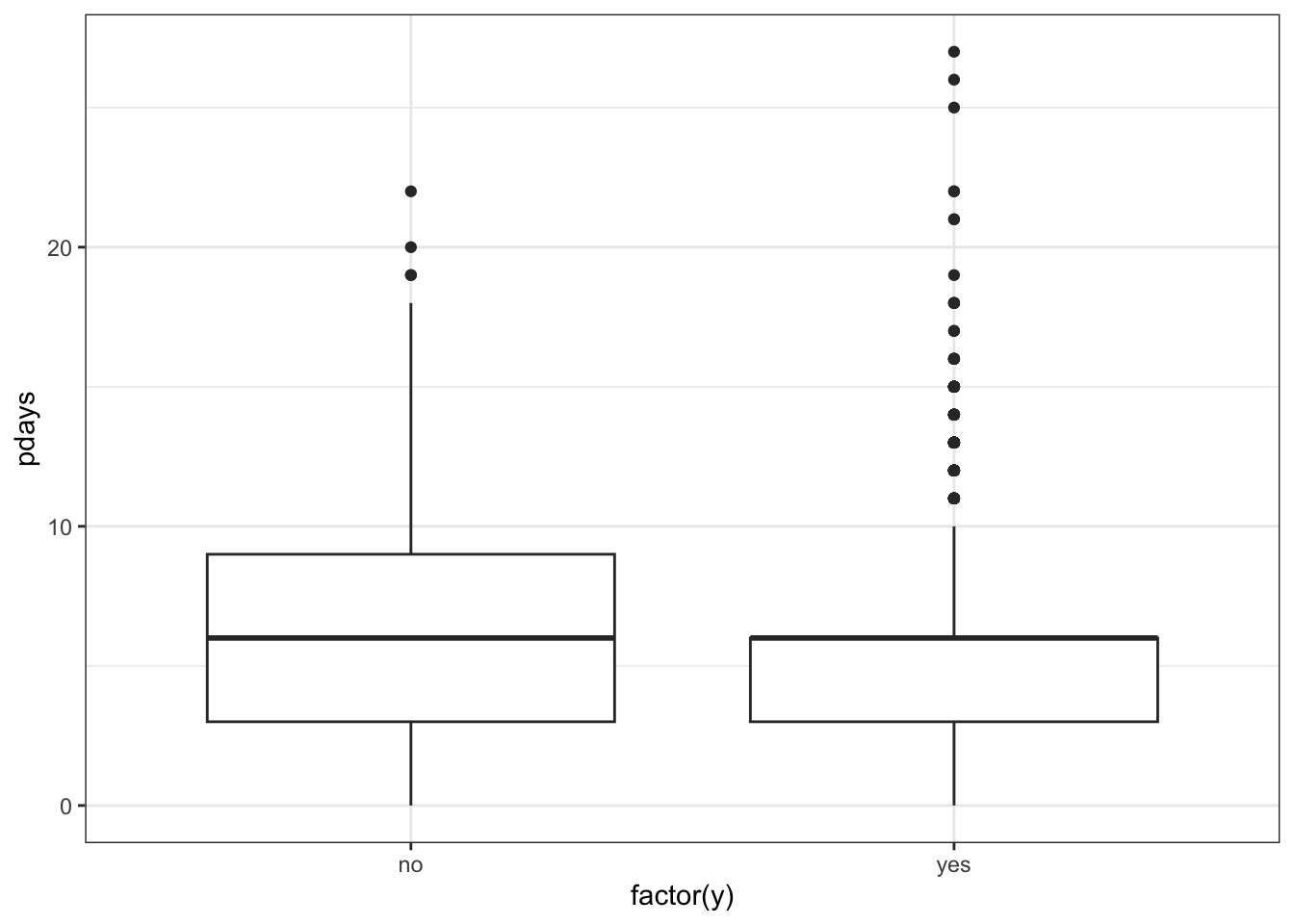

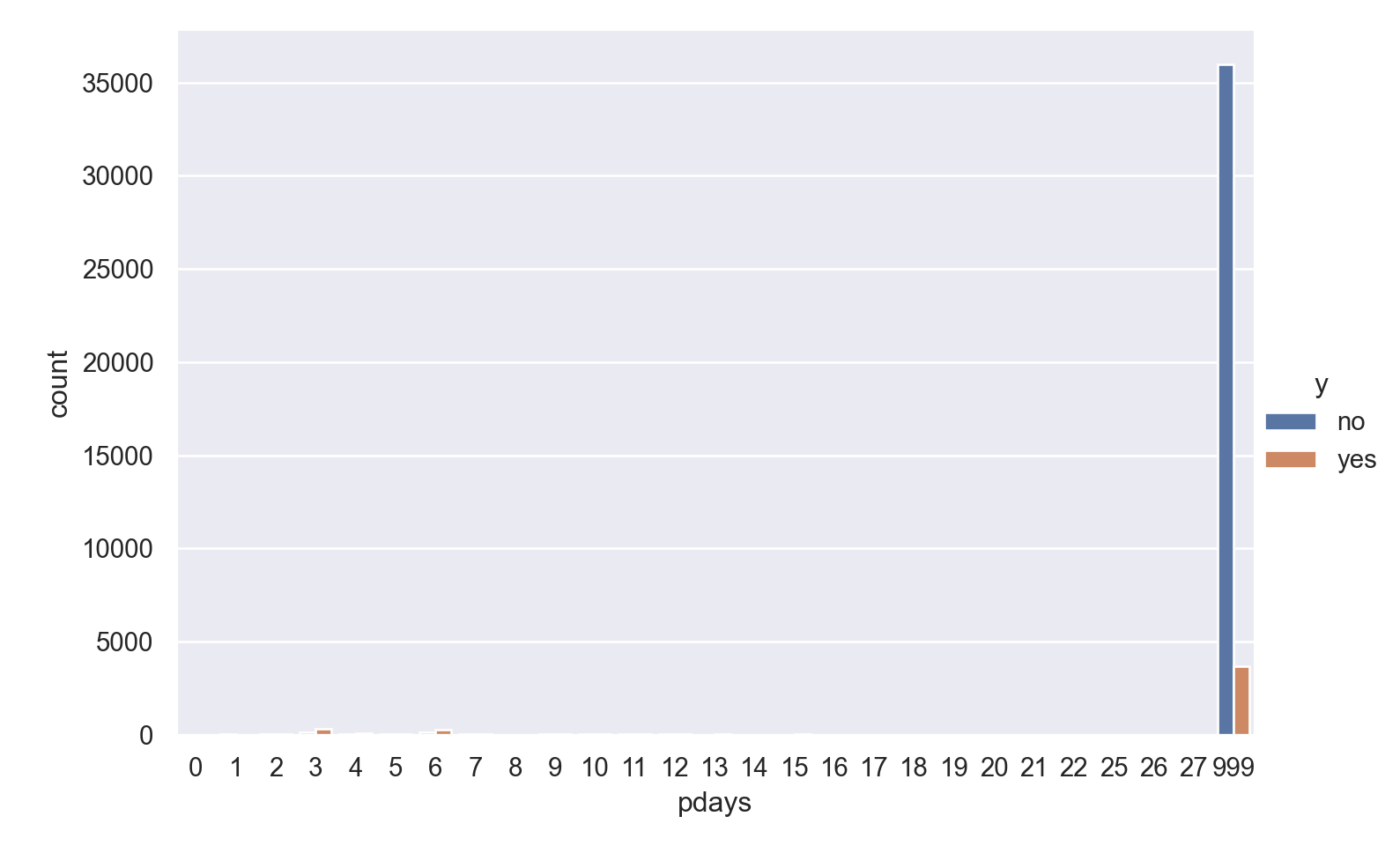

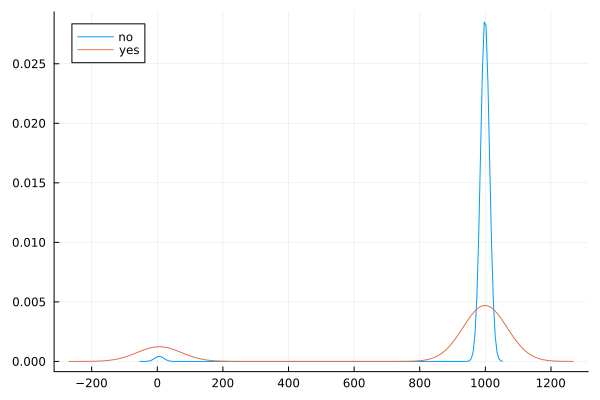

pdays

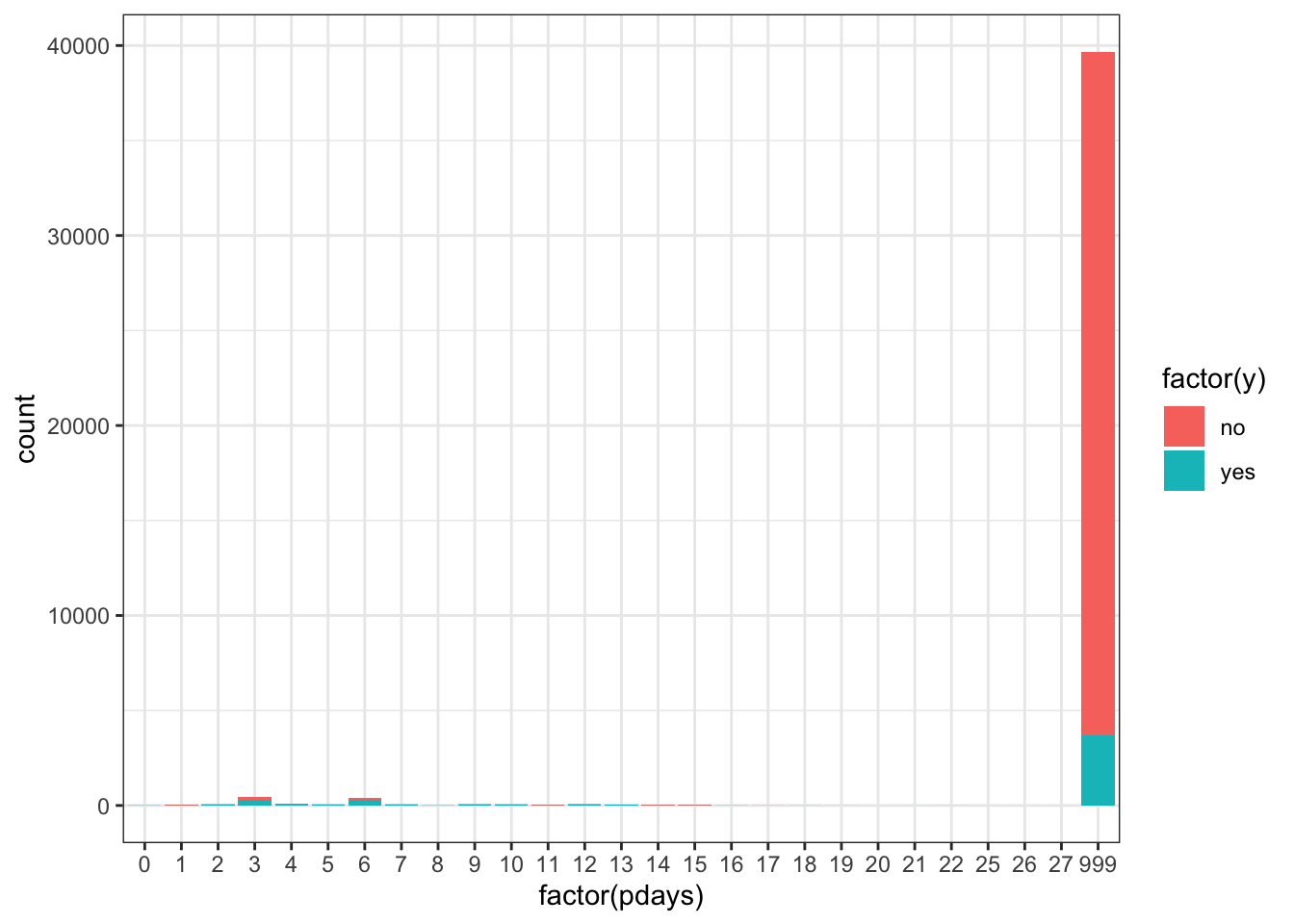

ggplot(data_bank_marketing) + geom_bar(aes(x=factor(pdays), fill=factor(y)))

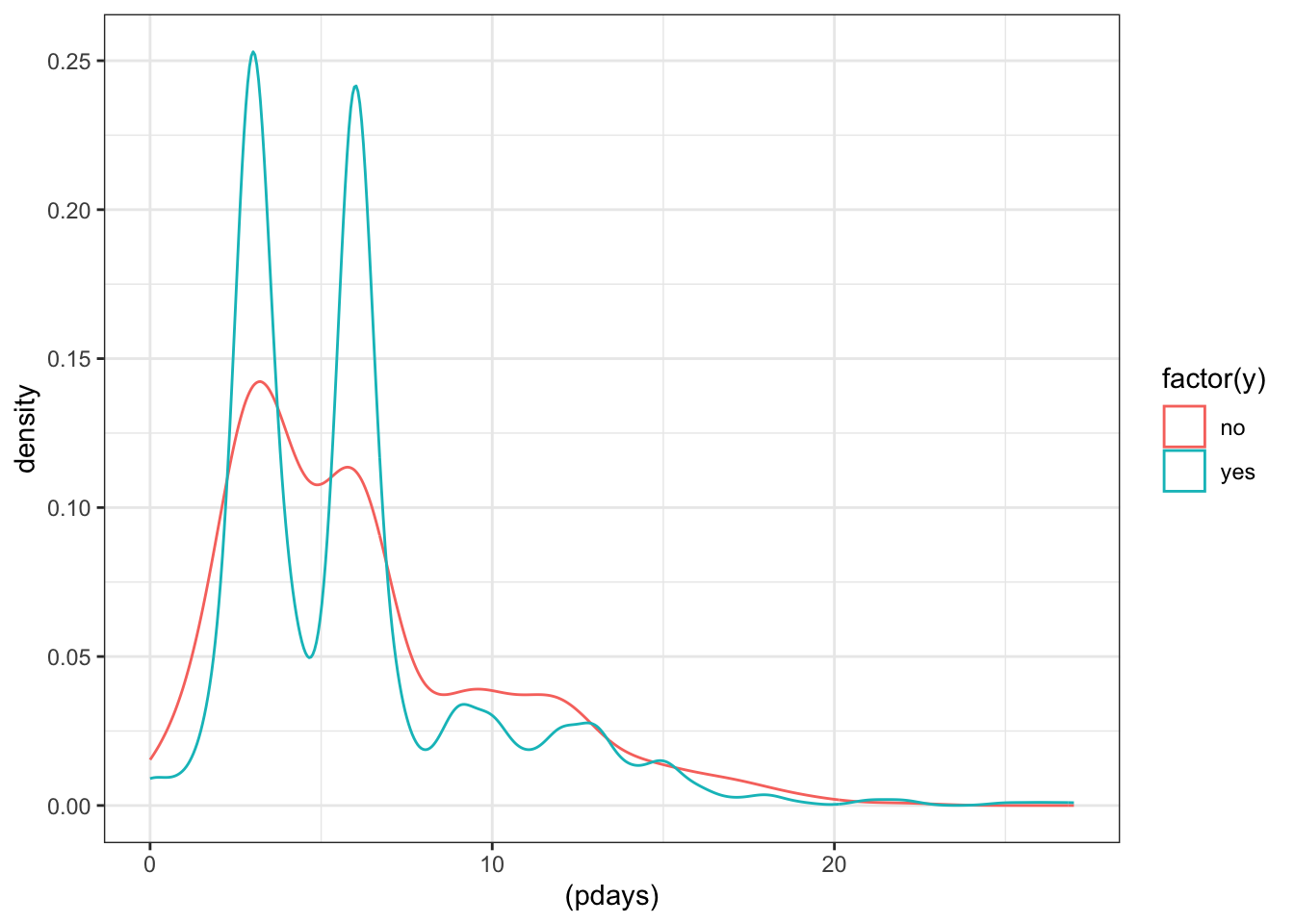

ggplot(data_bank_marketing %>% filter(pdays<999)) + geom_density(aes(x=(pdays), color=factor(y)))

ggplot(data_bank_marketing %>% filter(pdays<999)) + geom_boxplot(aes(x=factor(y), y=pdays))

p=sns.catplot(data=data_bank_marketing, x="pdays", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

@df data density(:pdays, group = (:y))

Observations

The vast majority of people were not previously contacted, so there is a very high left skew.

Filtering to only include the previously contacted people reveals a bi-modal pattern in the data, especially for respondents with ‘yes’ outcome.

For those that were previously contacted, median value of days since previous contact is the same for both outcomes, but ‘yes’ outcome has many outliers on the higher end.

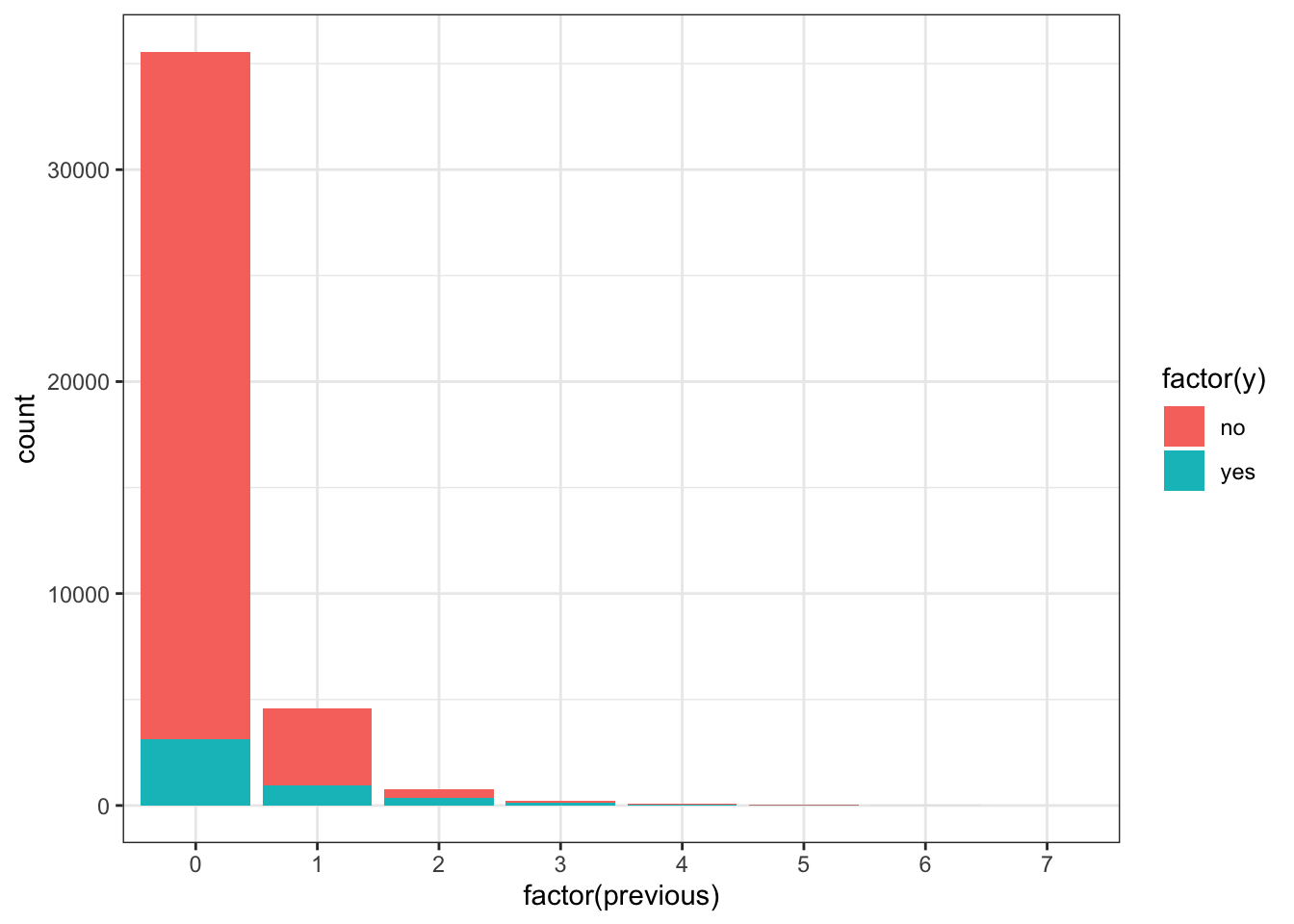

previous

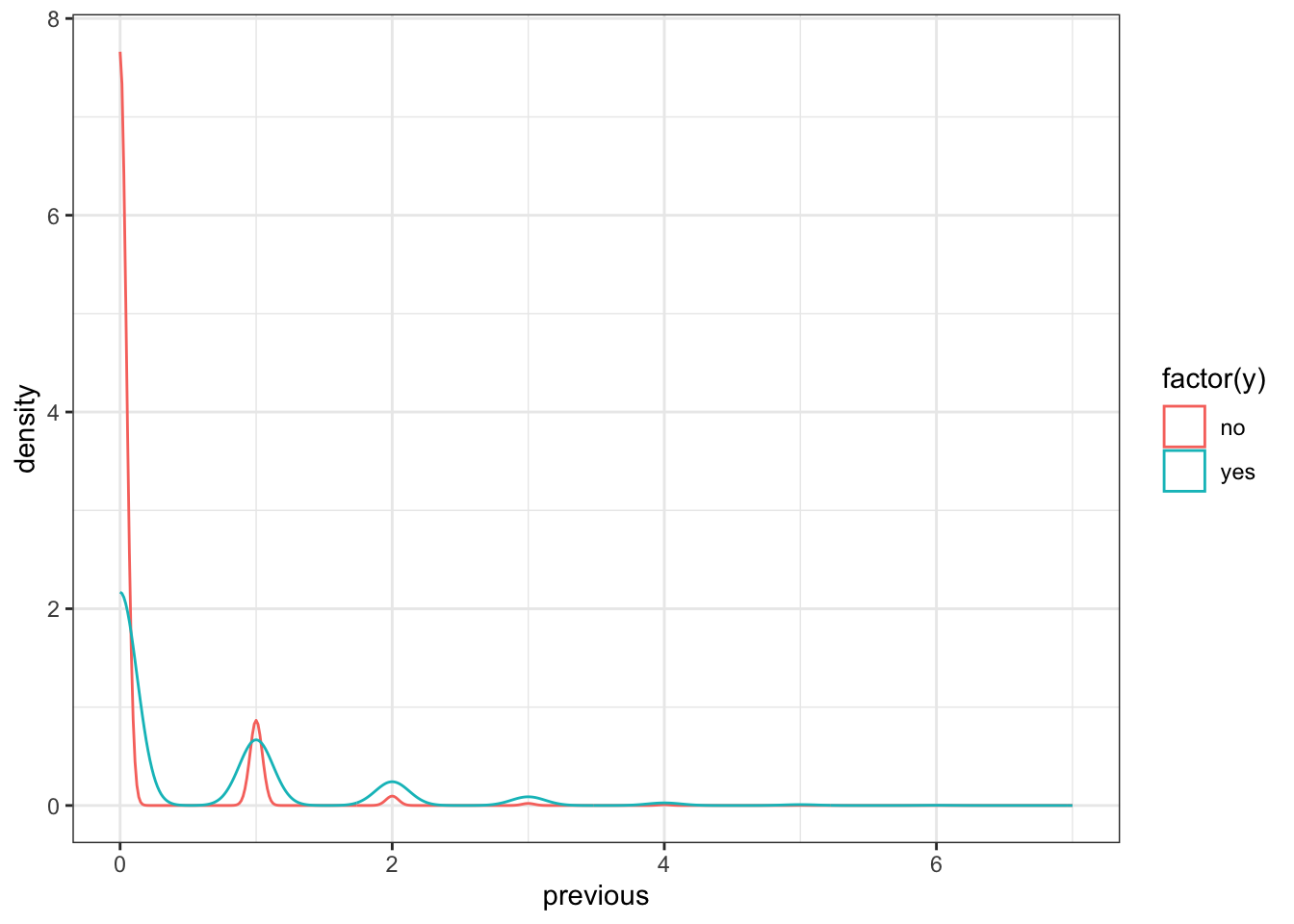

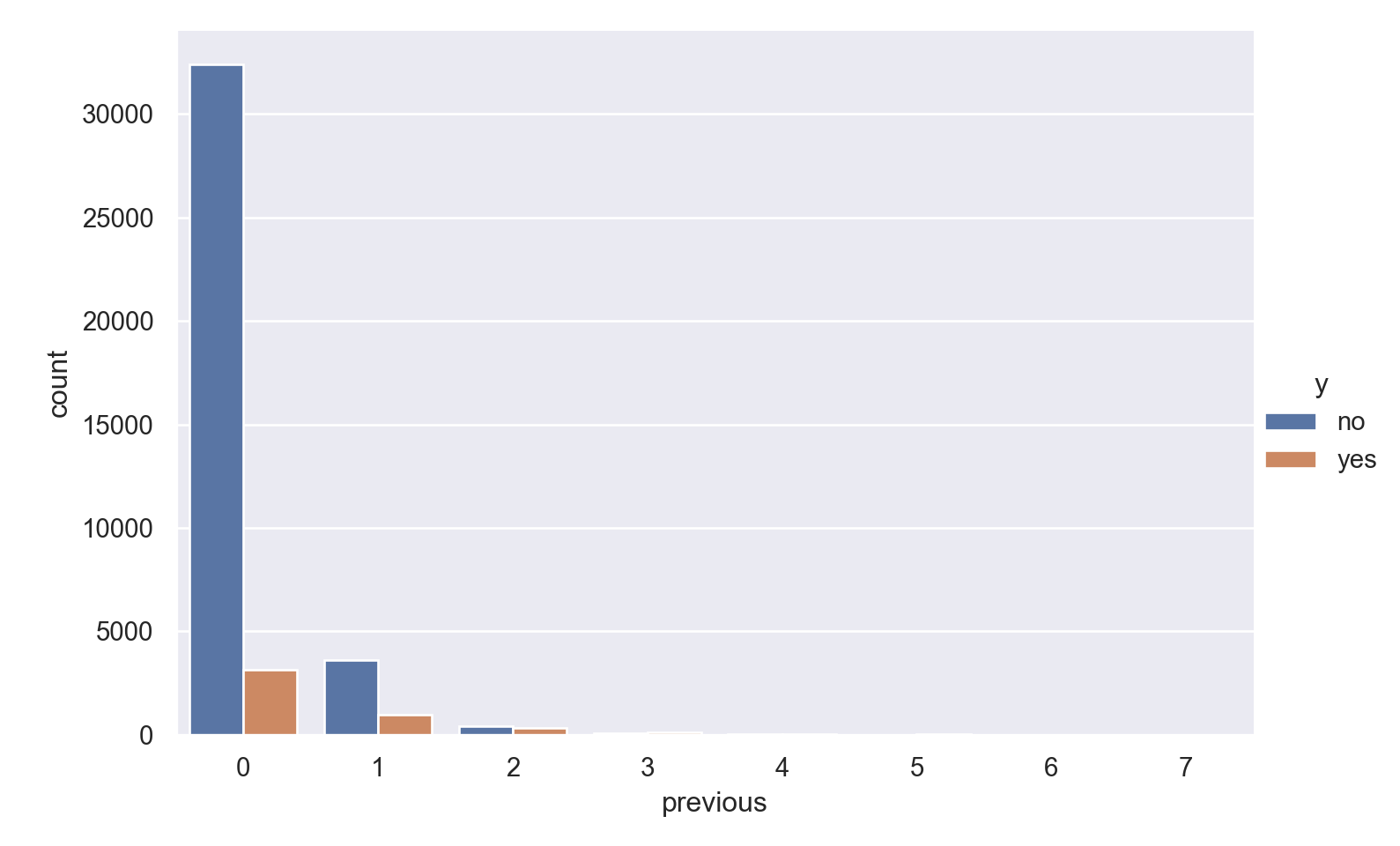

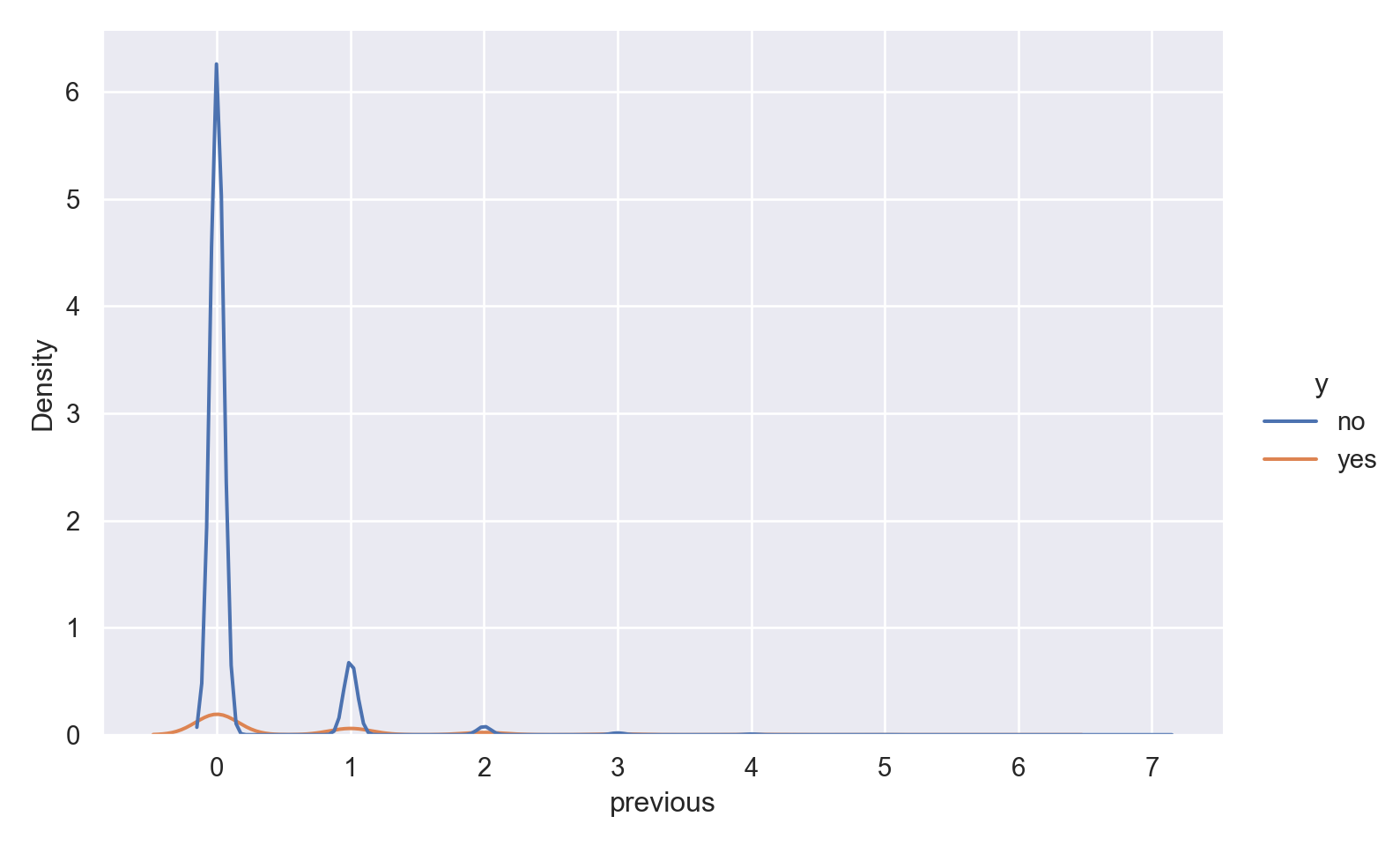

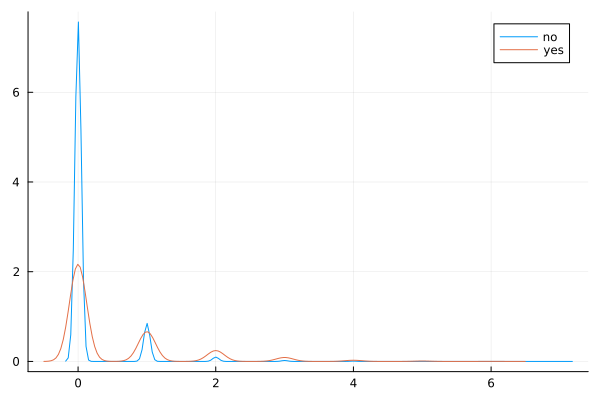

ggplot(data_bank_marketing) + geom_bar(aes(x=factor(previous), fill=factor(y)))

ggplot(data_bank_marketing) + geom_density(aes(x=previous, color=factor(y)))

p=sns.catplot(data=data_bank_marketing, x="previous", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

p=sns.displot(data_bank_marketing, x="previous", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

@df data density(:previous, group = (:y))

Observations

The vast majority of people were not previously contacted in the previous campaign, so there is a very high right skew.

The few people who were contacted multiple times seem to show higher ‘yes’ outcome for the current campaign.

campaign

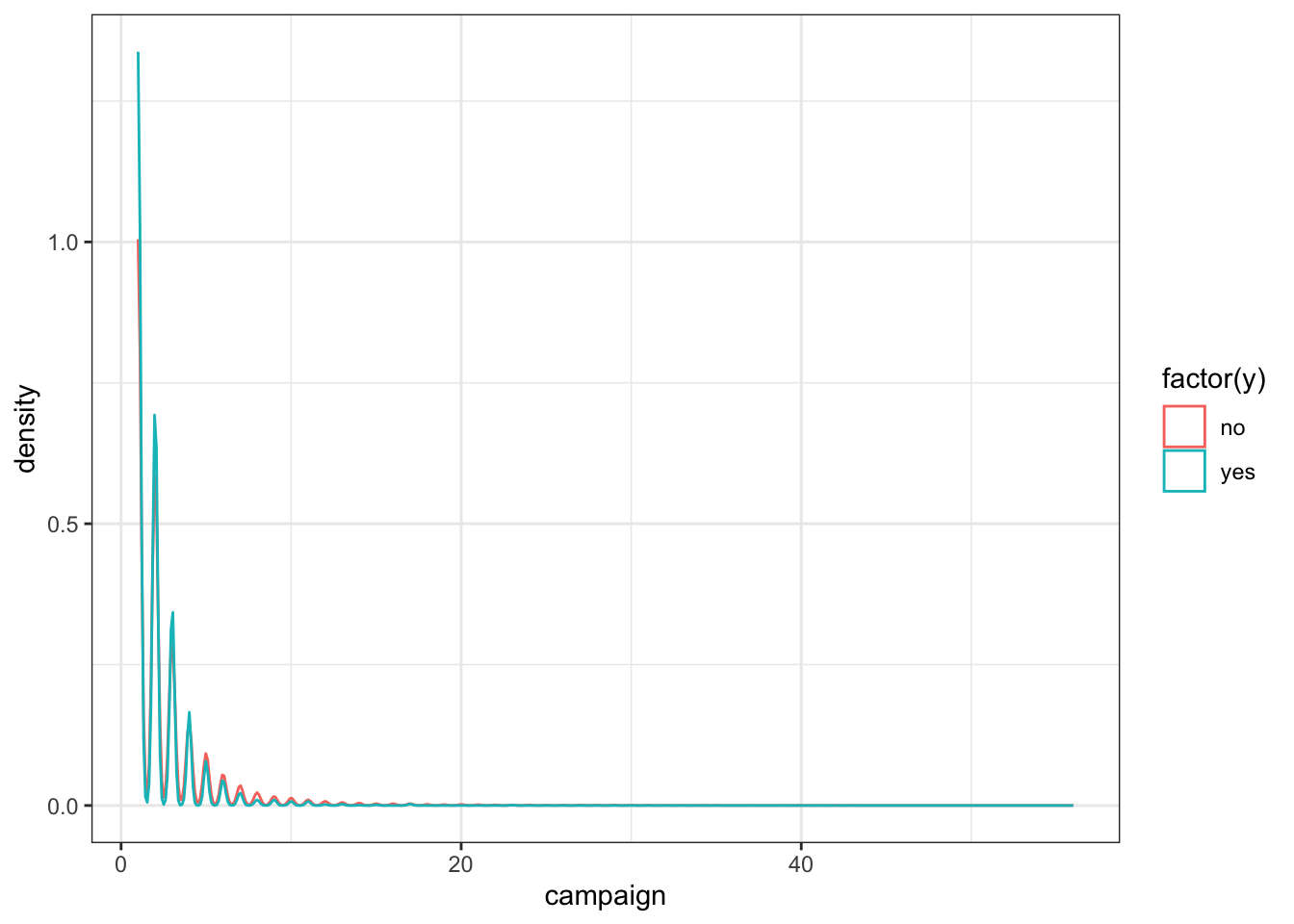

ggplot(data_bank_marketing) + geom_density(aes(x=campaign, color=factor(y)))

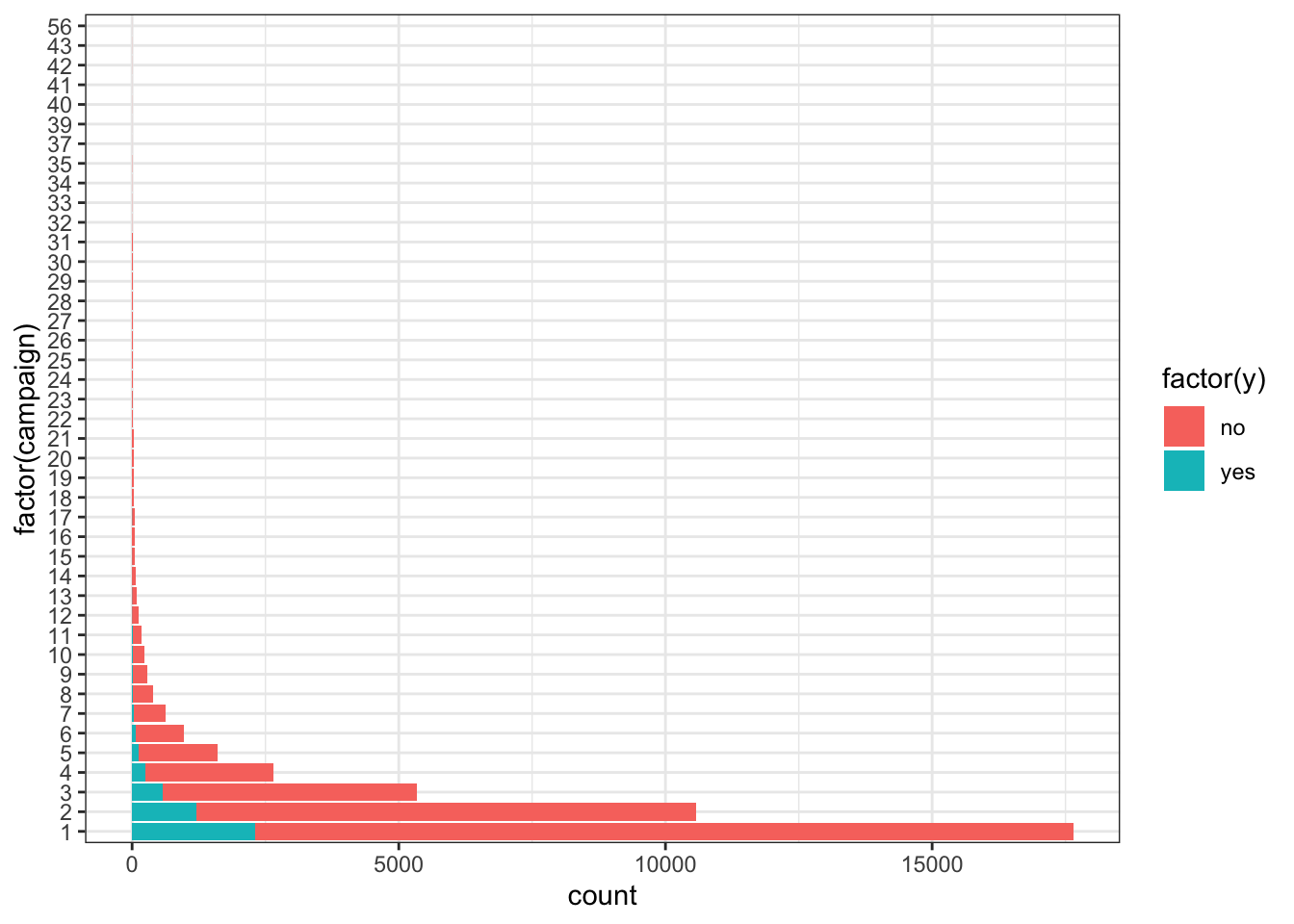

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(campaign), fill=factor(y)))

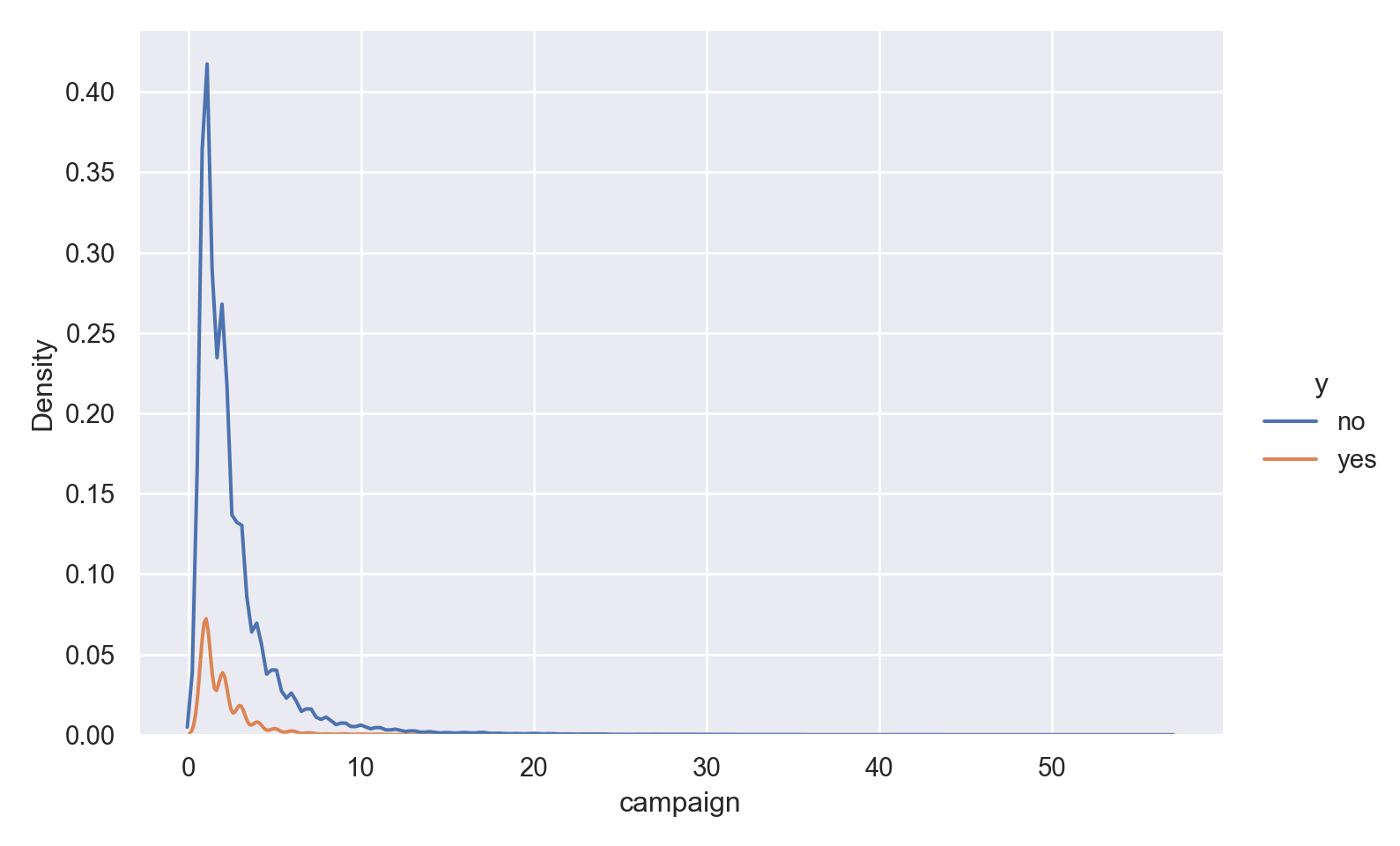

p=sns.displot(data_bank_marketing, x="campaign", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

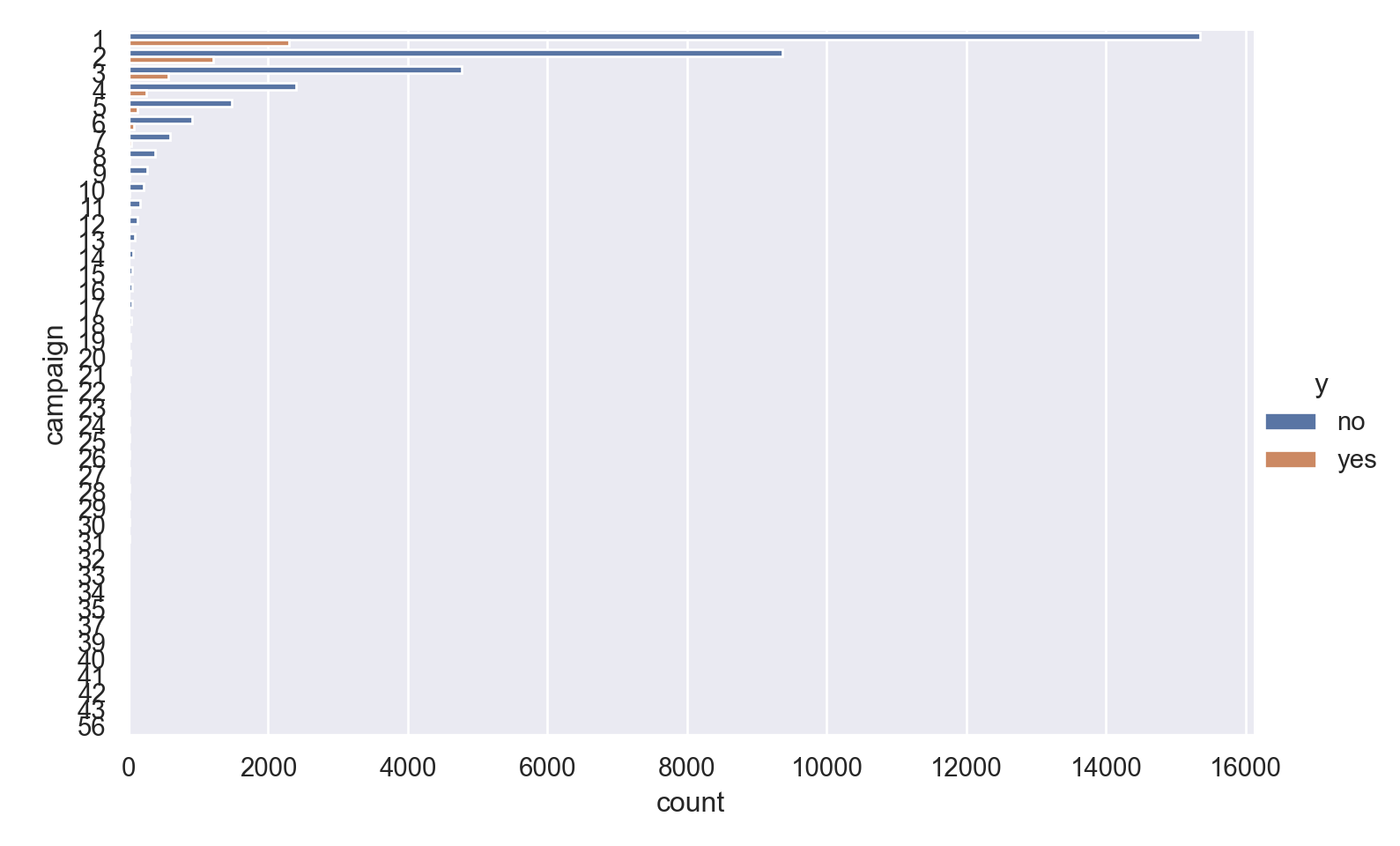

p=sns.catplot(data=data_bank_marketing, y="campaign", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

data1 = @transform(data, :campaign = categorical(:campaign));

p=@df data1 bar(:campaign, group = (:y))Plot{Plots.GRBackend() n=2}@df data1 density(:campaign, group = (:y))

display(p)Plot{Plots.GRBackend() n=2}Observations

The vast majority of people were contacted only once in the current campaign, so there is a very high right skew.

The few people who were contacted multiple times seem to show higher ‘yes’ outcome.

emp.var.rate

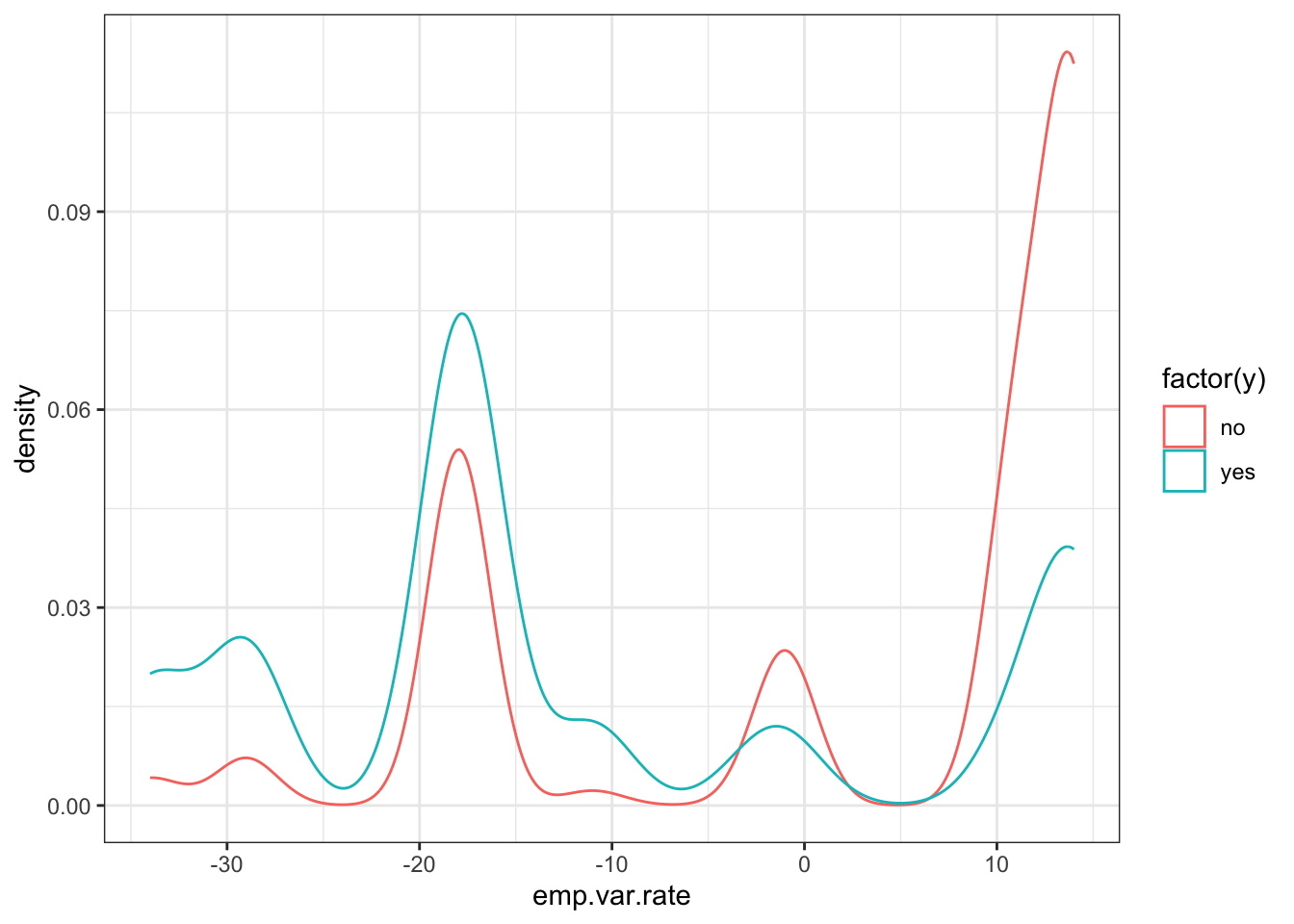

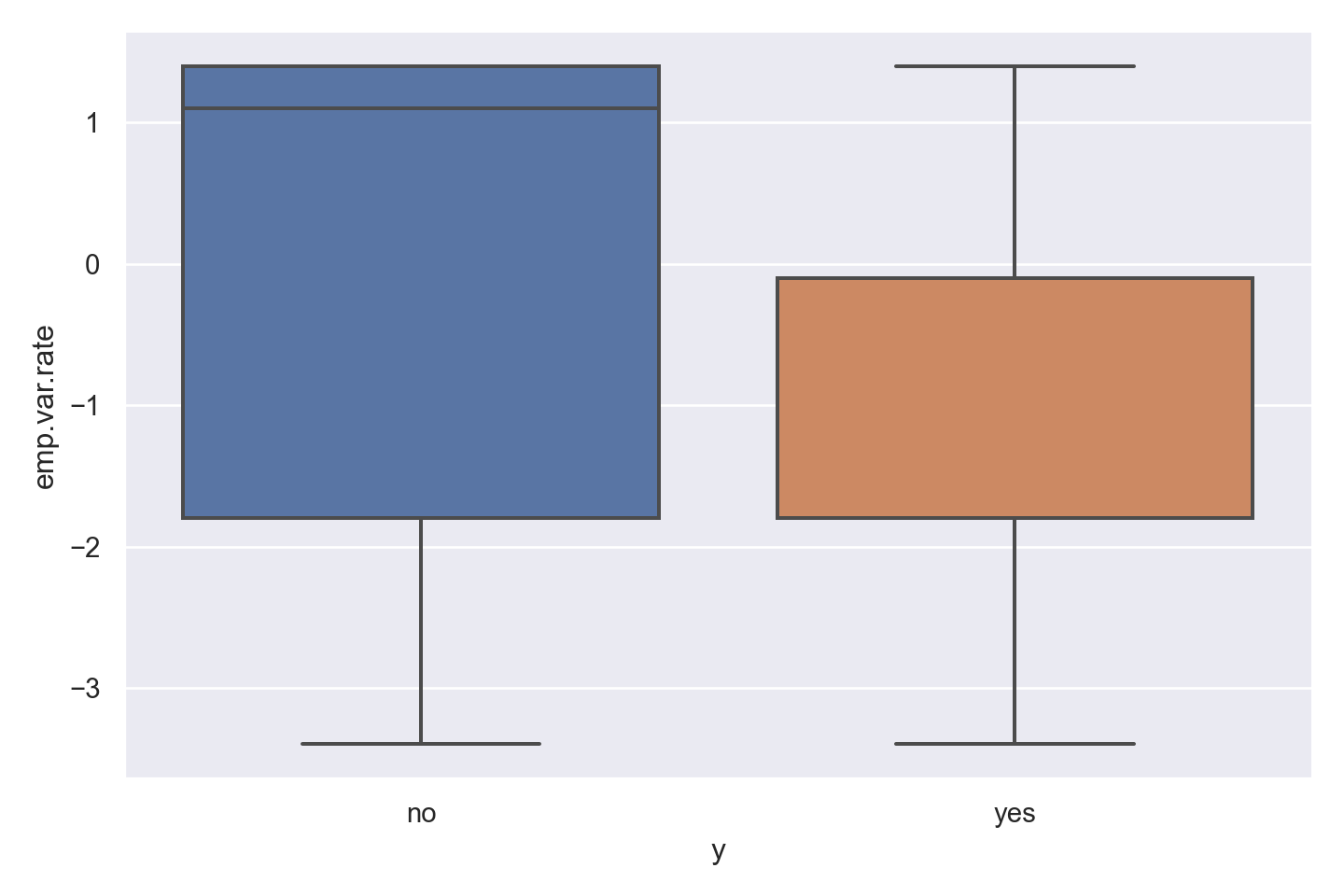

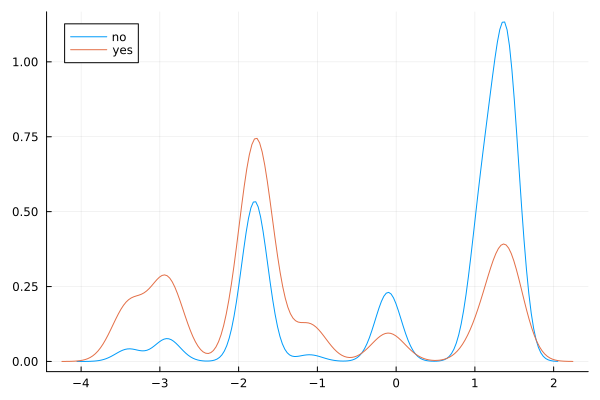

ggplot(data_bank_marketing) + geom_density(aes(x=emp.var.rate, color=factor(y)))

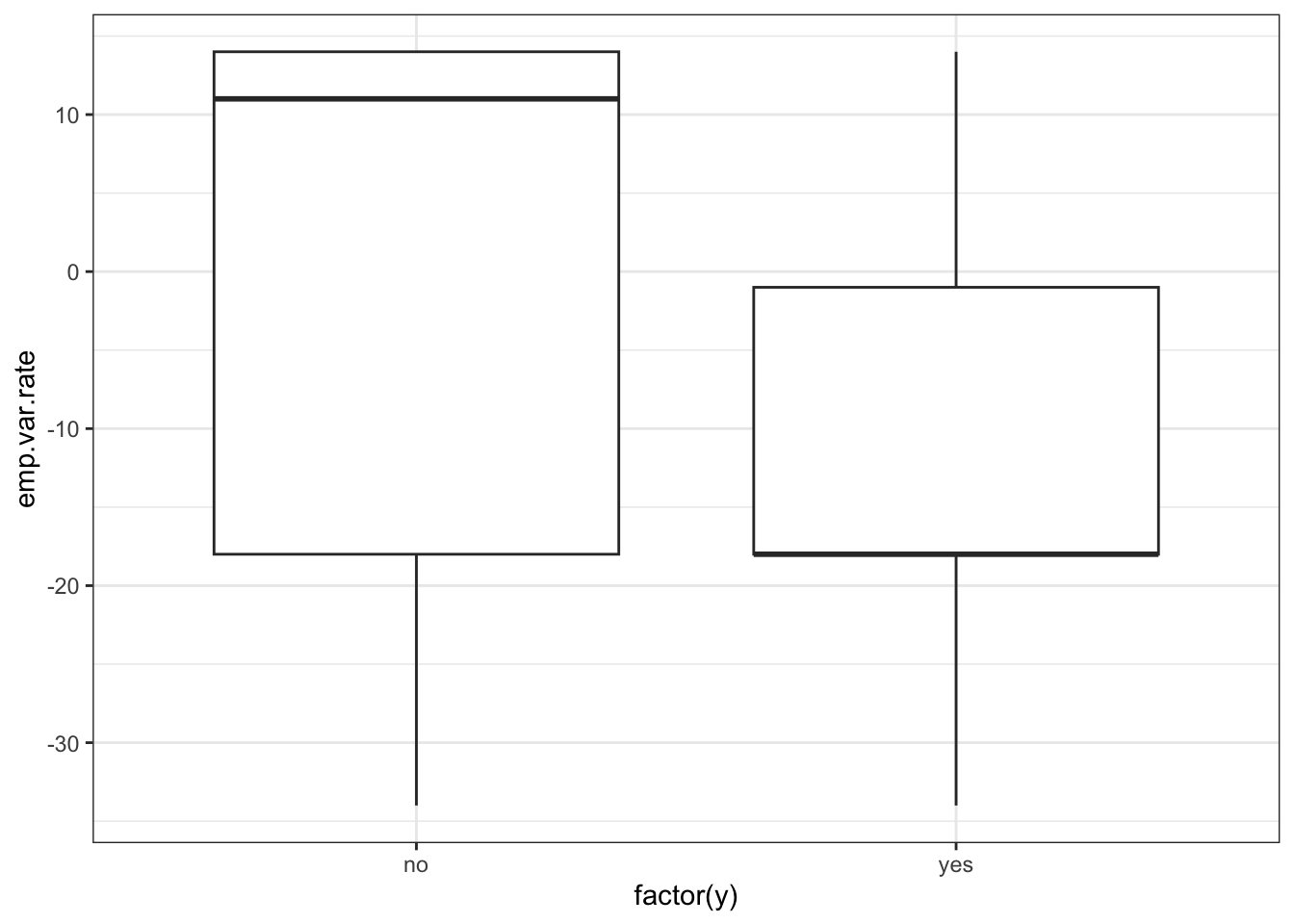

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=emp.var.rate))

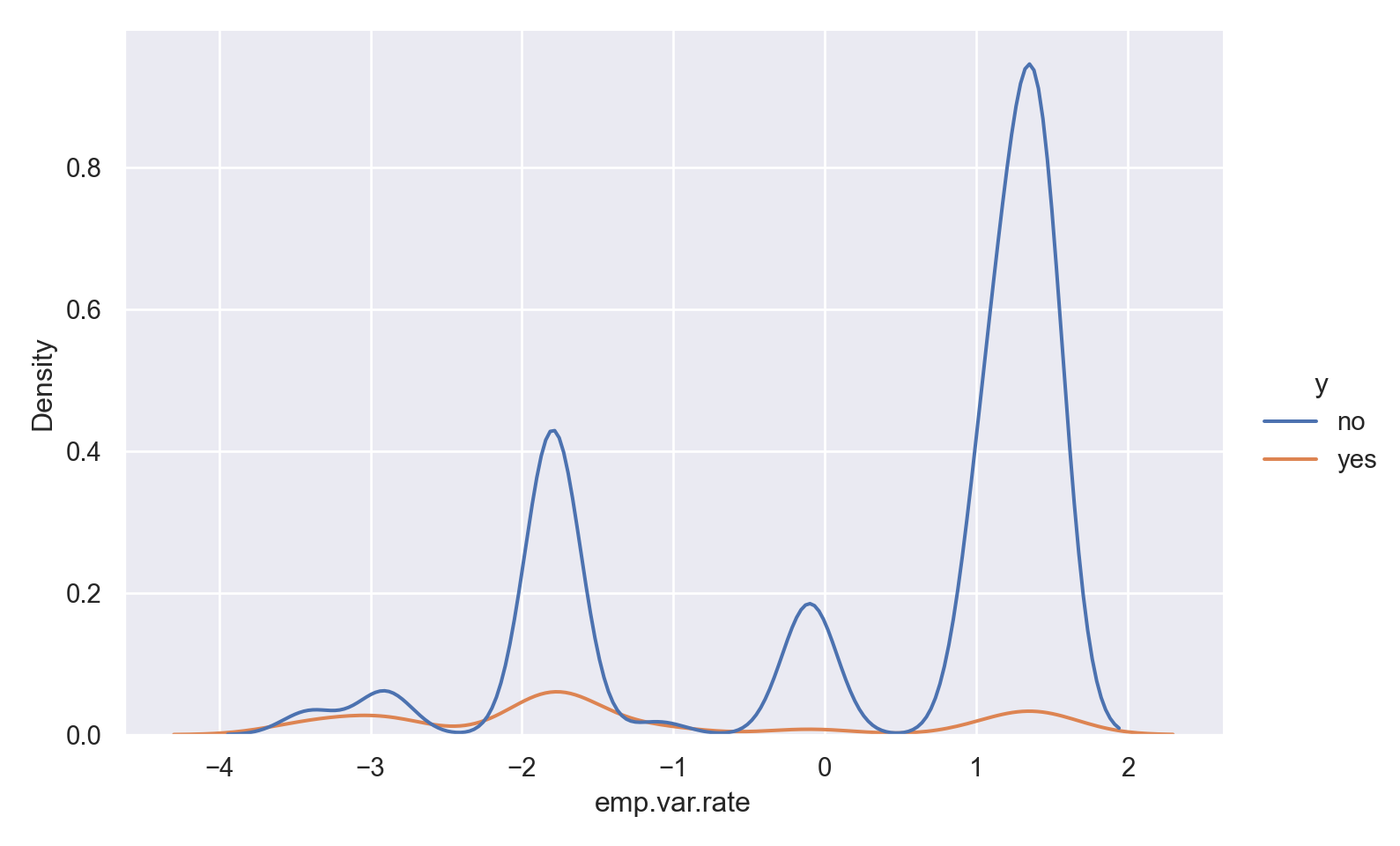

p=sns.displot(data_bank_marketing, x="emp.var.rate", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

p=sns.catplot(data=data_bank_marketing, x="y", y="emp.var.rate", kind="box", height = 5, aspect = 1.5)

plt.show()

data1=rename(data, "emp.var.rate" => "emp_var_rate");

@df data1 density(:emp_var_rate, group = (:y))

Observations

There is a striking association between employment variation rate and response - ‘yes’ outcomes show a much lower variation rate.

There is a multi-modal pattern in the data.

cons.price.idx

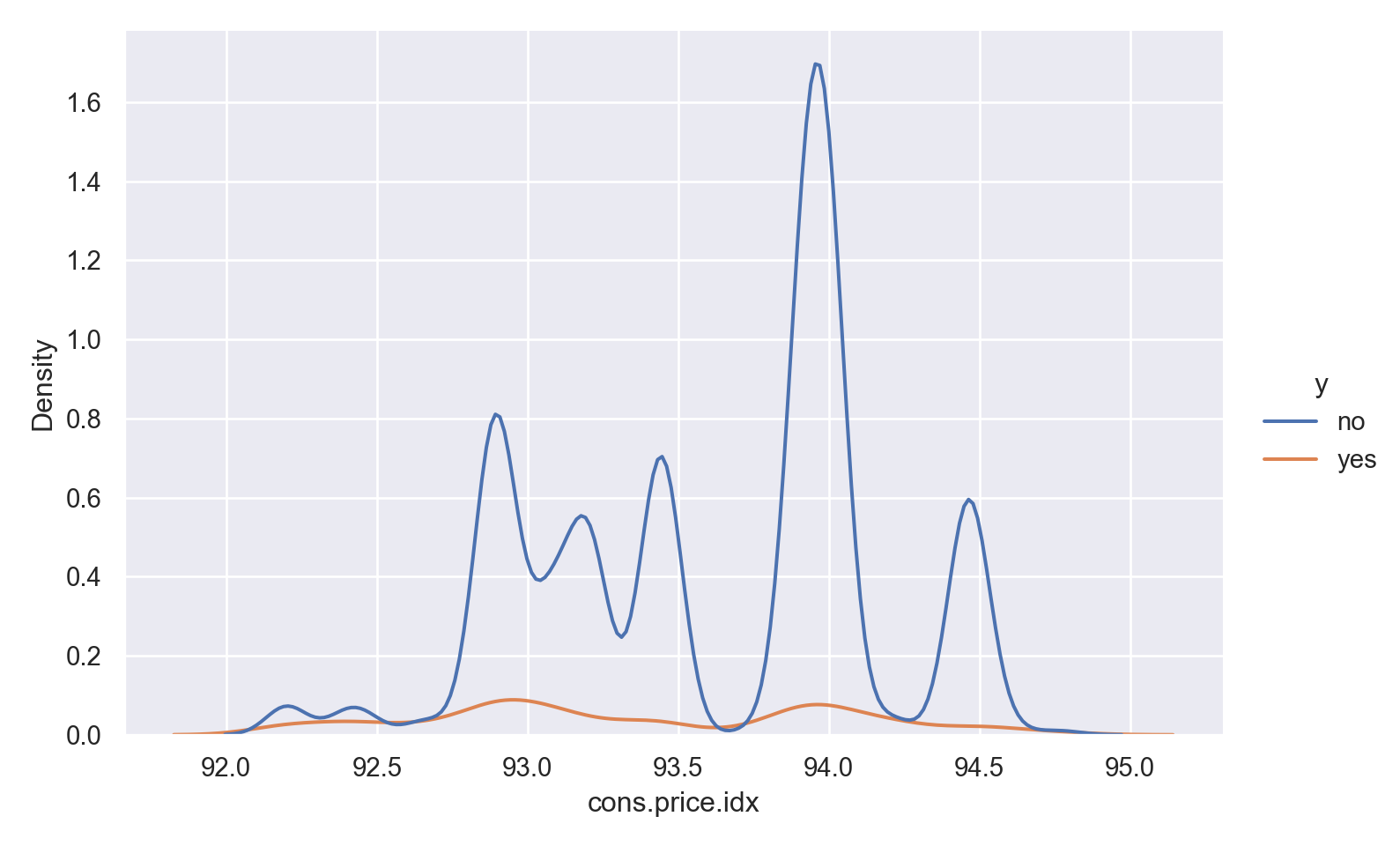

ggplot(data_bank_marketing) + geom_density(aes(x=cons.price.idx, color=factor(y)))

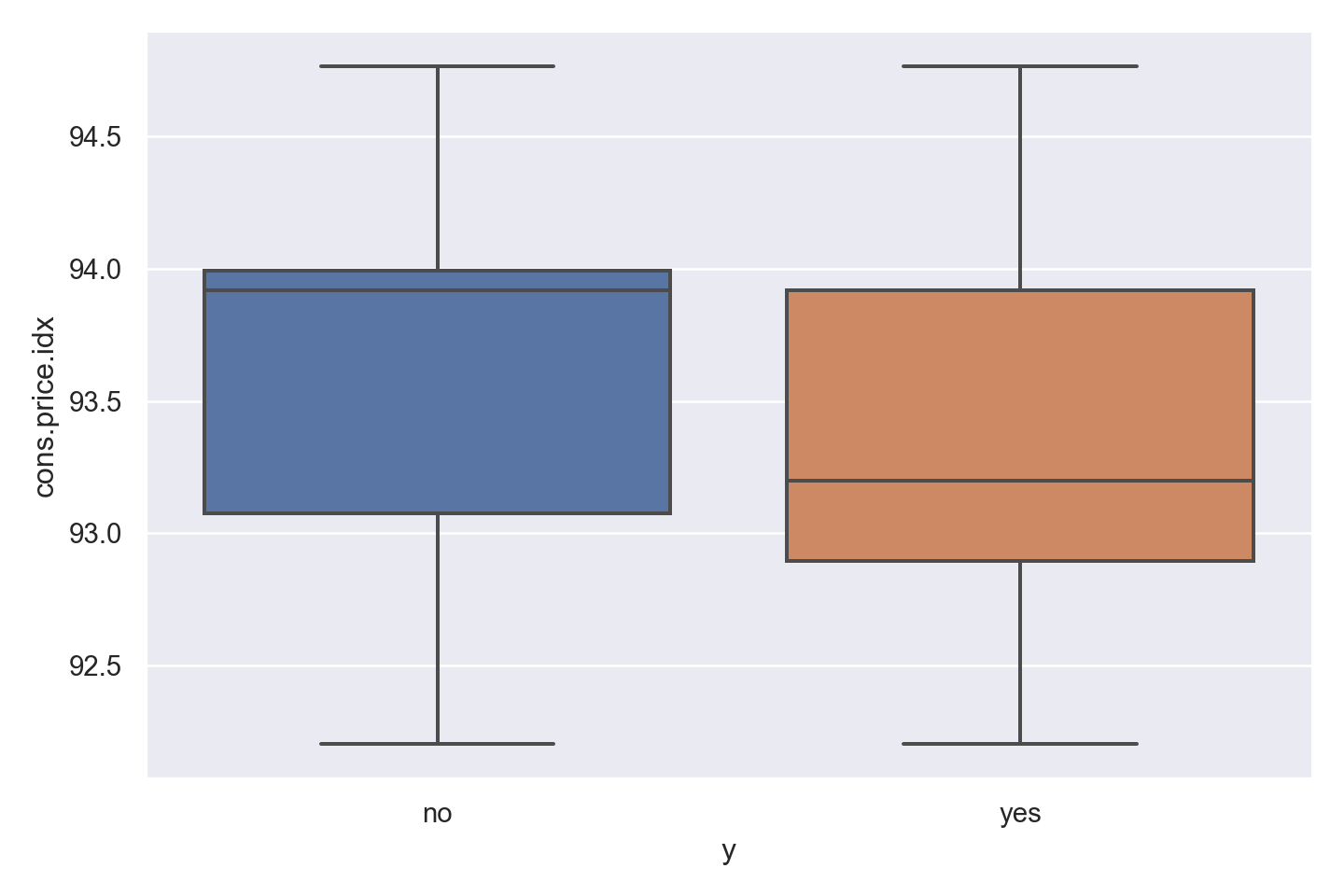

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=cons.price.idx))

p=sns.displot(data_bank_marketing, x="cons.price.idx", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

p=sns.catplot(data=data_bank_marketing, x="y", y="cons.price.idx", kind="box", height = 5, aspect = 1.5)

plt.show()

data1=rename(data, "cons.price.idx" => "cons_price_idx");

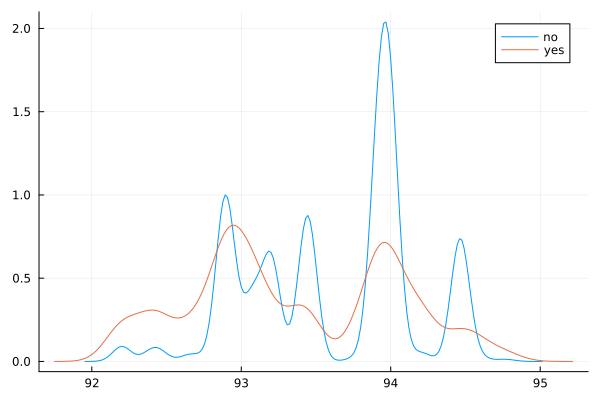

@df data1 density(:cons_price_idx, group = (:y))

Observations

There is not much variation in the data,other than two outliers (perhaps data entry errors?)

‘yes’ outcome is associated with a slightly lower price index.

cons.conf.idx

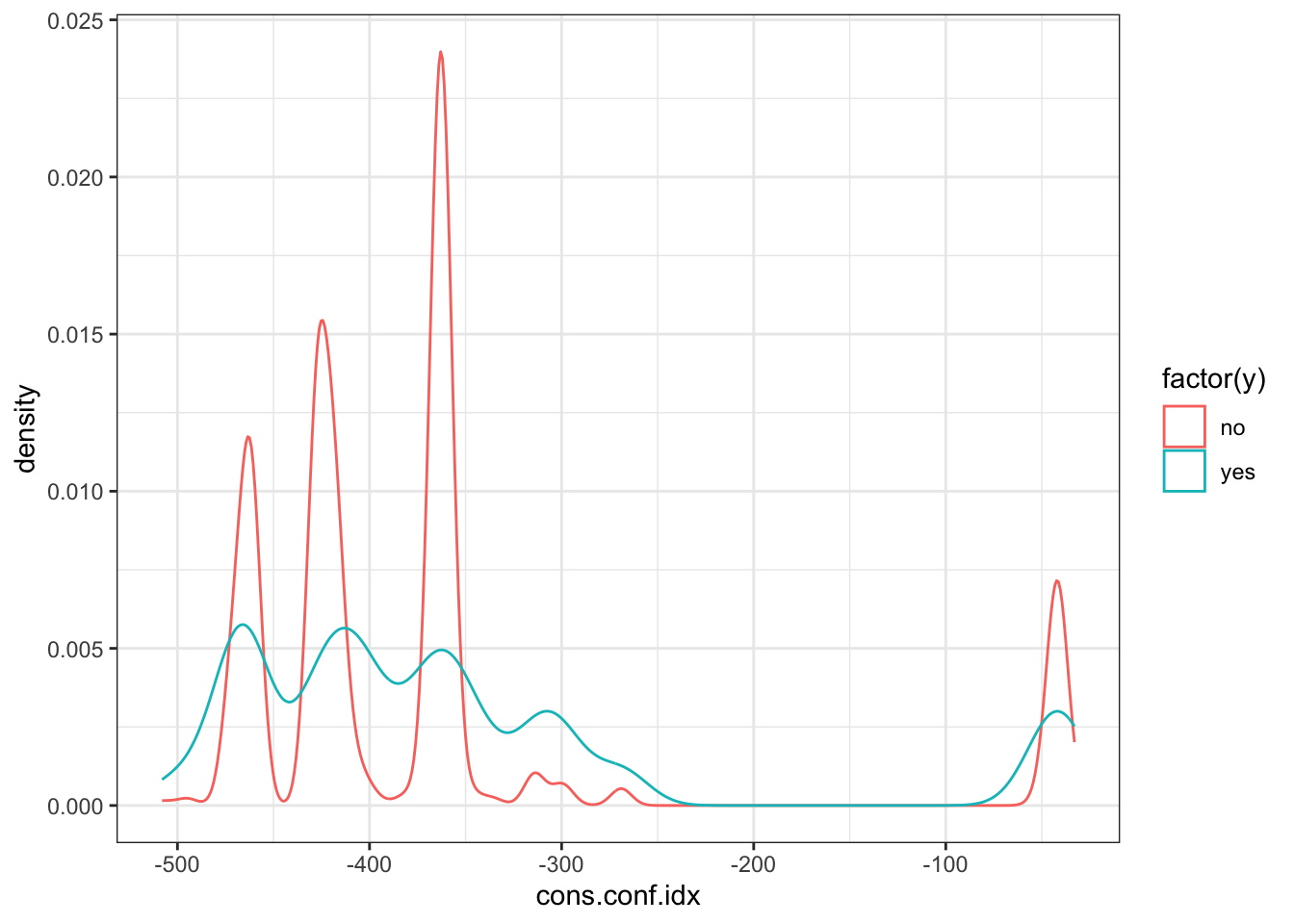

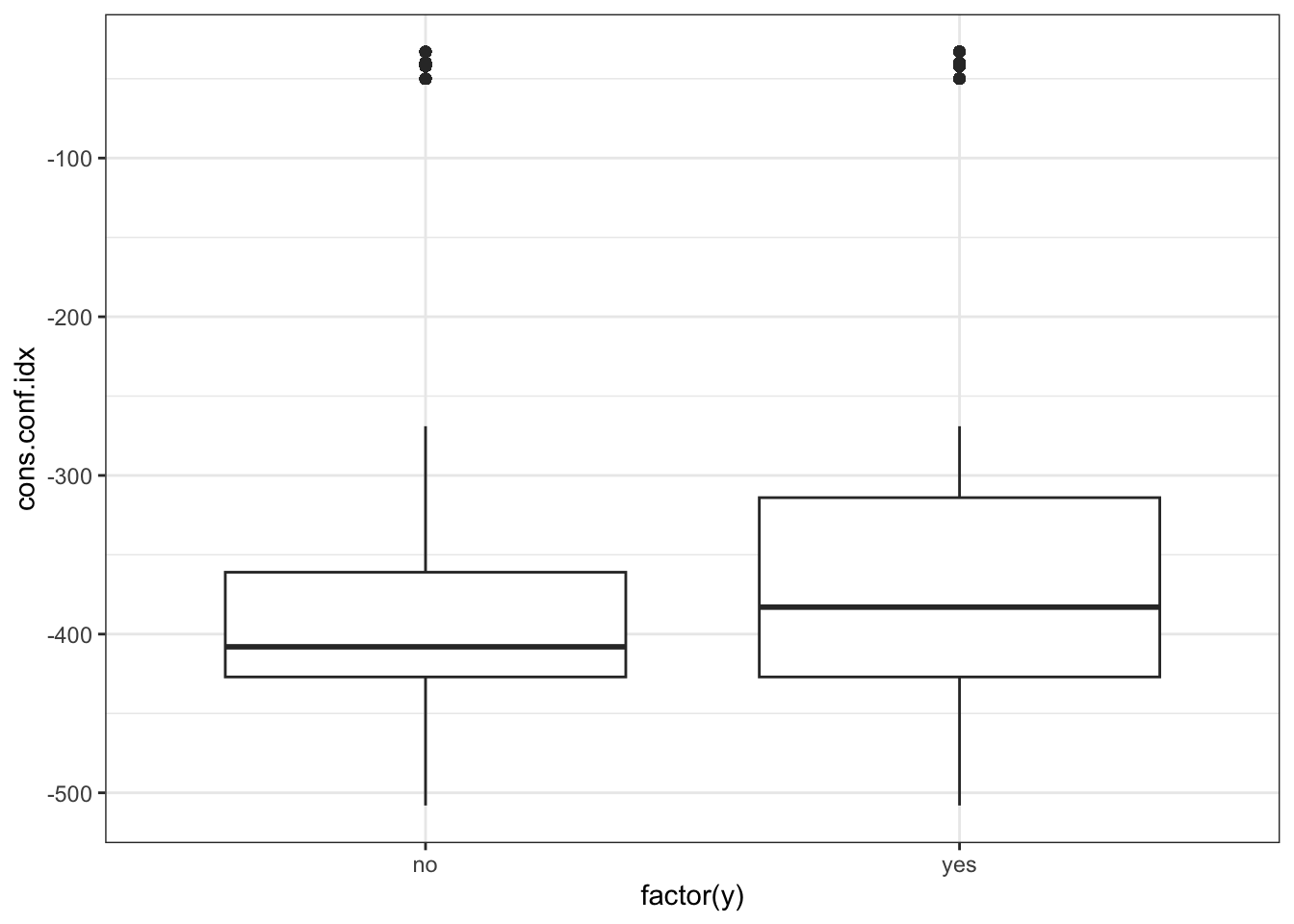

ggplot(data_bank_marketing) + geom_density(aes(x=cons.conf.idx, color=factor(y)))

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=cons.conf.idx))

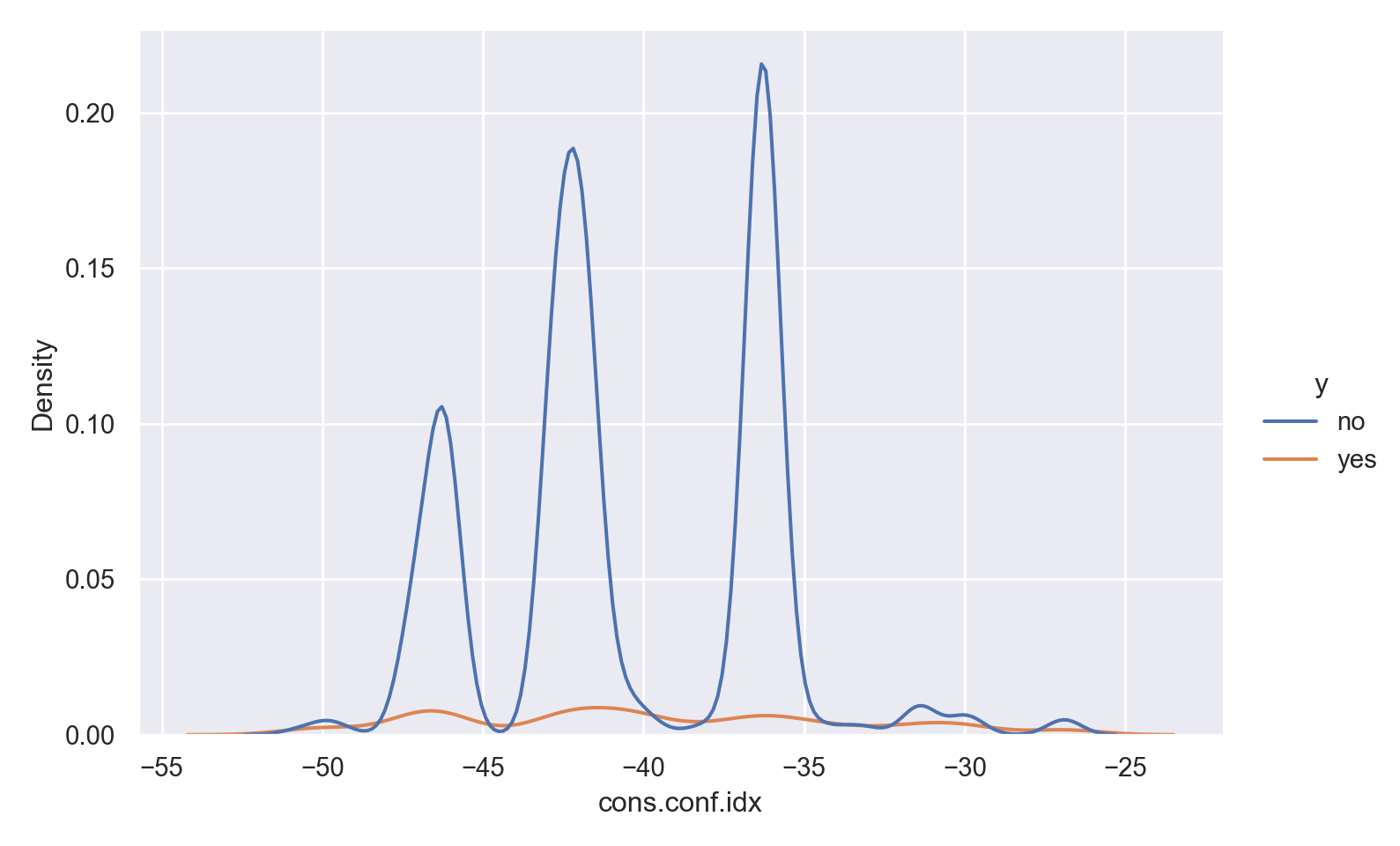

p=sns.displot(data_bank_marketing, x="cons.conf.idx", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

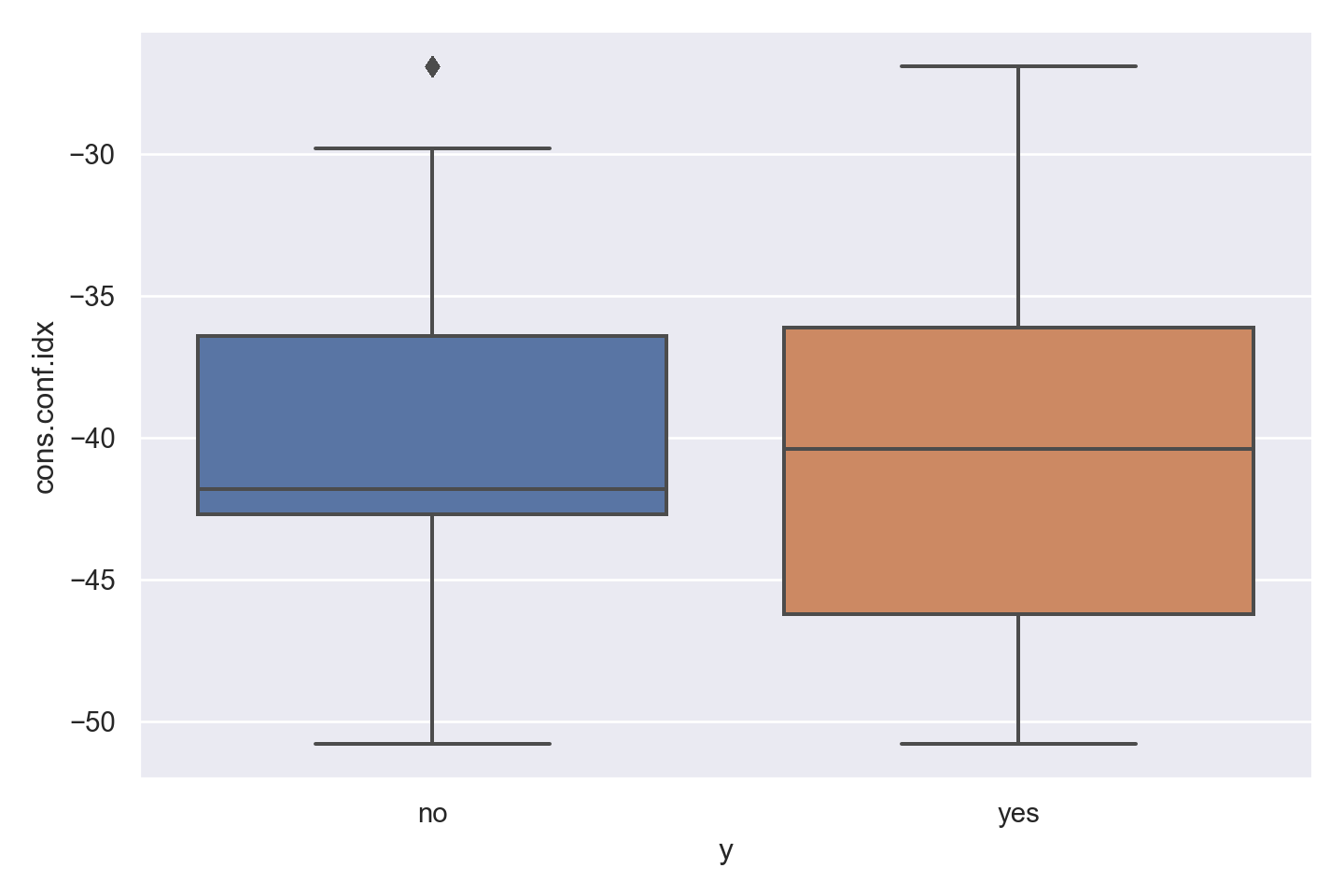

p=sns.catplot(data=data_bank_marketing, x="y", y="cons.conf.idx", kind="box", height = 5, aspect = 1.5)

plt.show()

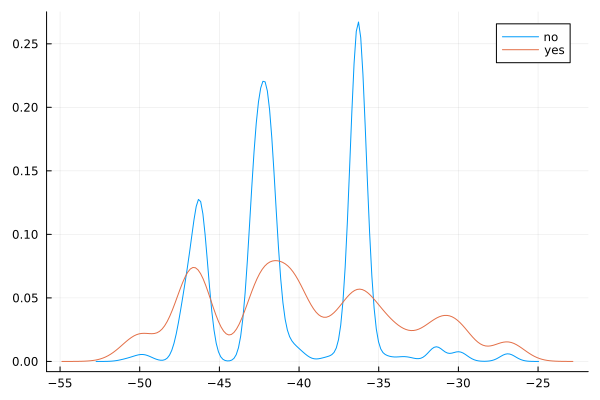

data1=rename(data, "cons.conf.idx" => "cons_conf_idx");

@df data1 density(:cons_conf_idx, group = (:y))

Observations

There is a strong association between confidence index and response - ‘yes’ outcomes show a higher index.

There is a multi-modal pattern in the data.

euribor3m

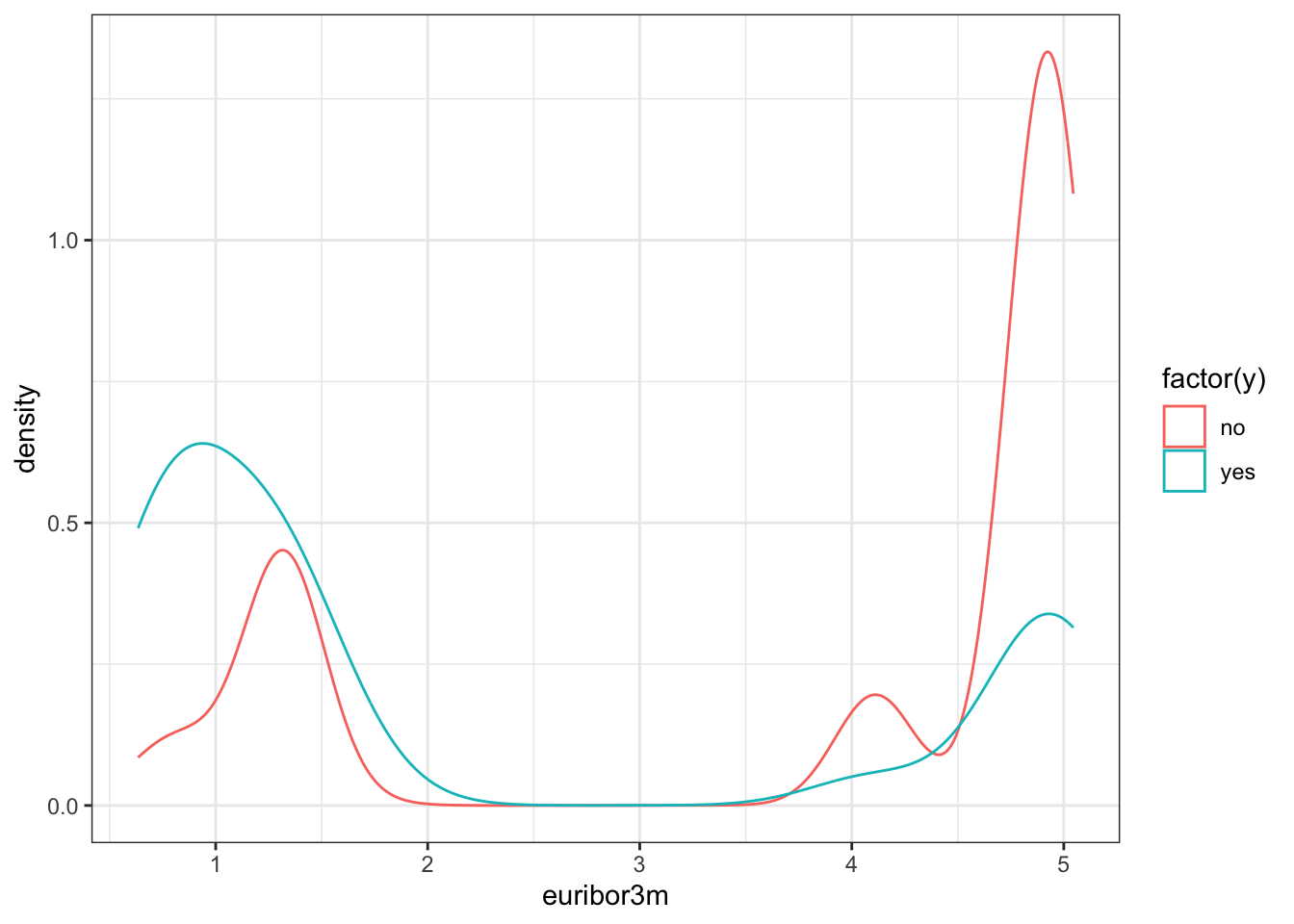

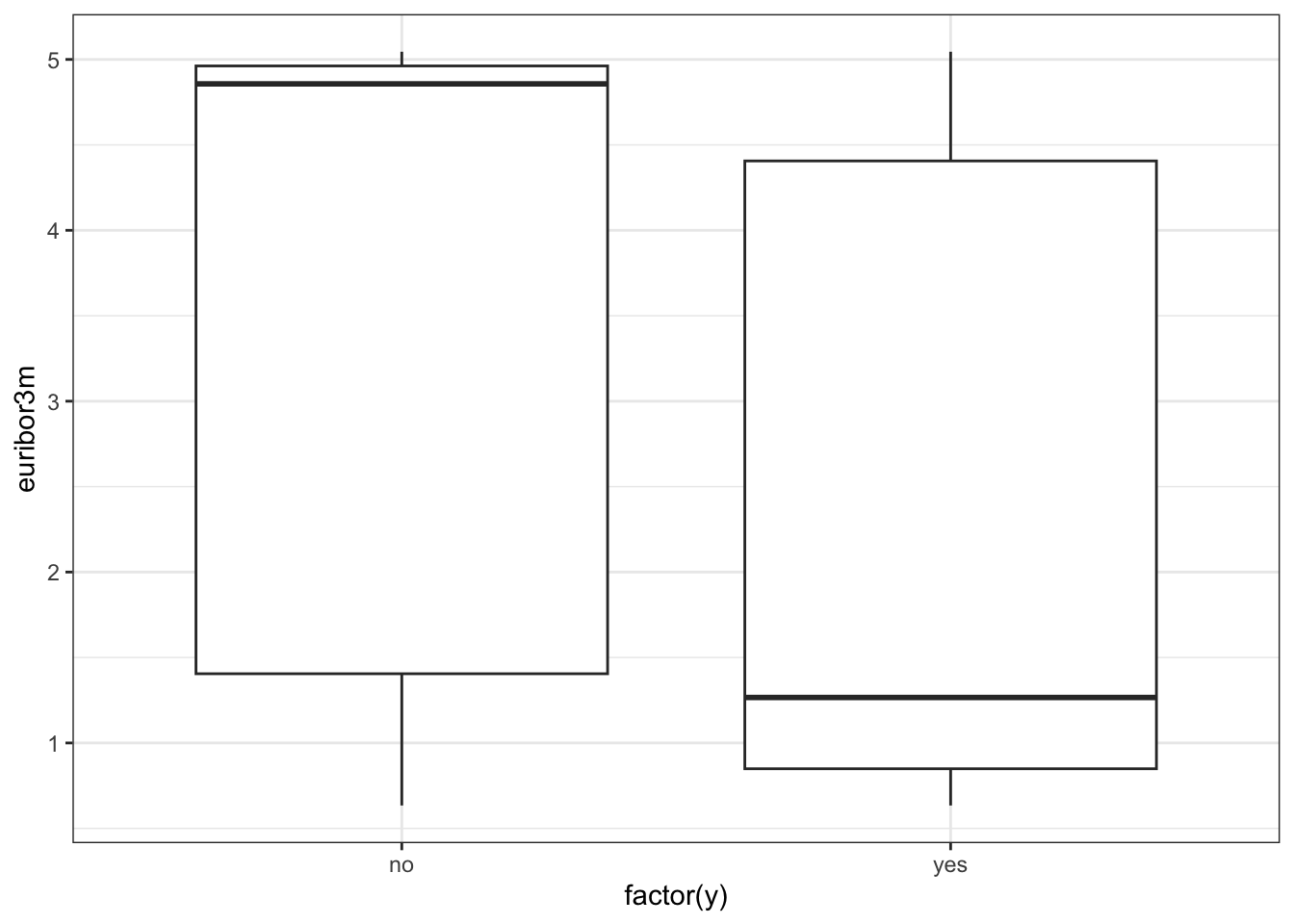

ggplot(data_bank_marketing) + geom_density(aes(x=euribor3m, color=factor(y)))

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=euribor3m))

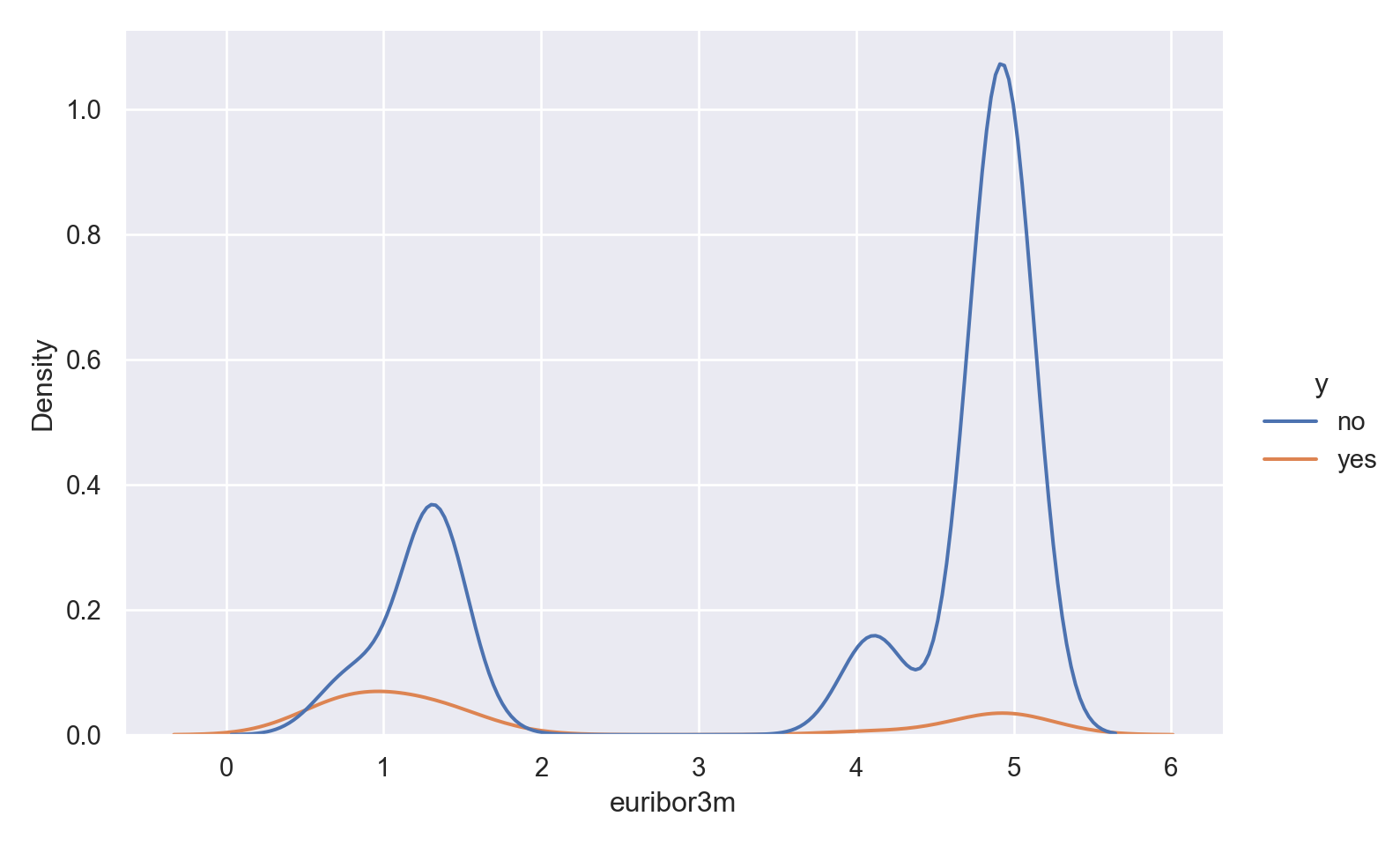

p=sns.displot(data_bank_marketing, x="euribor3m", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

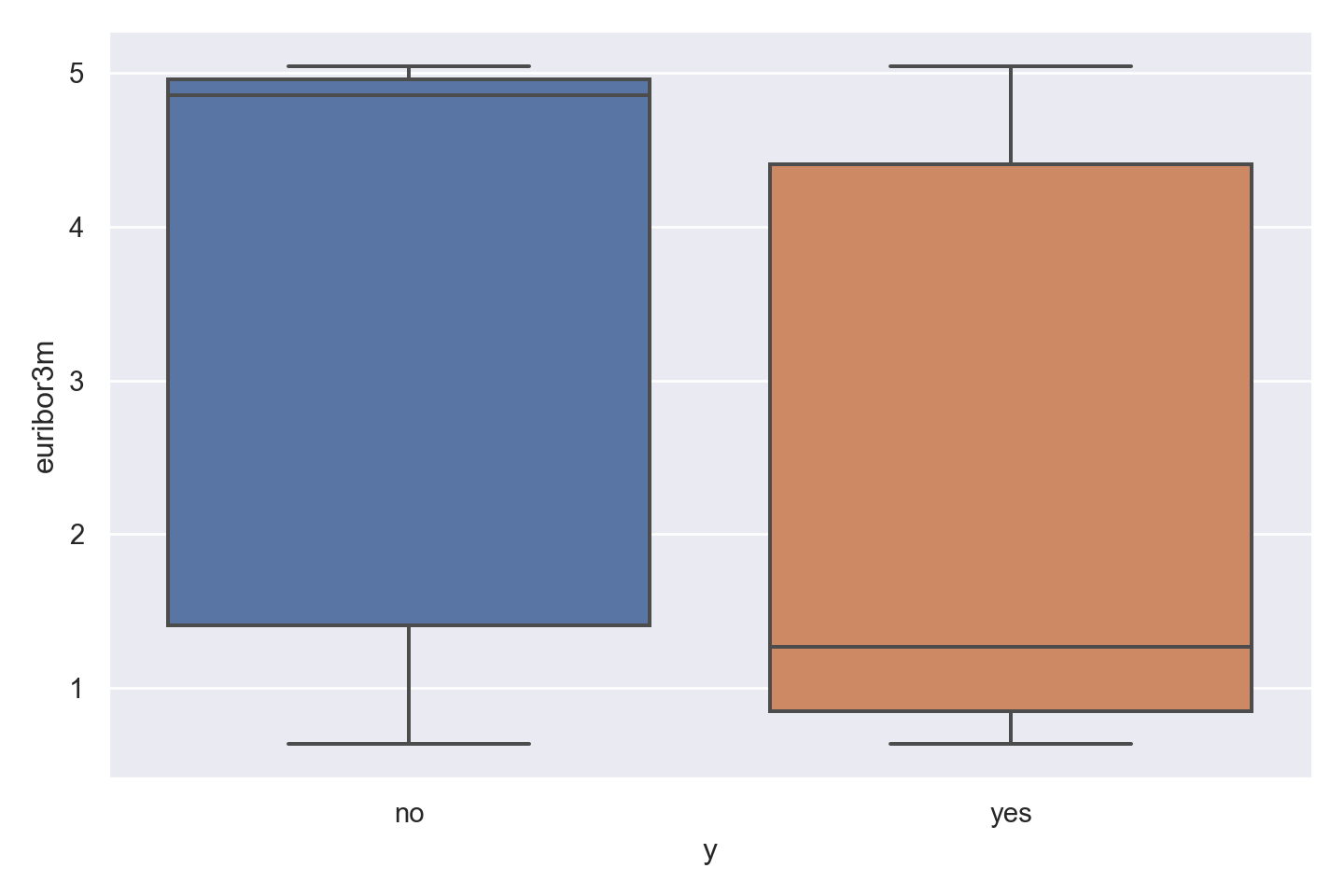

p=sns.catplot(data=data_bank_marketing, x="y", y="euribor3m", kind="box", height = 5, aspect = 1.5)

plt.show()

@df data density(:euribor3m, group = (:y))

Observations

There is a striking association between employment euribor3m interest rate and response - ‘yes’ outcomes show a much lower interest rate.

There is a multi-modal pattern in the data, with more records for 1 and 5.

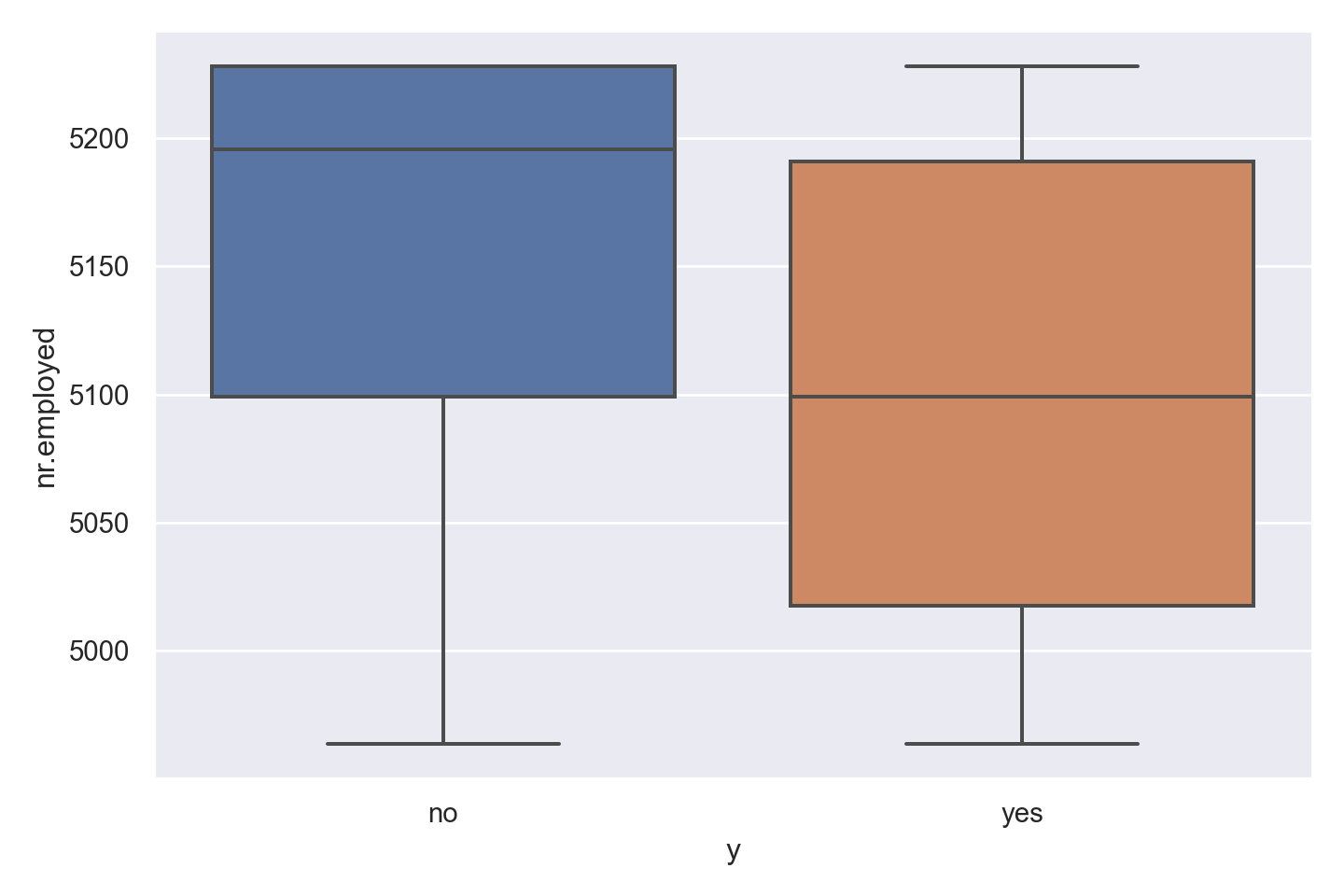

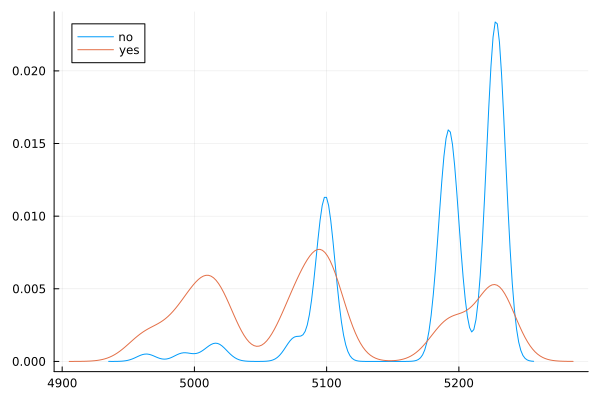

nr.employed

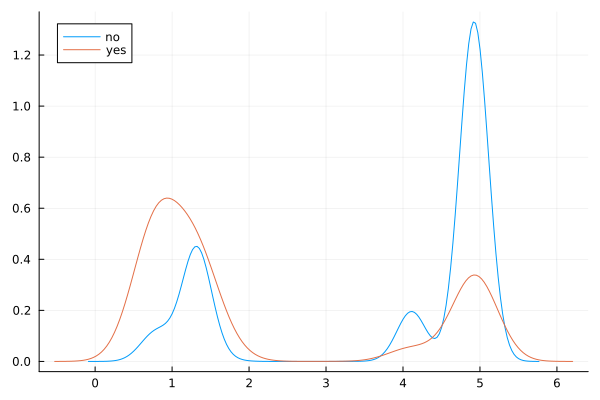

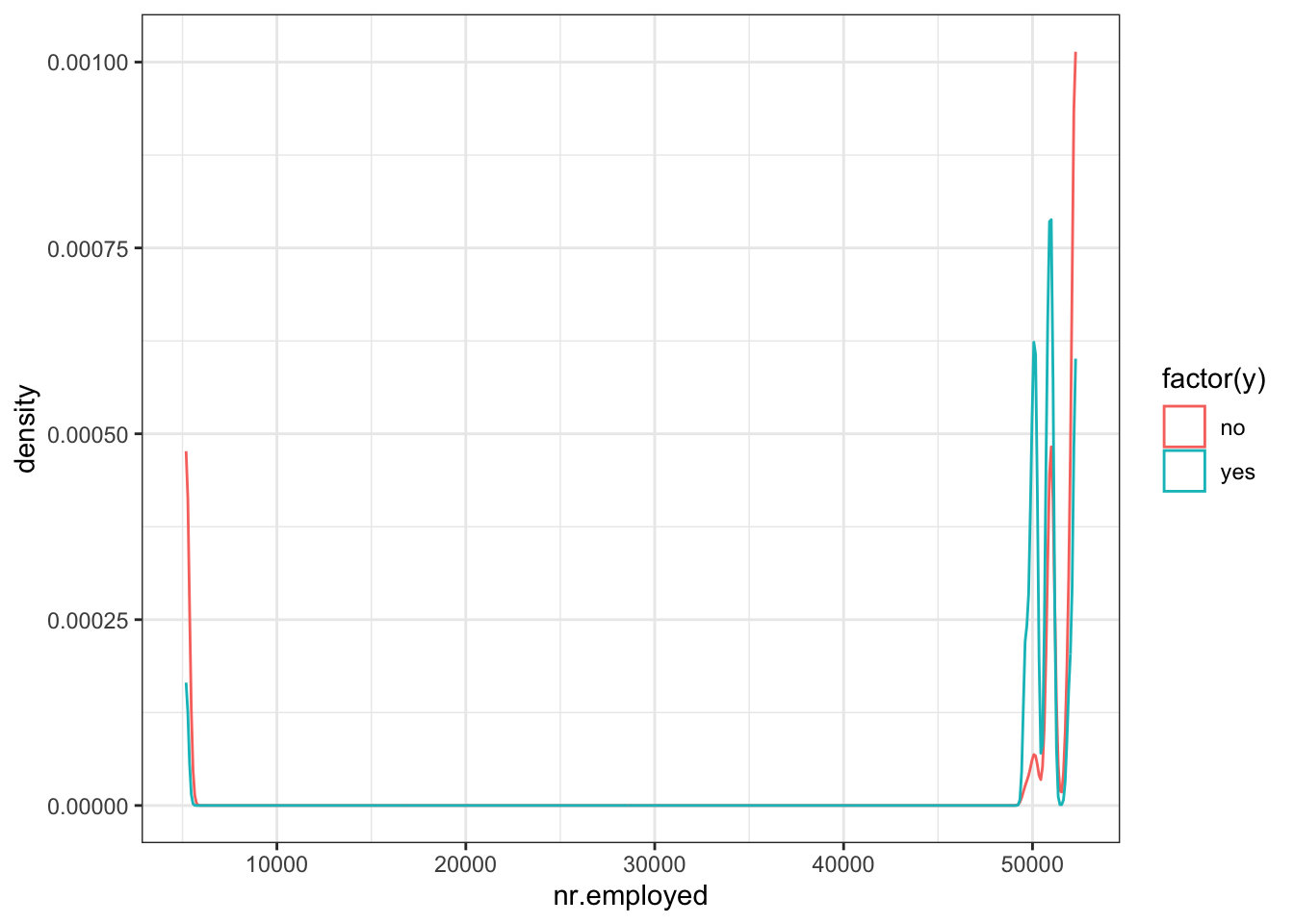

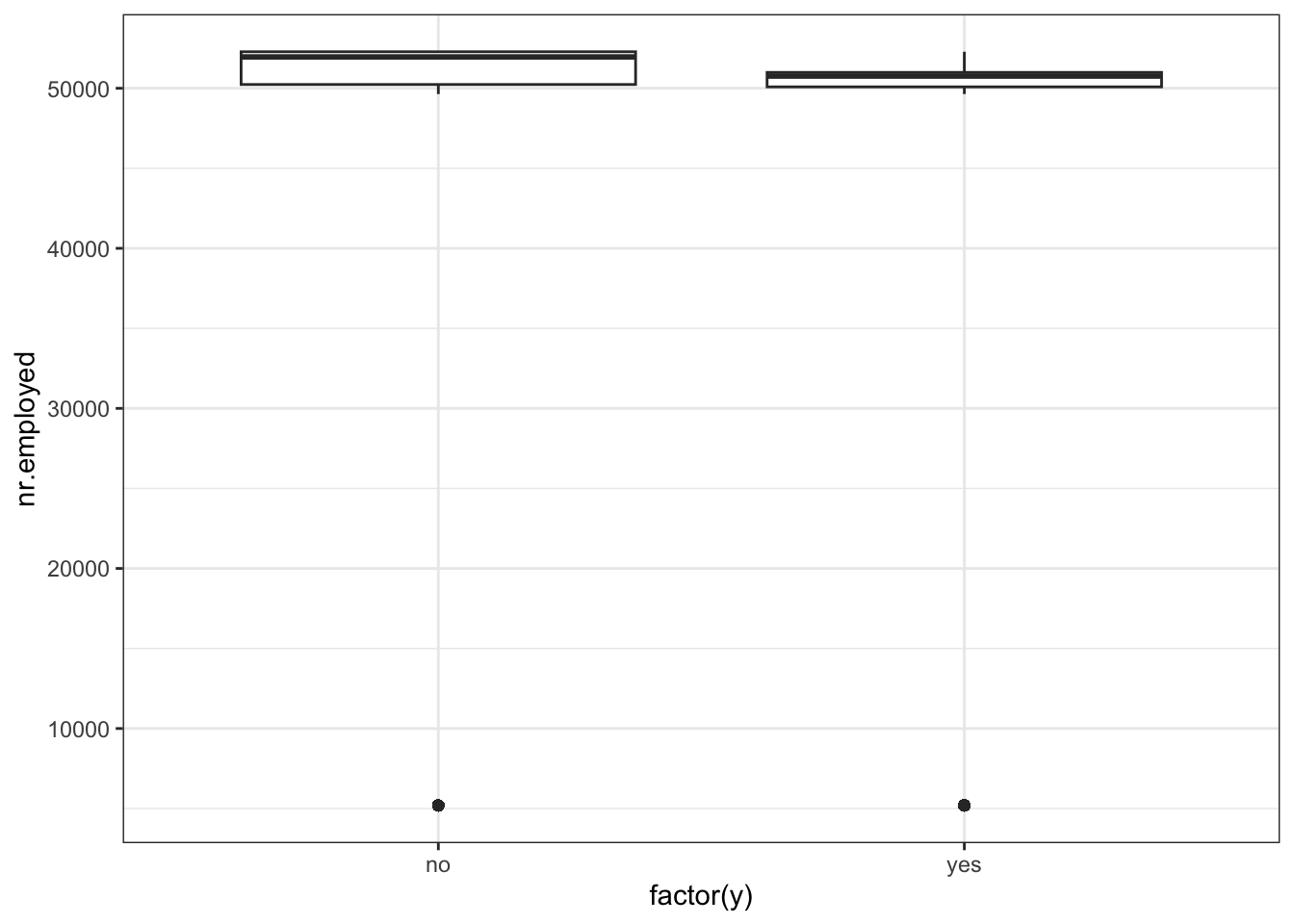

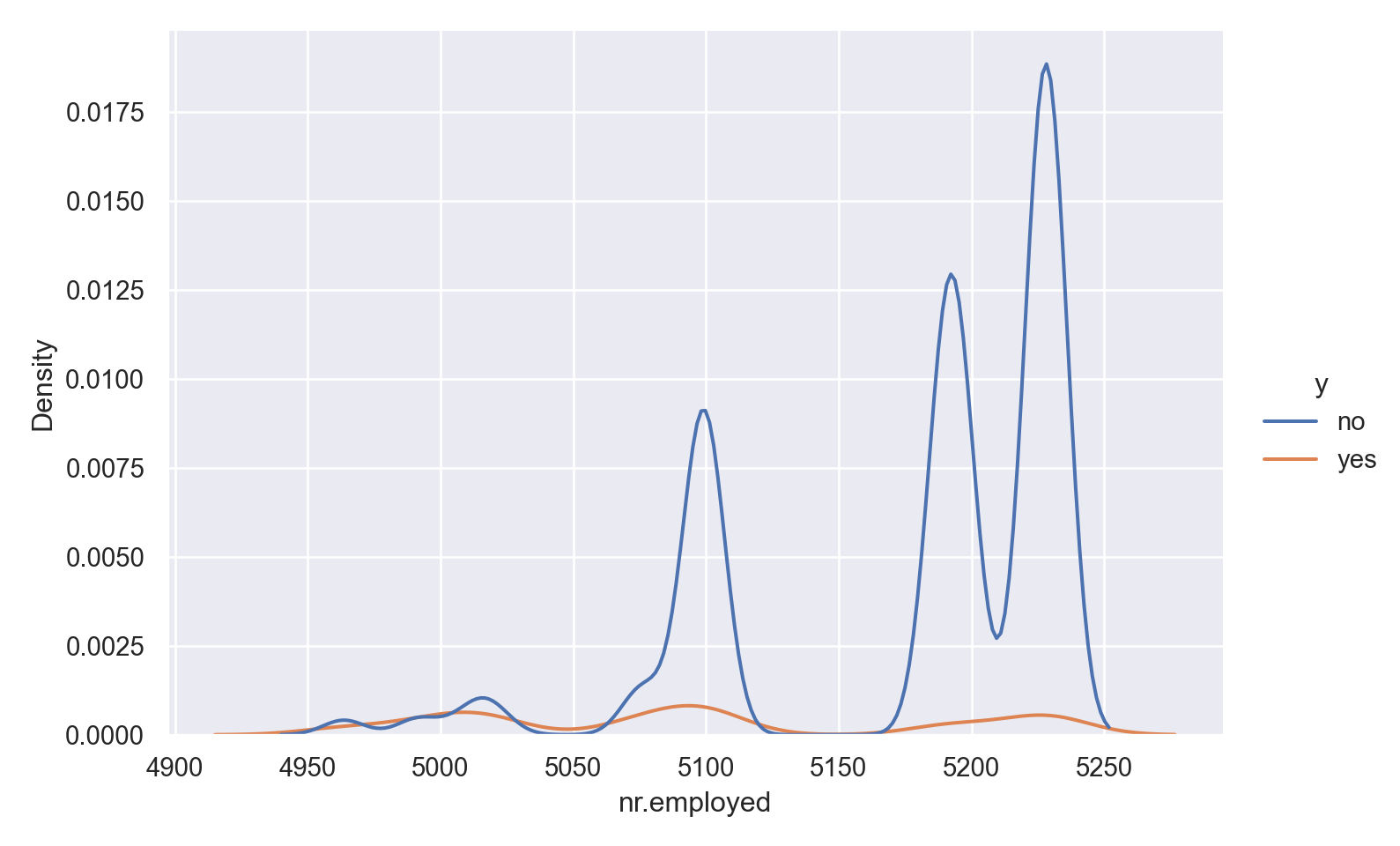

ggplot(data_bank_marketing) + geom_density(aes(x=nr.employed, color=factor(y)))

ggplot(data_bank_marketing) + geom_boxplot(aes(x=factor(y), y=nr.employed))

p=sns.displot(data_bank_marketing, x="nr.employed", hue="y", kind="kde", height = 5, aspect = 1.5)

plt.show()

p=sns.catplot(data=data_bank_marketing, x="y", y="nr.employed", kind="box", height = 5, aspect = 1.5)

plt.show()

data1 = rename!(data, "nr.employed" => "nr_employed");

@df data density(:nr_employed, group = (:y))

Observations

Curiously, ‘yes’ outcome is associated with a lower employment number.

There are two outliers in the data.

Categorical Attributes

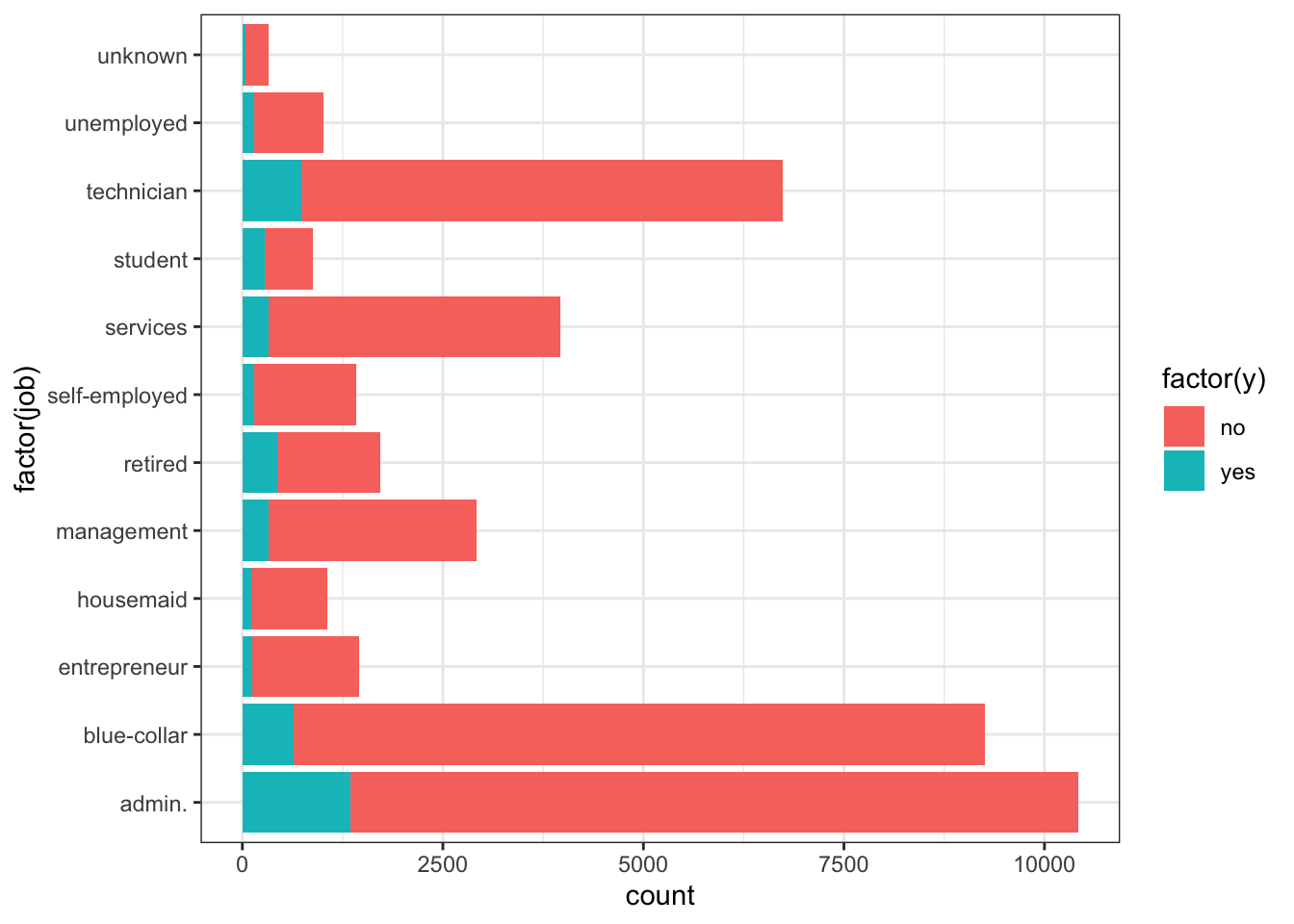

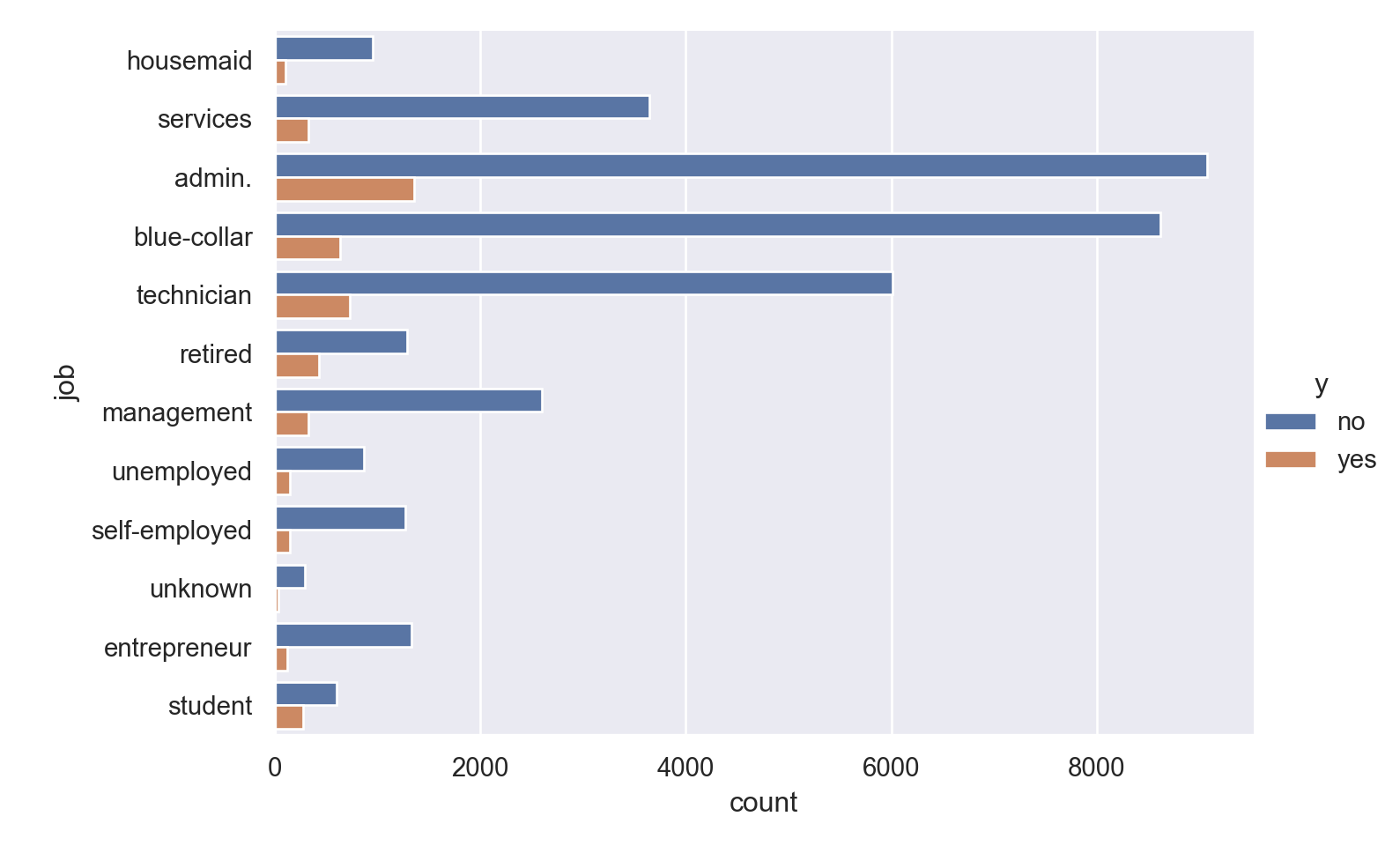

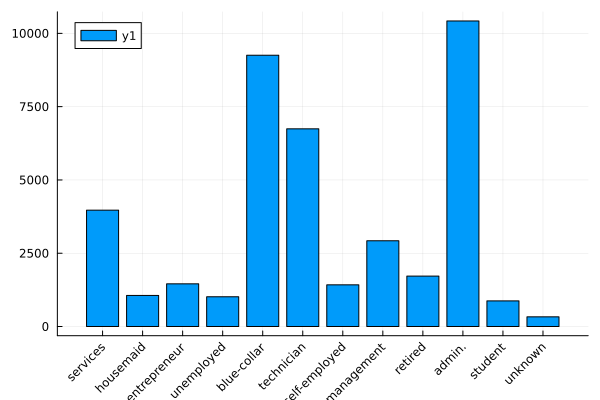

job

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(job), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="job", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

bar(countmap(data.job), xrotation=45)

Observations

admin, blue-collar and technicians make up the majority of the people called.

There is higher percentage of yes outcome for students and retired persons, but the overall proportion of these categories is low (without being insignificant)

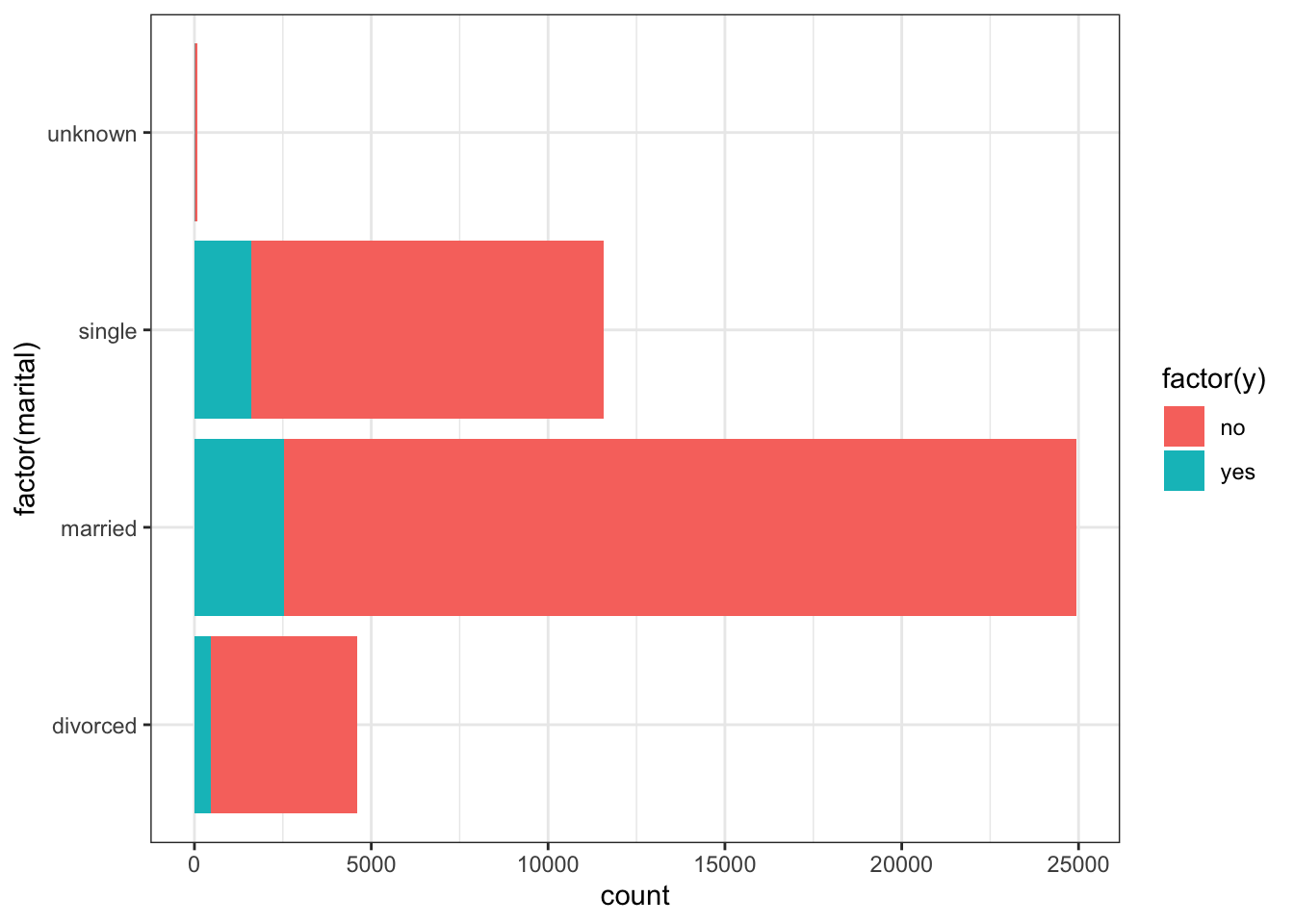

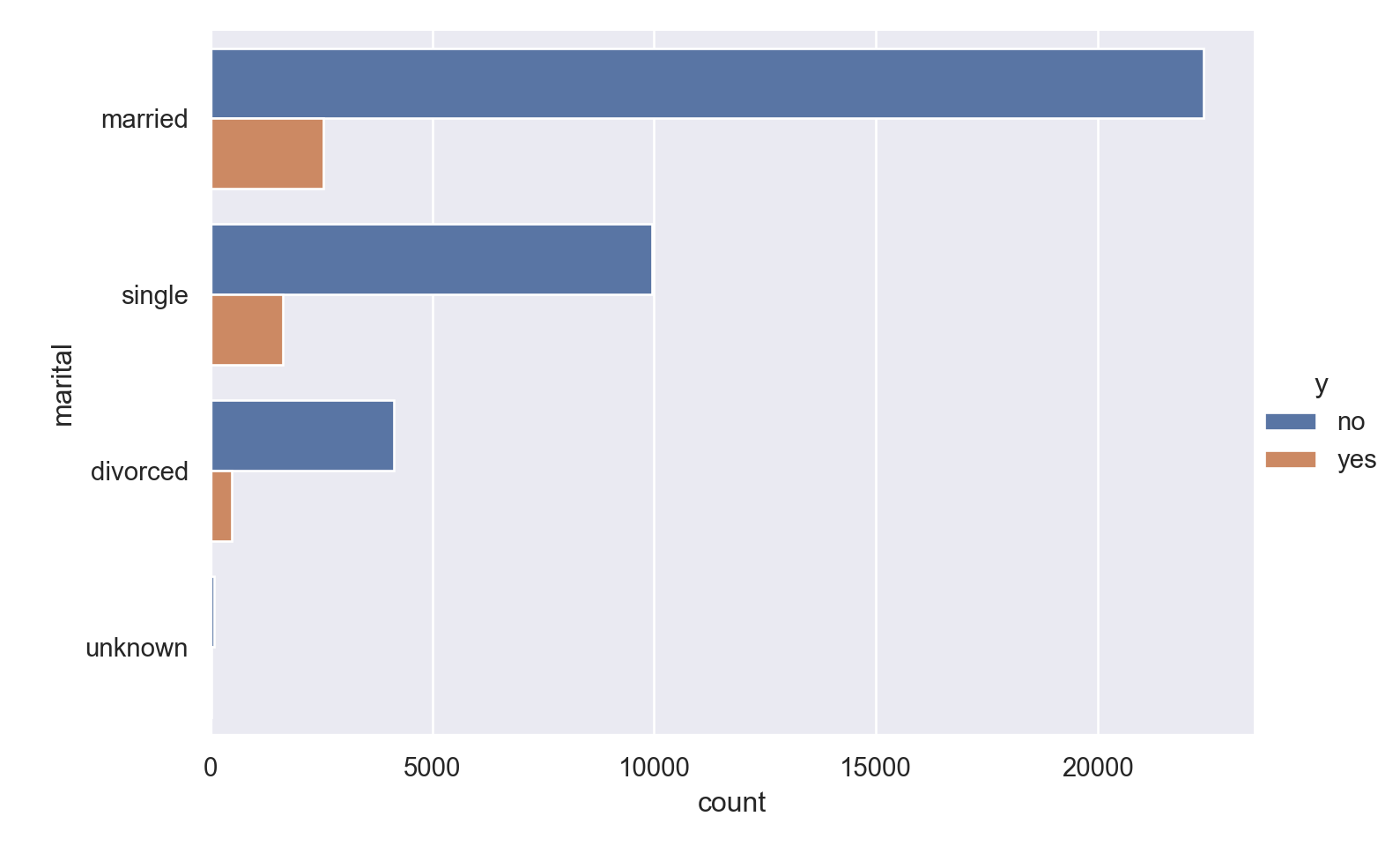

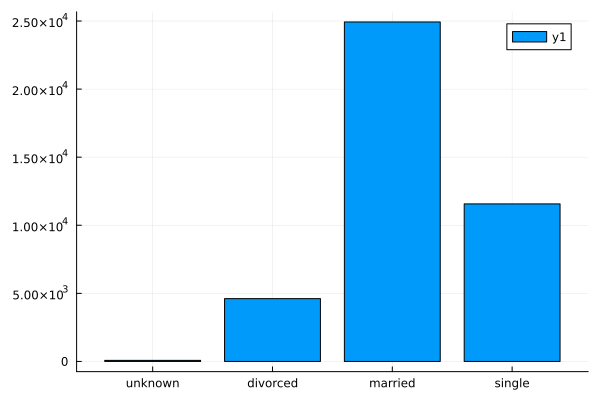

marital

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(marital), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="marital", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

bar(countmap(data.marital))

Observations

More of the people are married.

People who are single (and not divorced) have a higher proportion of ‘yes’ response.

education

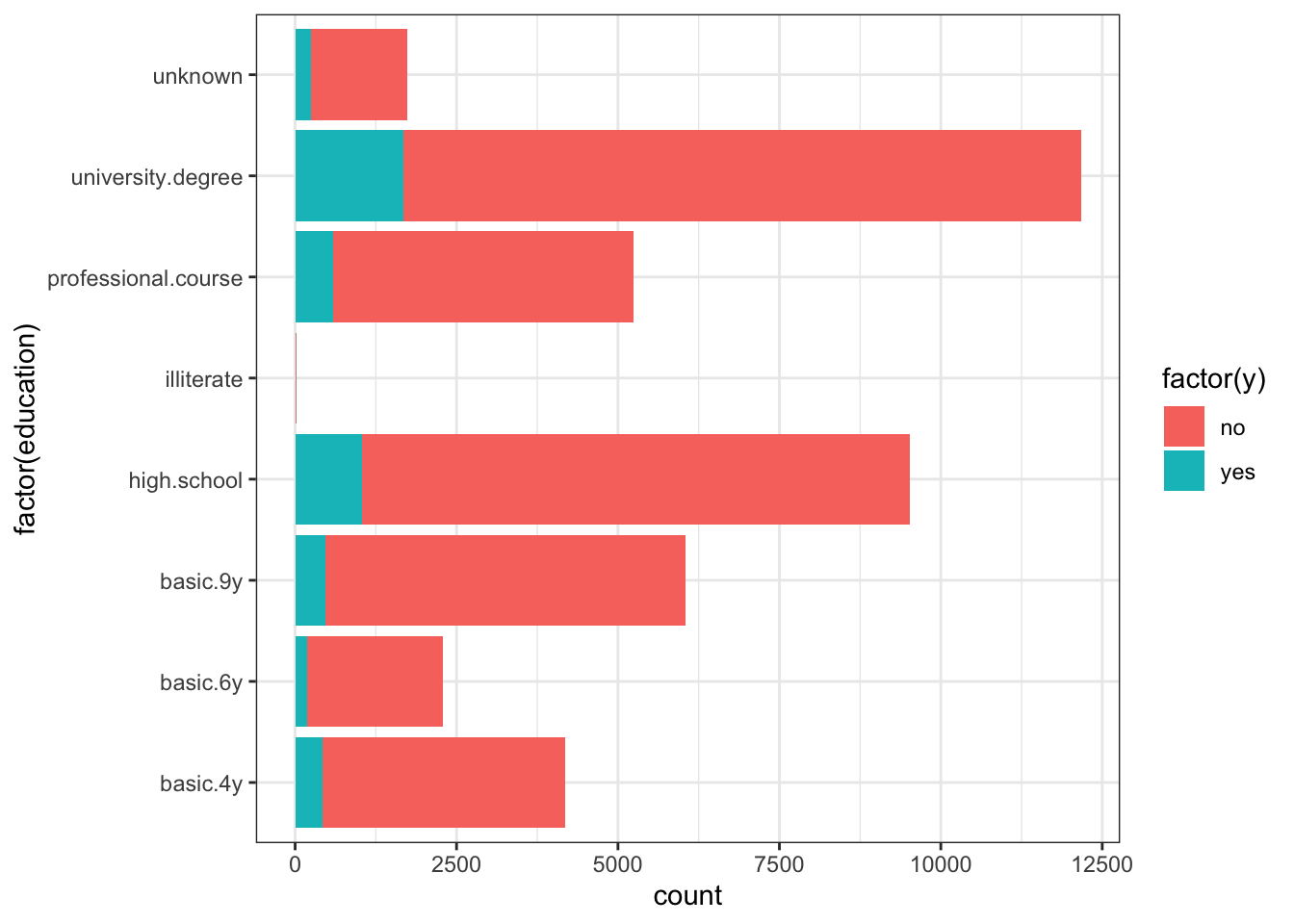

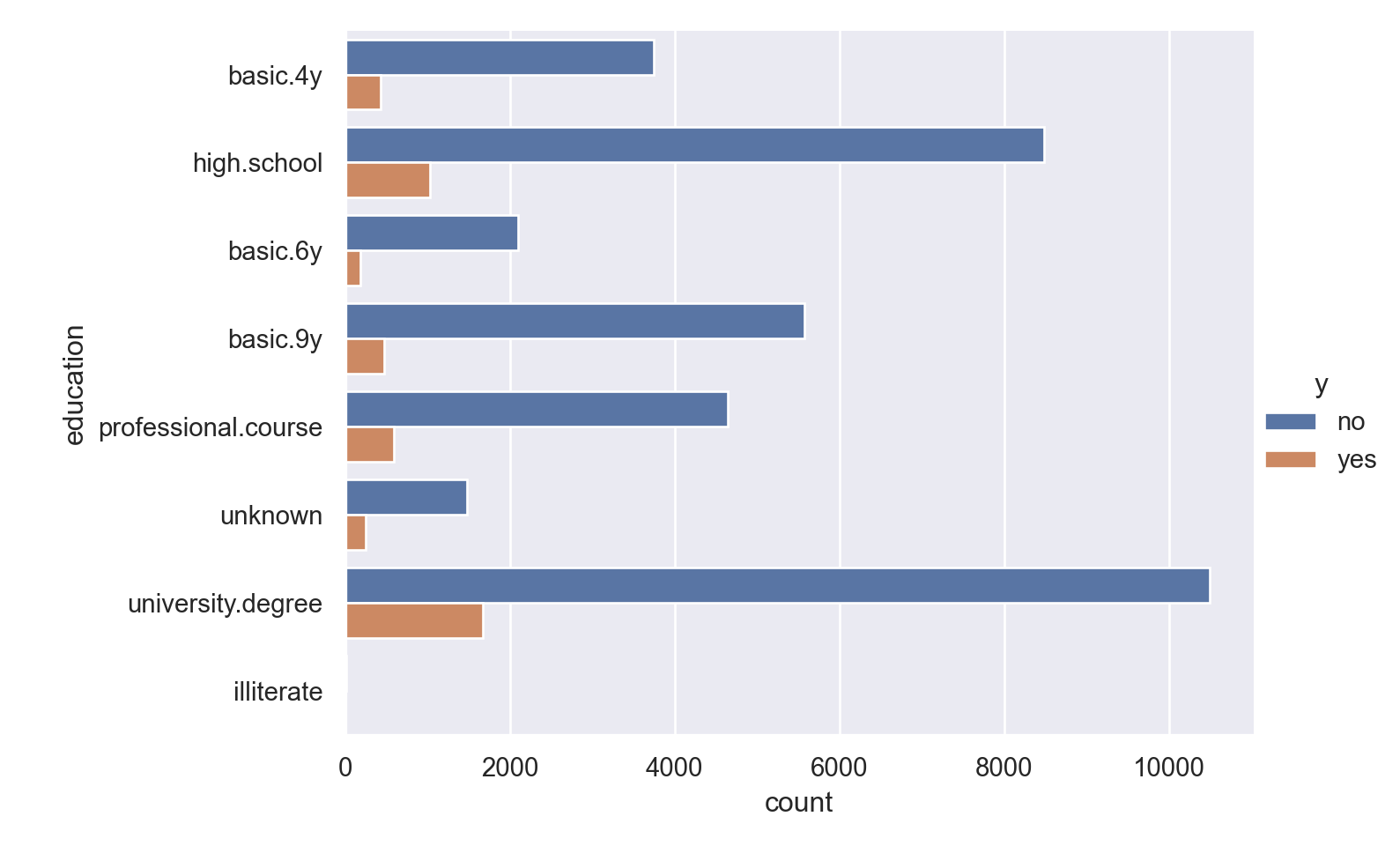

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(education), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="education", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

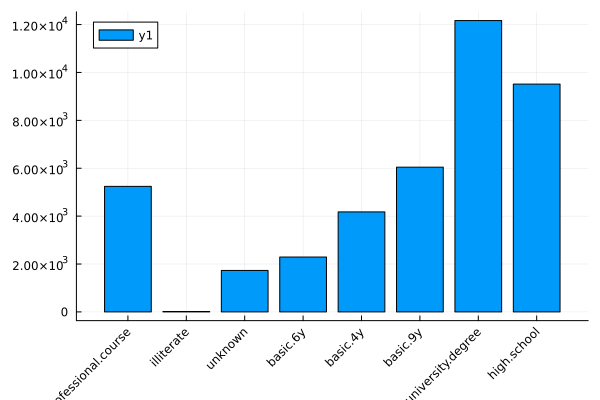

bar(countmap(data.education), xrotation=45)

Observations

Most people called have 9 years or more education; many have a university degree.

Those with university degree show a slightly higher proportion of ‘yes’ outcome (confirmed by the numerical inspection).

default

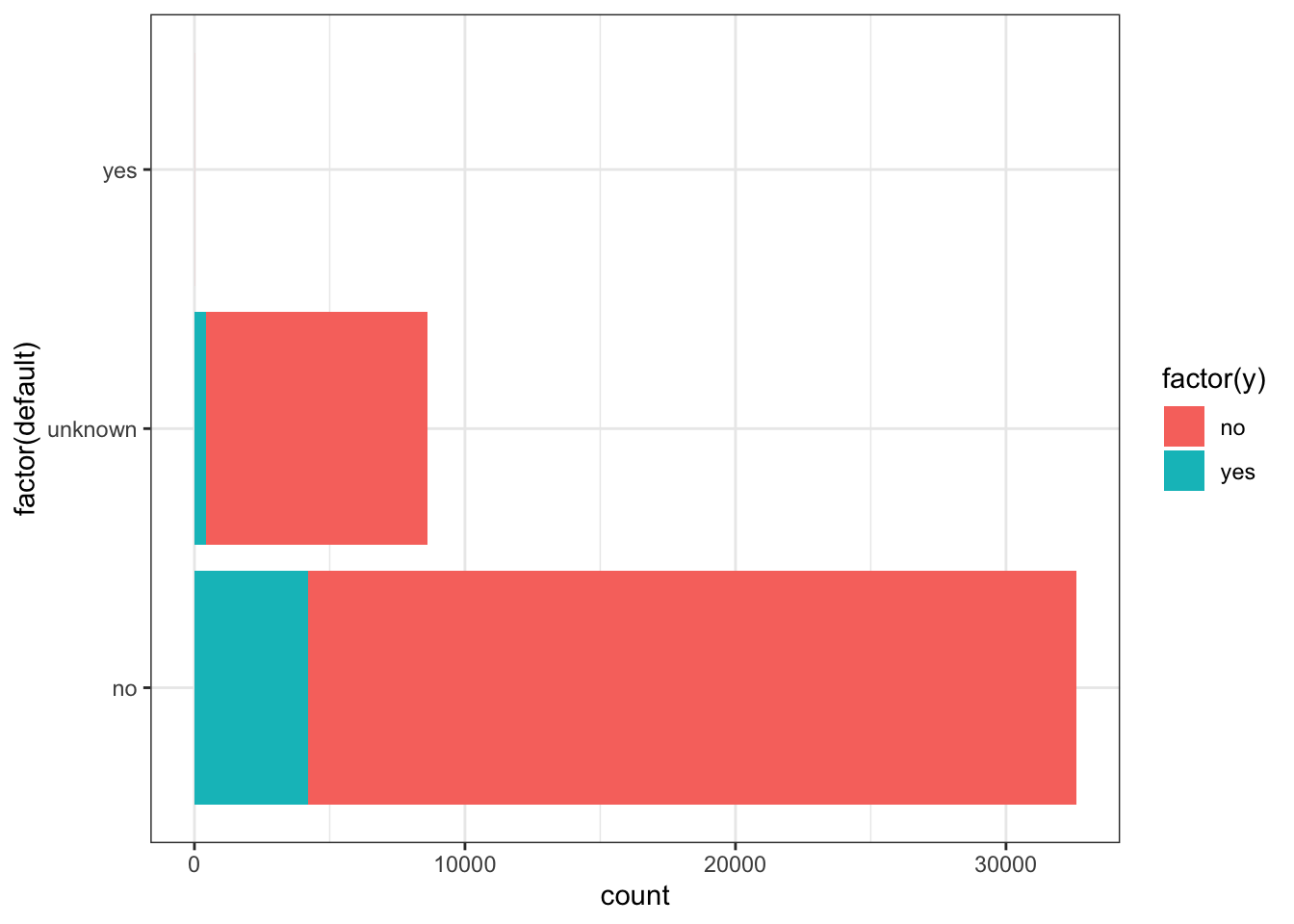

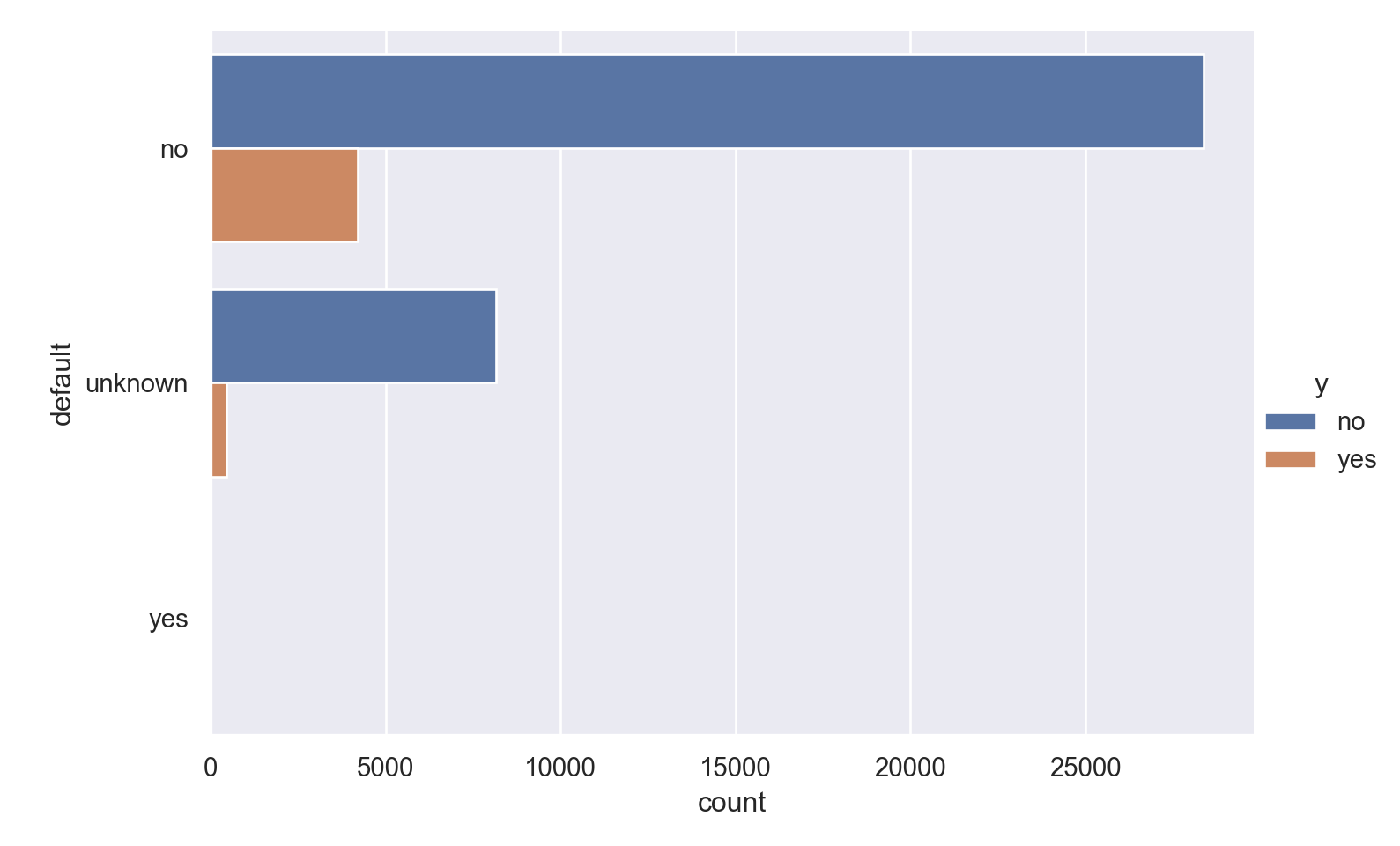

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(default), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="default", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

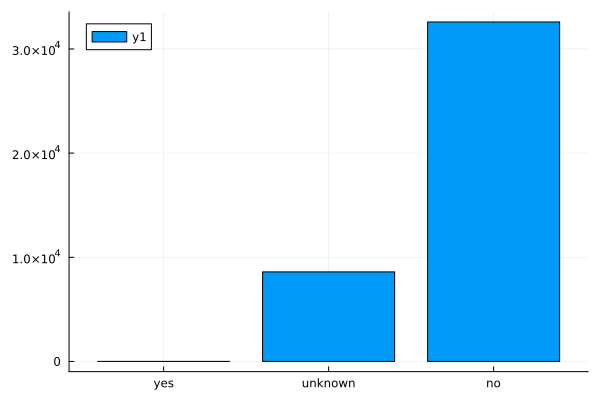

bar(countmap(data.default))

Observations

- A minuscule number of the people called have a loan default.

housing

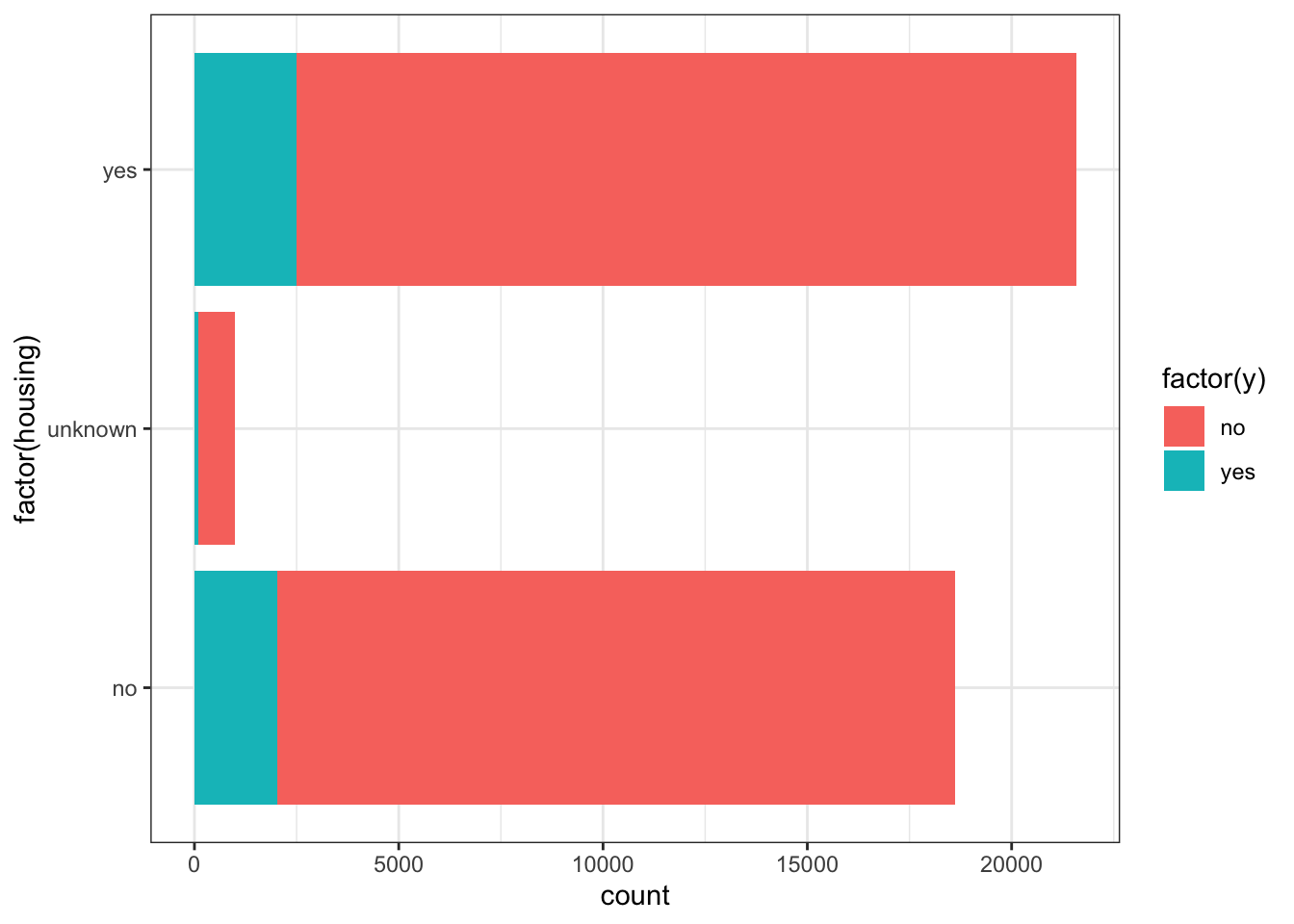

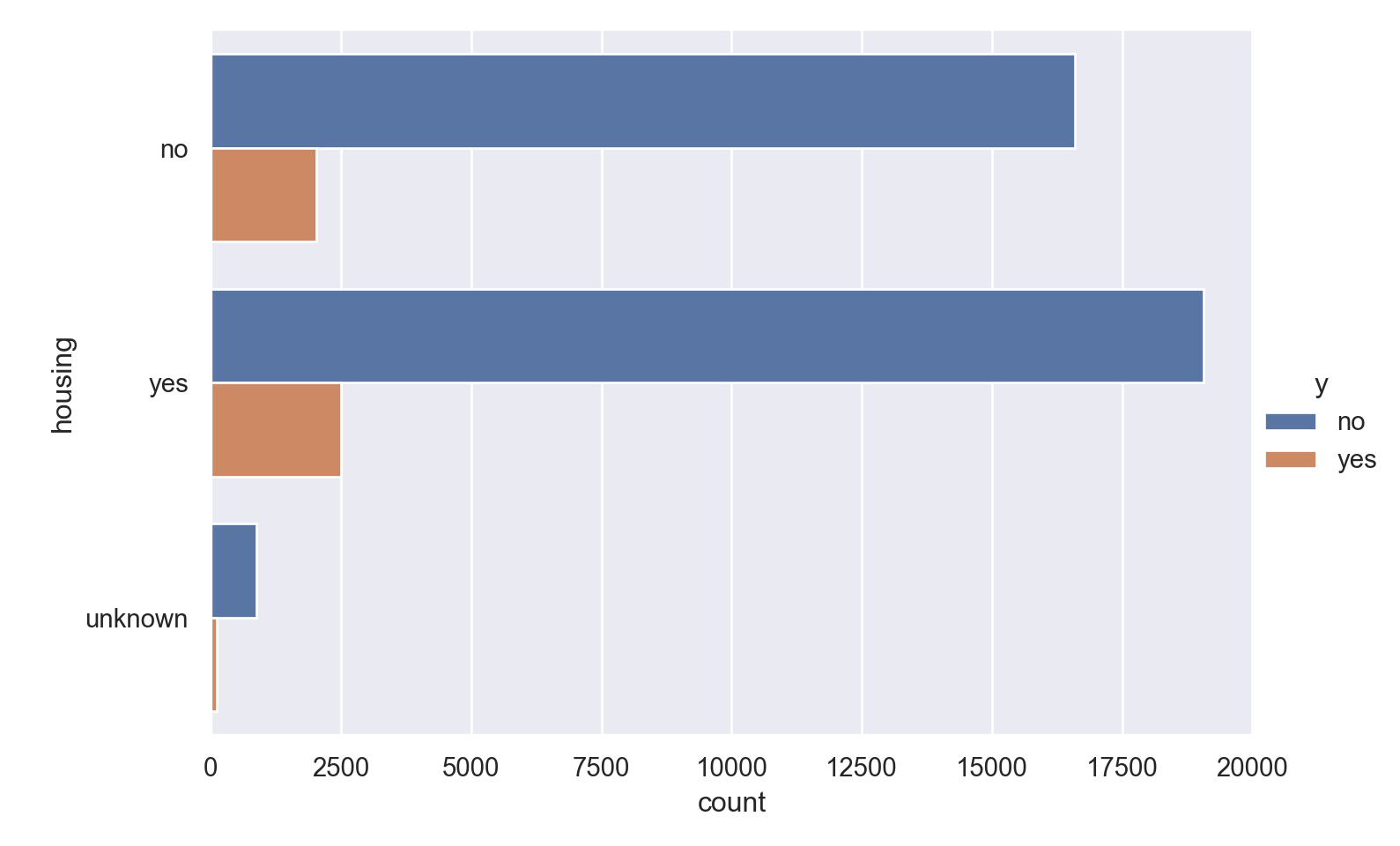

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(housing), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="housing", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

bar(countmap(data.housing))

Observations

- Slightly more number of people have housing.

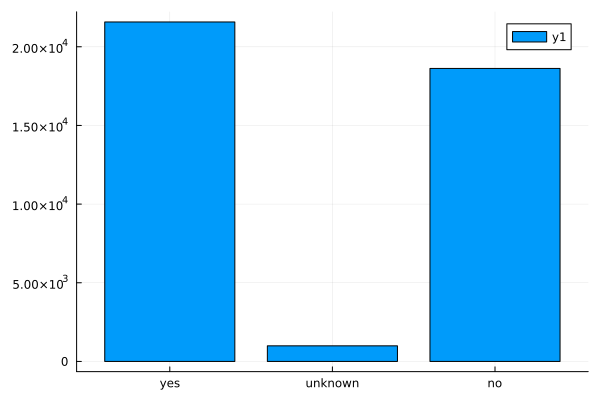

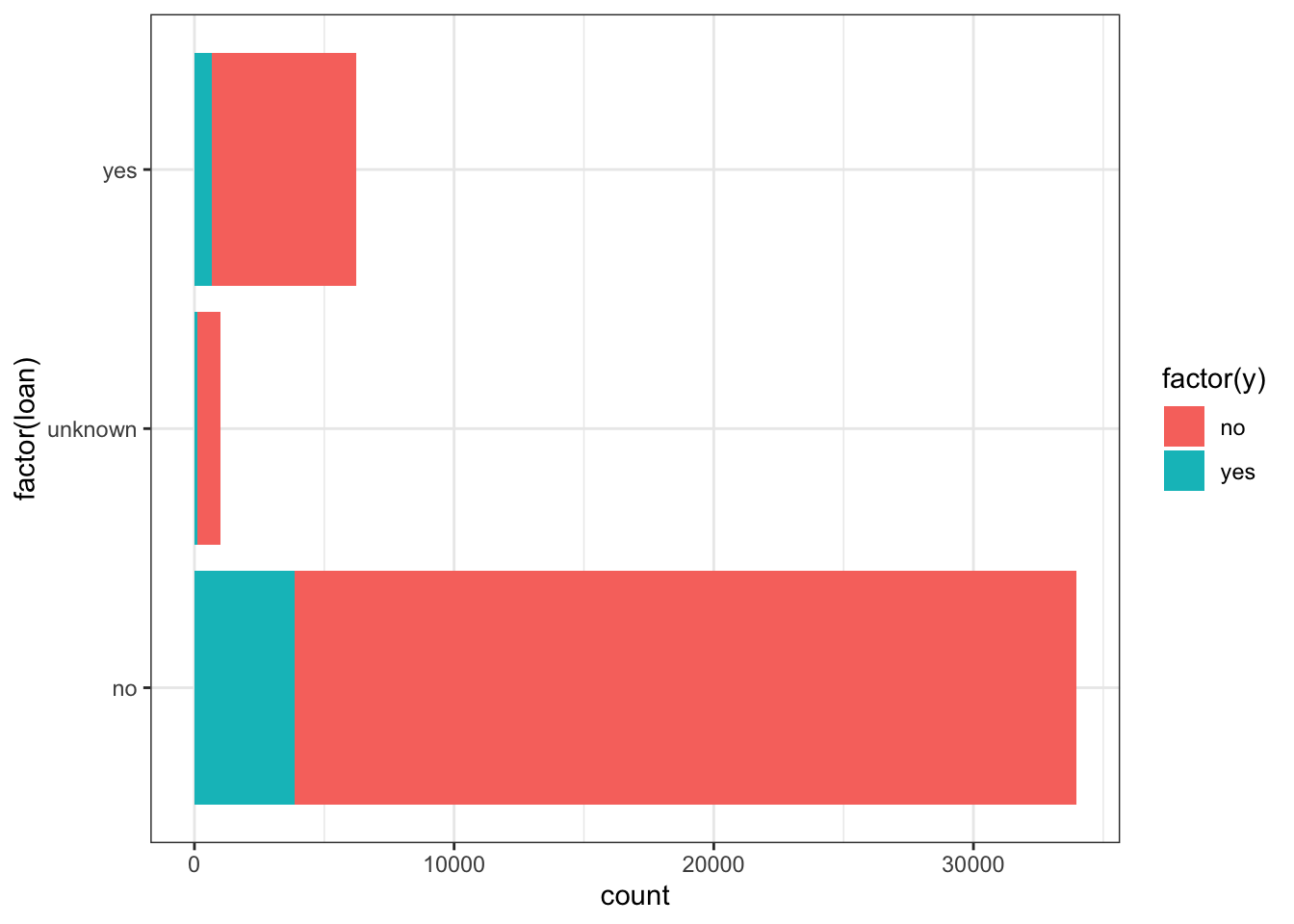

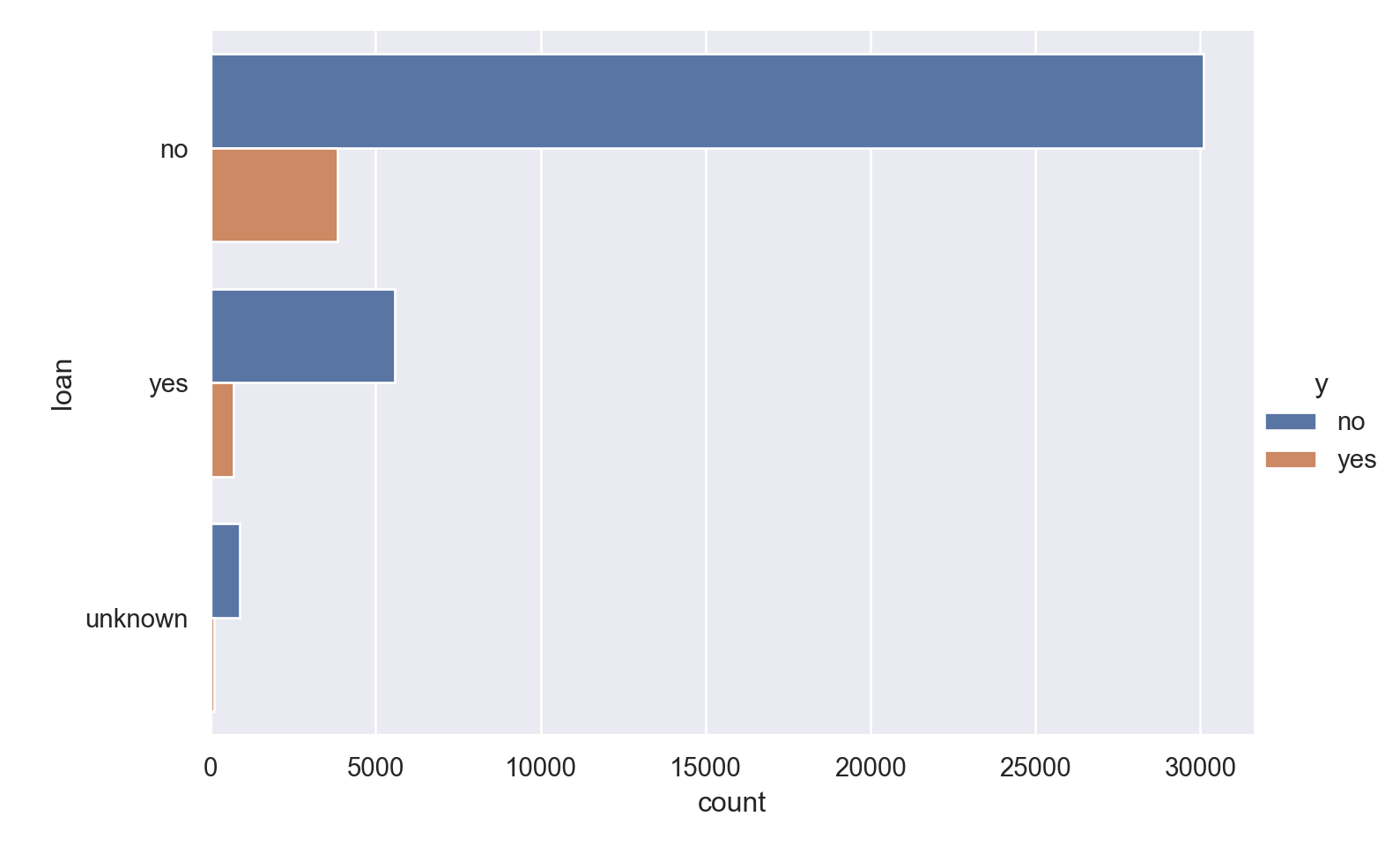

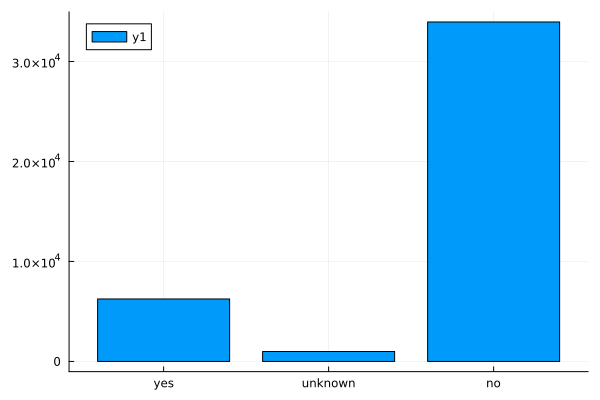

loan

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(loan), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="loan", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

display(bar(countmap(data.loan)))

contact

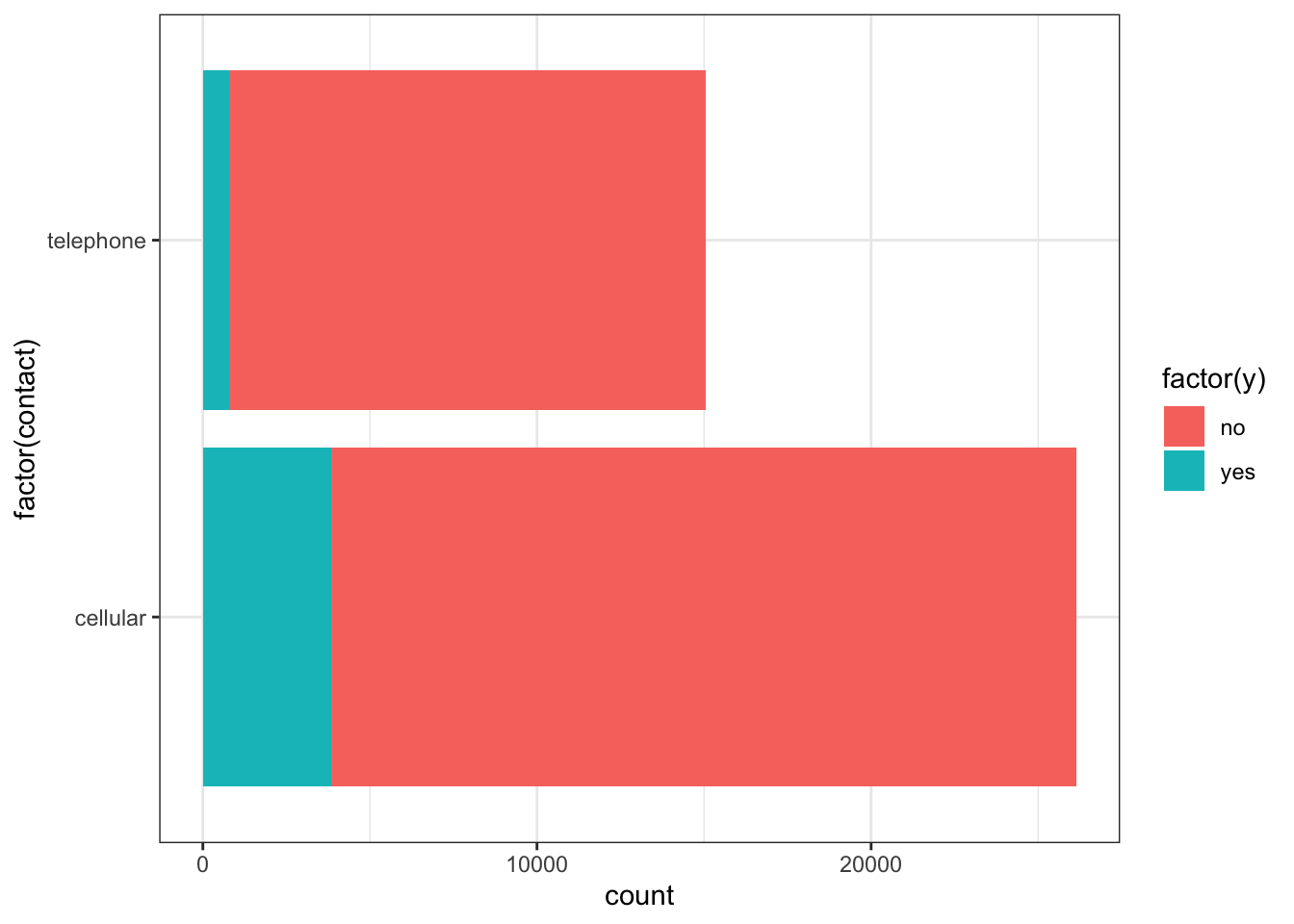

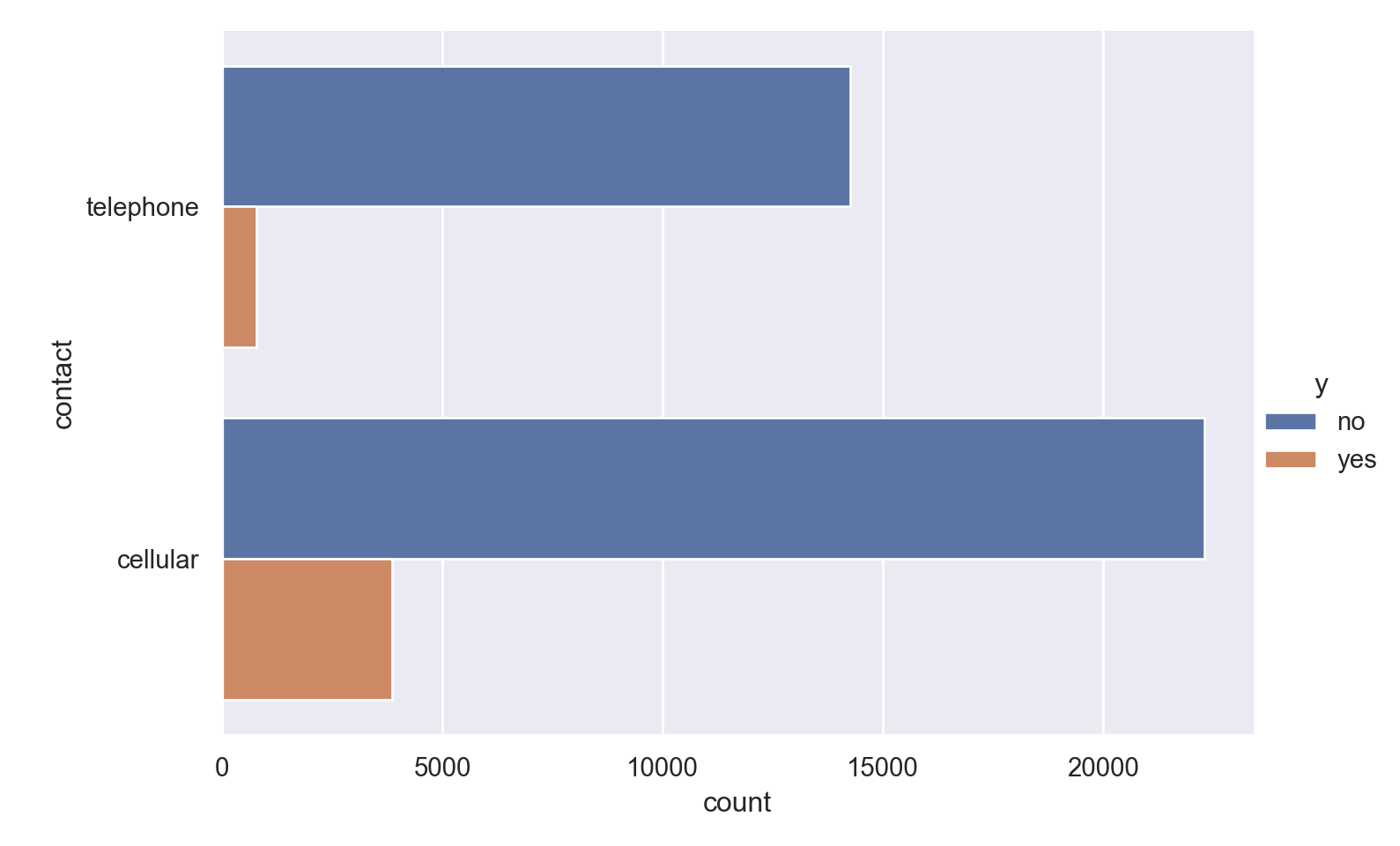

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(contact), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="contact", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

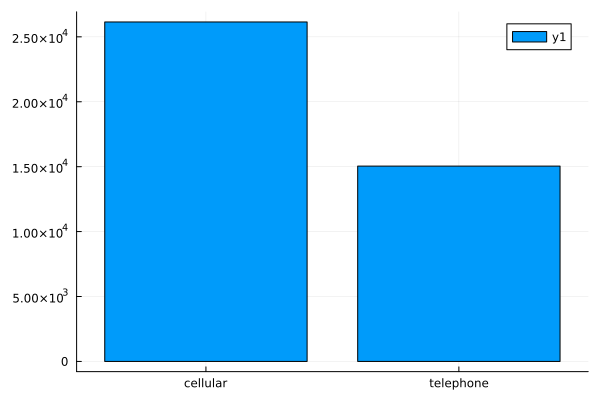

bar(countmap(data.contact))

Observations

- Those contacted on cellular phones have a significantly higher possibility of subscribing to the deposit.

month

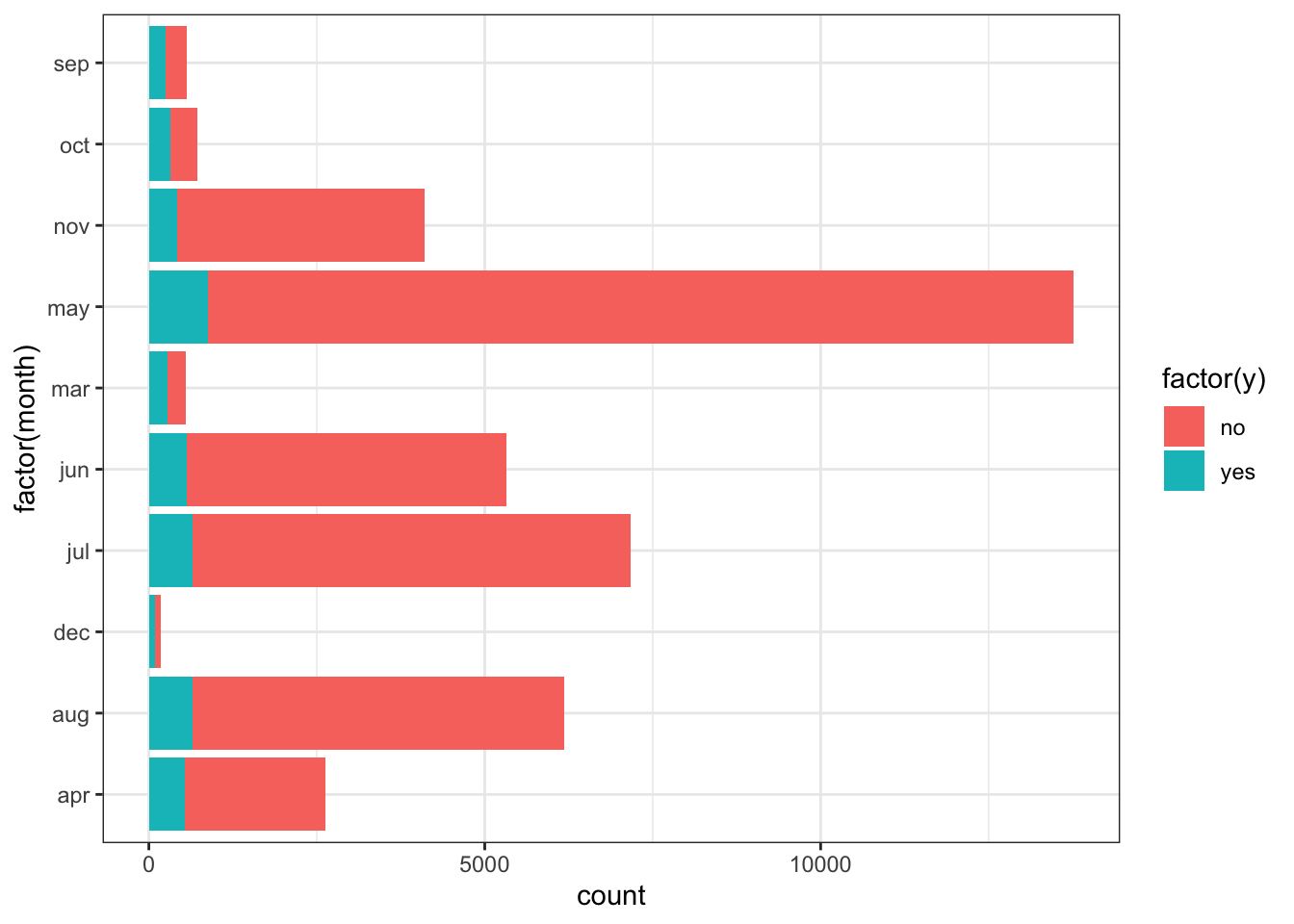

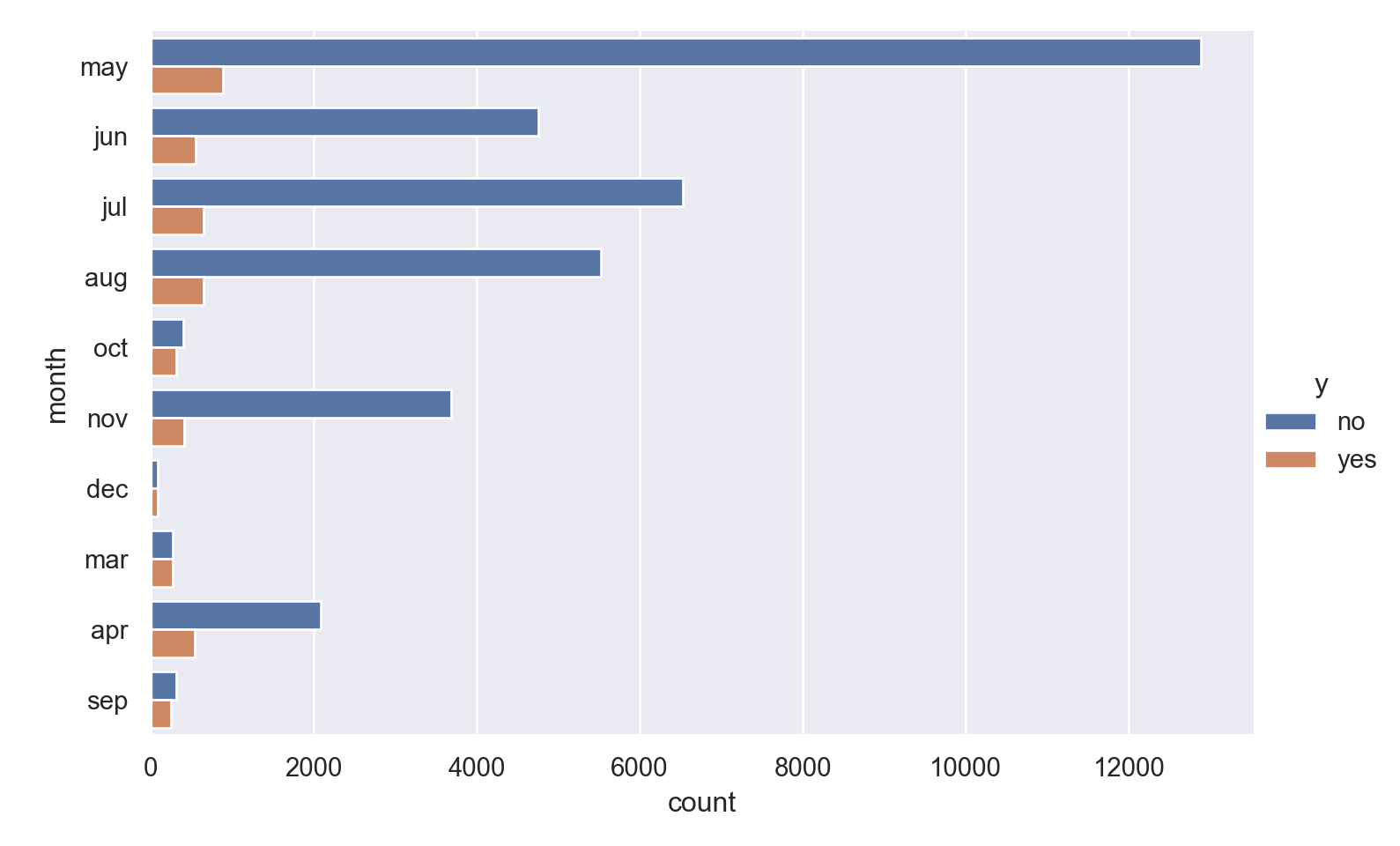

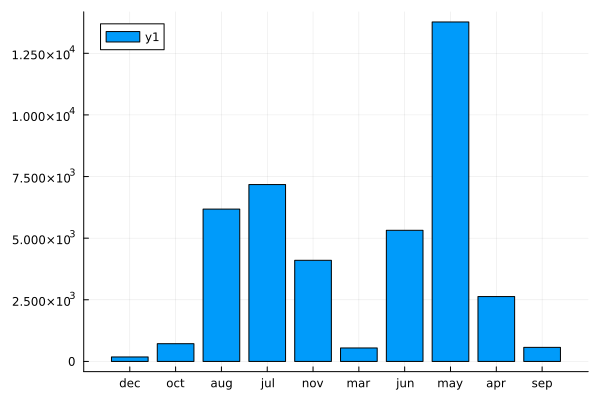

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(month), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="month", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

bar(countmap(data.month))

Observations

Most calls are placed in May.

The months where there were much fewer calls have a much larger chance of subscribing for the loan.

day_of_week

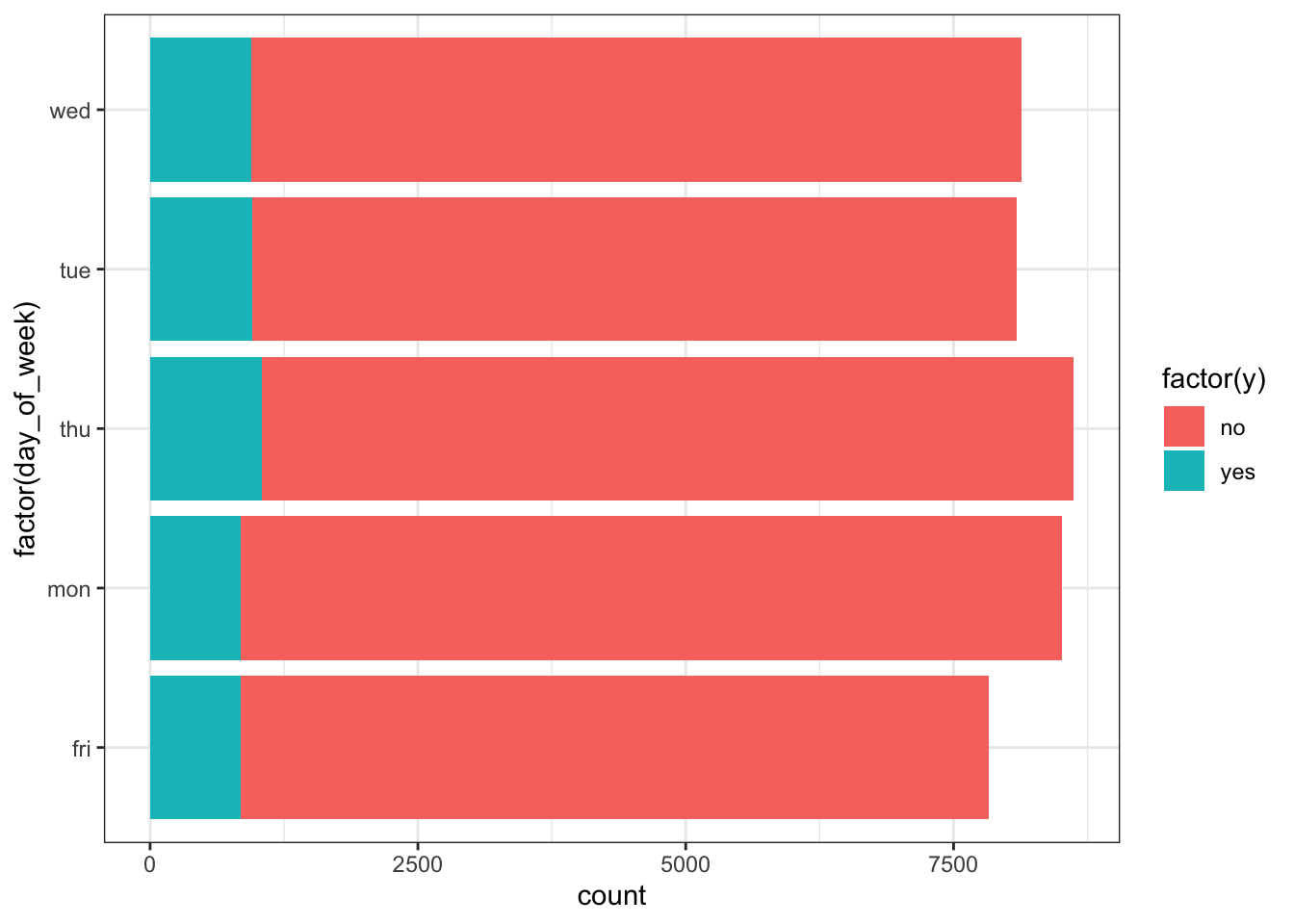

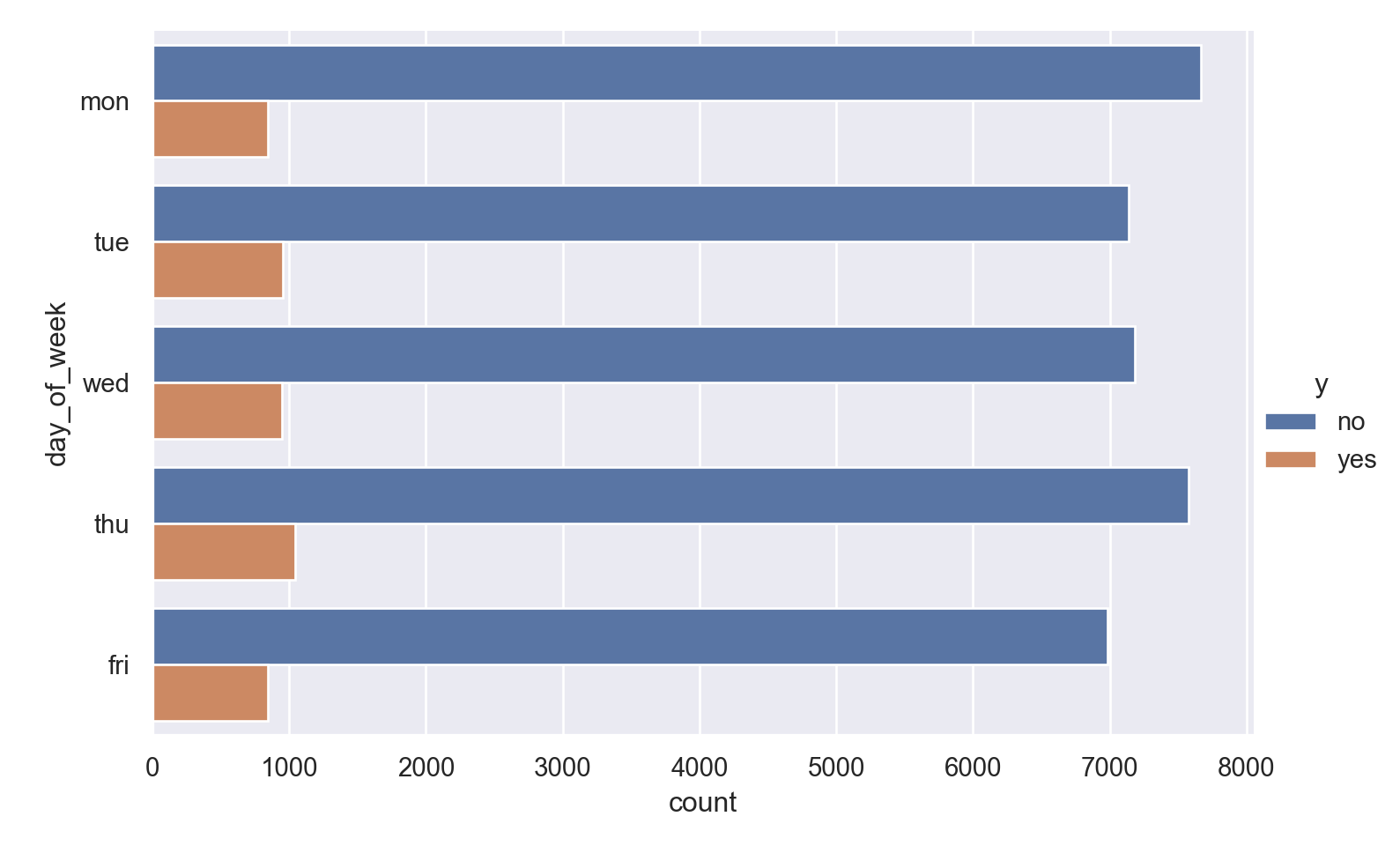

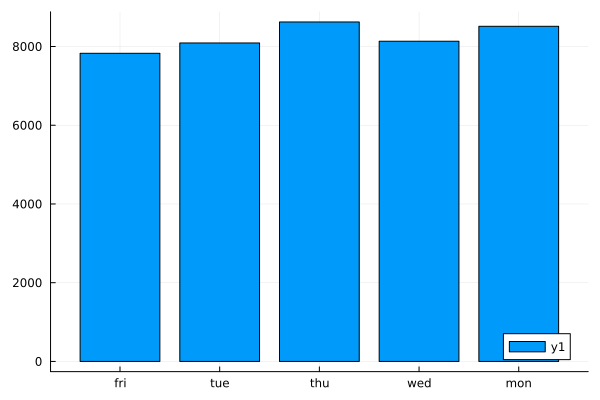

ggplot(data_bank_marketing) + geom_bar(aes(y=factor(day_of_week), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, y="day_of_week", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

bar(countmap(data.day_of_week))

poutcome

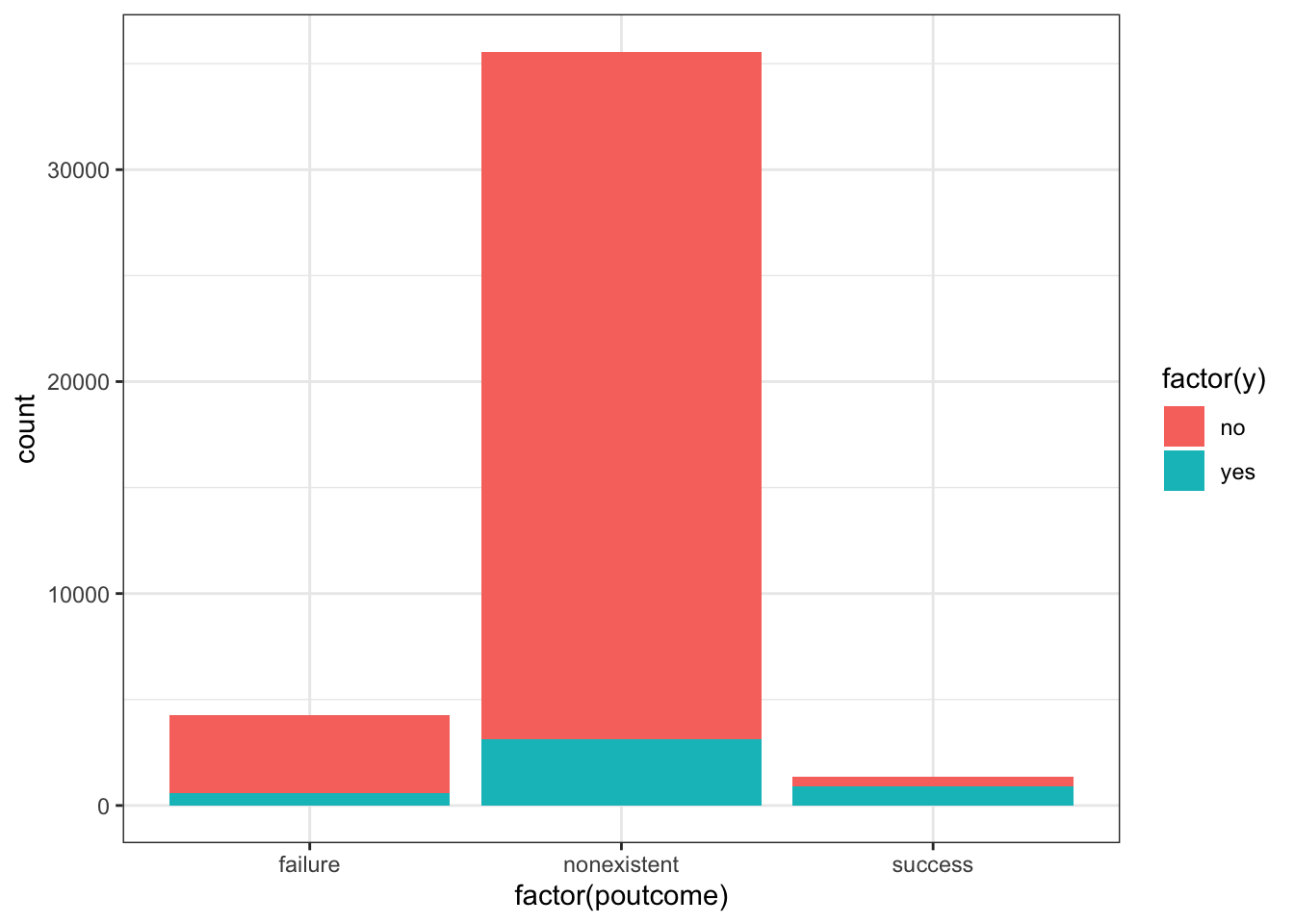

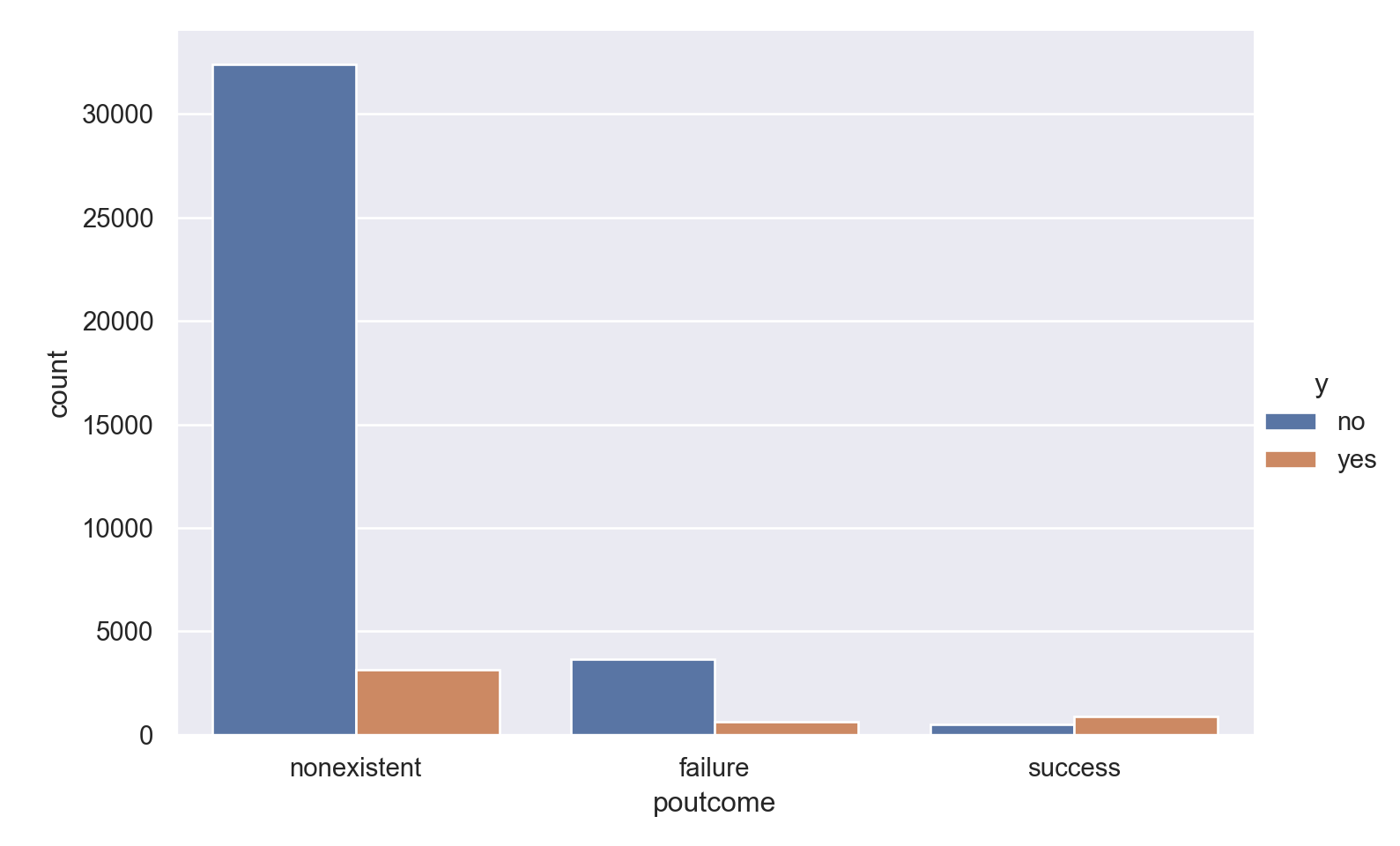

ggplot(data_bank_marketing) + geom_bar(aes(x=factor(poutcome), fill=factor(y)))

p=sns.catplot(data=data_bank_marketing, x="poutcome", hue="y", kind="count", height = 5, aspect = 1.5)

plt.show()

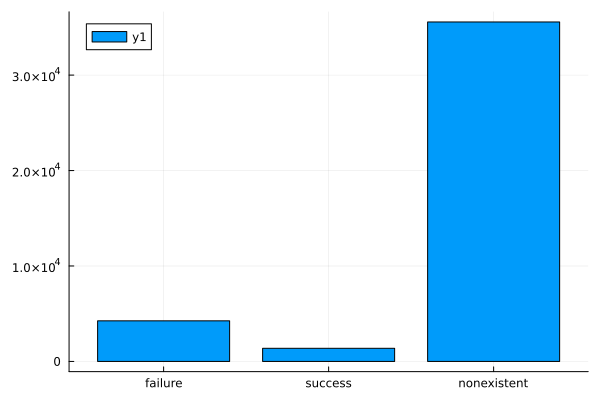

bar(countmap(data.poutcome))

Observations

People with successful outcome in the previous campaign are much more like to have the same outcome in the current campaign.

Most people were not contacted in previous campaigns.

Transformations

- Log and square transforms applied to numeric predictors.

- Dummy transform needed for categorical predictors.

- Interactions defined for age with job and education.

base_rec = recipe(y ~ ., data = data_bank_marketing_train) %>% step_rm(duration) #%>% step_zv(all_numeric_predictors()) %>% step_normalize(all_numeric_predictors()) %>% step_pca(all_numeric_predictors())

trfm_rec = base_rec %>% step_log(c(age, campaign, previous)) %>% step_poly(c(pdays, cons.conf.idx, cons.price.idx, nr.employed, emp.var.rate, euribor3m)) %>% step_dummy(all_nominal_predictors()) %>% step_interact(terms =~ age:starts_with("job") + age:starts_with("education"))

trfm_data = prep(trfm_rec, data_bank_marketing_train) %>% bake(new_data = NULL)

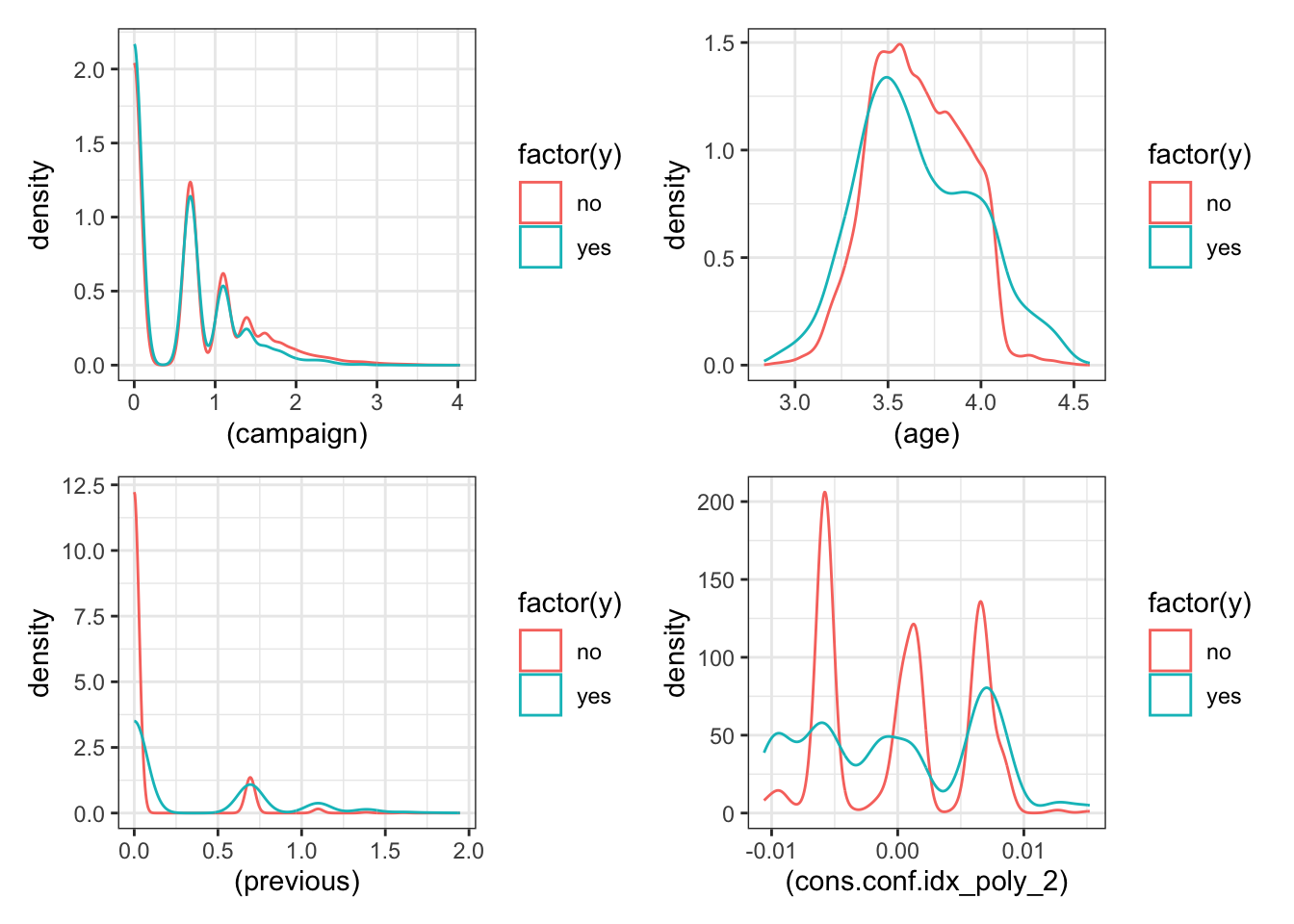

p1 = ggplot(trfm_data) + geom_density(aes(x=(campaign), color=factor(y)))

p2 = ggplot(trfm_data) + geom_density(aes(x=(age), color=factor(y)))

p3 = ggplot(trfm_data) + geom_density(aes(x=(previous), color=factor(y)))

p4 = ggplot(trfm_data) + geom_density(aes(x=(cons.conf.idx_poly_2), color=factor(y)))

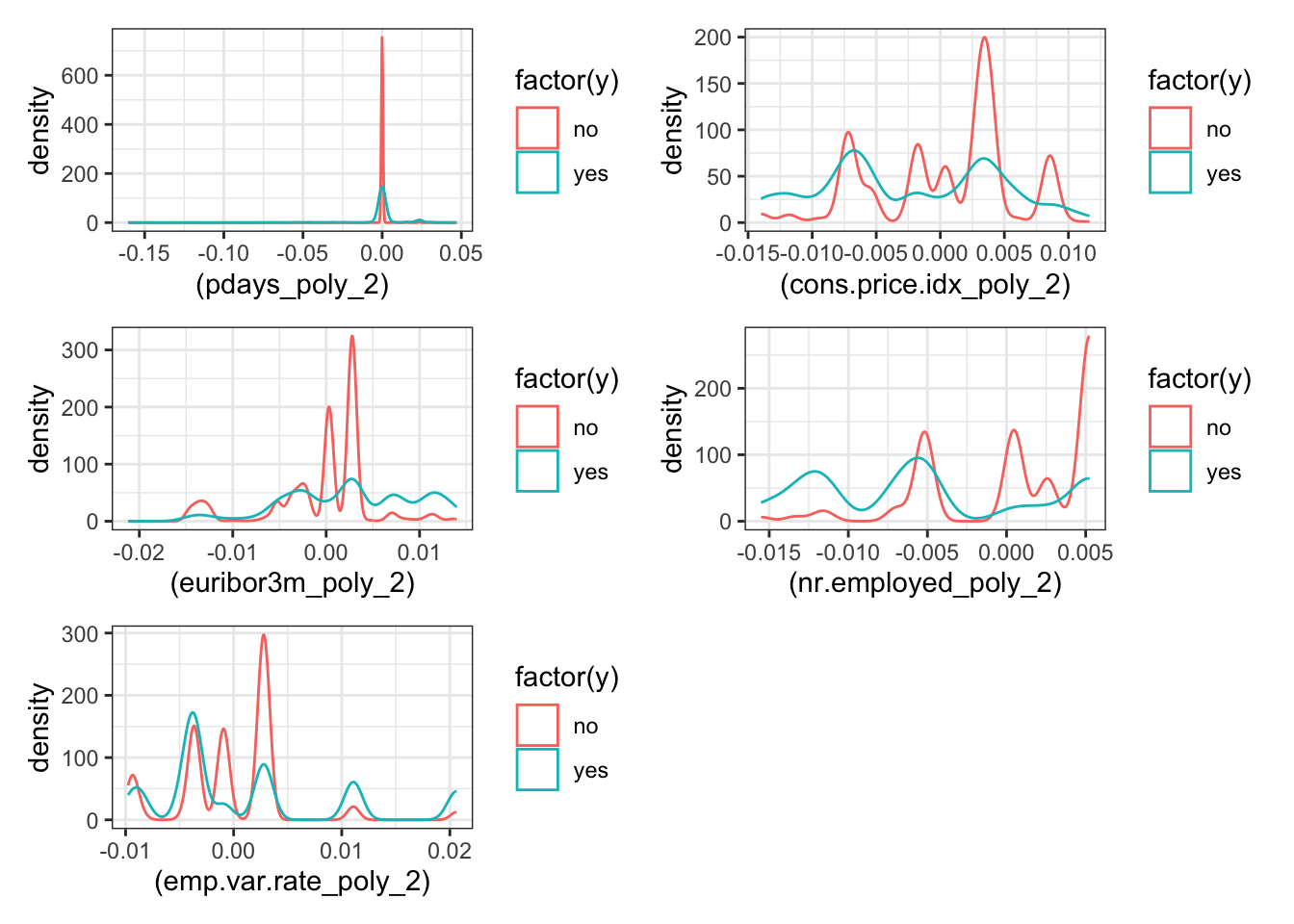

p5 = ggplot(trfm_data) + geom_density(aes(x=(pdays_poly_2), color=factor(y)))

p6 = ggplot(trfm_data) + geom_density(aes(x=(cons.price.idx_poly_2), color=factor(y)))

p7 = ggplot(trfm_data) + geom_density(aes(x=(euribor3m_poly_2), color=factor(y)))

p8 = ggplot(trfm_data) + geom_density(aes(x=(nr.employed_poly_2), color=factor(y)))

p9 = ggplot(trfm_data) + geom_density(aes(x=(emp.var.rate_poly_2), color=factor(y)))

p1+p2+p3+p4 + plot_layout(ncol = 2)

p5+p6+p7+p8+p9 + plot_layout(ncol = 2)

numerical_cols = data_bank_marketing_train.select_dtypes(include=['int64', 'float64']).columns

categorical_cols = data_bank_marketing_train.select_dtypes(include=['object', 'bool']).columns

log_tranform_cols = ['age', 'campaign', 'previous']

cols_index = [data_bank_marketing_train.columns.get_loc(col) for col in log_tranform_cols]

#power_transform_cols = ['cons.conf.idx', 'cons.price.idx', 'nr.employed', 'emp.var.rate', 'euribor3m']

#power_cols_index = [data_bank_marketing_train.columns.get_loc(col) for col in power_transform_cols]

#dummy_cols = ['age', 'duration', 'campaign', 'pdays', 'previous', 'emp.var.rate', 'cons.price.idx', 'cons.conf.idx', 'euribor3m', 'nr.employed']

interact_cols = ['age', 'job']

interact_cols_index = [data_bank_marketing_train.columns.get_loc(col) for col in interact_cols]

# set up the log transformer

log_transform = ColumnTransformer(

transformers=[

('log', FunctionTransformer(np.log1p), cols_index),

],

verbose_feature_names_out=False, # if True, "log_" will be prefixed to the column names that have been transformed

remainder='passthrough' # this allows columns not being transformed to pass through unchanged

)

# this ensures that the transform outputs a DataFrame, so that the column names are available for the next step.

log_transform.set_output(transform='pandas')

# power = ColumnTransformer(

# transformers=[

# ('power', FunctionTransformer(np.square), power_cols_index),

# ],

# verbose_feature_names_out=False,

# remainder='passthrough'

# )

# power.set_output(transform='pandas')ColumnTransformer(remainder='passthrough',

transformers=[('log',

FunctionTransformer(func=<ufunc 'log1p'>),

[0, 10, 12])],

verbose_feature_names_out=False)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

ColumnTransformer(remainder='passthrough',

transformers=[('log',

FunctionTransformer(func=<ufunc 'log1p'>),

[0, 10, 12])],

verbose_feature_names_out=False)[0, 10, 12]

FunctionTransformer(func=<ufunc 'log1p'>)

passthrough

dummy = ColumnTransformer(

transformers=[

('dummy', OneHotEncoder(drop='first', sparse=False), categorical_cols),

],

verbose_feature_names_out=False,

remainder='passthrough'

)

dummy.set_output(transform='pandas')

# interact = ColumnTransformer(

# transformers=[

# ('interact', PolynomialFeatures(interaction_only=True), interact_cols_index),

# ],

# verbose_feature_names_out=False,

# remainder='passthrough'

# )

#

# interact.set_output(transform='pandas')ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first', sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first', sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object')

OneHotEncoder(drop='first', sparse=False)

passthrough

pipe = ContinuousEncoder()ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false)Observations

- Some of the predictors have a reduction in the skew after the transformation.

Logistic regression

glmnet_recipe <-

recipe(formula = y ~ ., data = data_bank_marketing_train) %>%

step_rm(duration) %>%

step_log(c(age, campaign, previous)) %>%

#step_poly(c(pdays, cons.conf.idx, cons.price.idx, nr.employed, emp.var.rate, euribor3m)) %>%

## For modeling, it is preferred to encode qualitative data as factors

## (instead of character).

step_string2factor(one_of("job", "marital", "education", "default", "housing",

"loan", "contact", "month", "day_of_week", "poutcome", "y")) %>%

step_novel(all_nominal_predictors()) %>%

## This model requires the predictors to be numeric. The most common

## method to convert qualitative predictors to numeric is to create

## binary indicator variables (aka dummy variables) from these

## predictors.

step_dummy(all_nominal_predictors()) %>%

## Regularization methods sum up functions of the model slope

## coefficients. Because of this, the predictor variables should be on

## the same scale. Before centering and scaling the numeric predictors,

## any predictors with a single unique value are filtered out.

step_zv(all_predictors()) %>%

step_normalize(all_numeric_predictors())

glmnet_spec <-

multinom_reg(penalty = tune(), mixture = tune()) %>%

set_mode("classification") %>%

set_engine("glmnet")

glmnet_workflow <-

workflow() %>%

add_recipe(glmnet_recipe) %>%

add_model(glmnet_spec)

glmnet_grid <- tidyr::crossing(penalty = 10^seq(-6, -1, length.out = 20), mixture = c(0.05,

0.2, 0.4, 0.6, 0.8, 1))

# glmnet_tune <-

# tune_grid(glmnet_workflow, resamples = data_folds, grid = glmnet_grid, control = control_grid(save_pred = TRUE), metrics = metric_set(roc_auc))

final_params <-

tibble(

penalty = 0.0000695,

mixture = 1

)

final_glmnet_wflow = glmnet_workflow %>% finalize_workflow(final_params)

final_glmnet_wflow══ Workflow ════════════════════════════════════════════════════════════════════

Preprocessor: Recipe

Model: multinom_reg()

── Preprocessor ────────────────────────────────────────────────────────────────

7 Recipe Steps

• step_rm()

• step_log()

• step_string2factor()

• step_novel()

• step_dummy()

• step_zv()

• step_normalize()

── Model ───────────────────────────────────────────────────────────────────────

Multinomial Regression Model Specification (classification)

Main Arguments:

penalty = 6.95e-05

mixture = 1

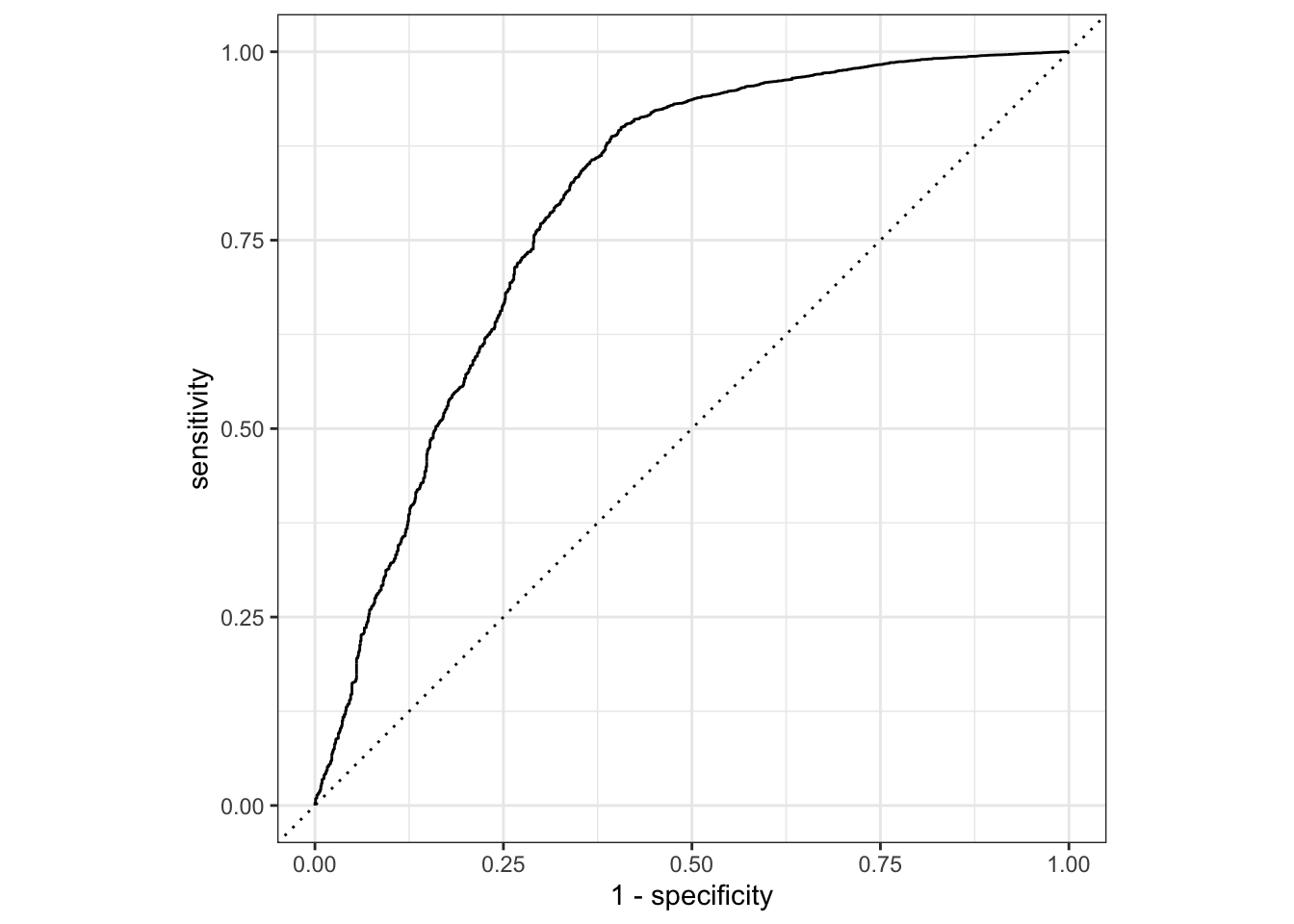

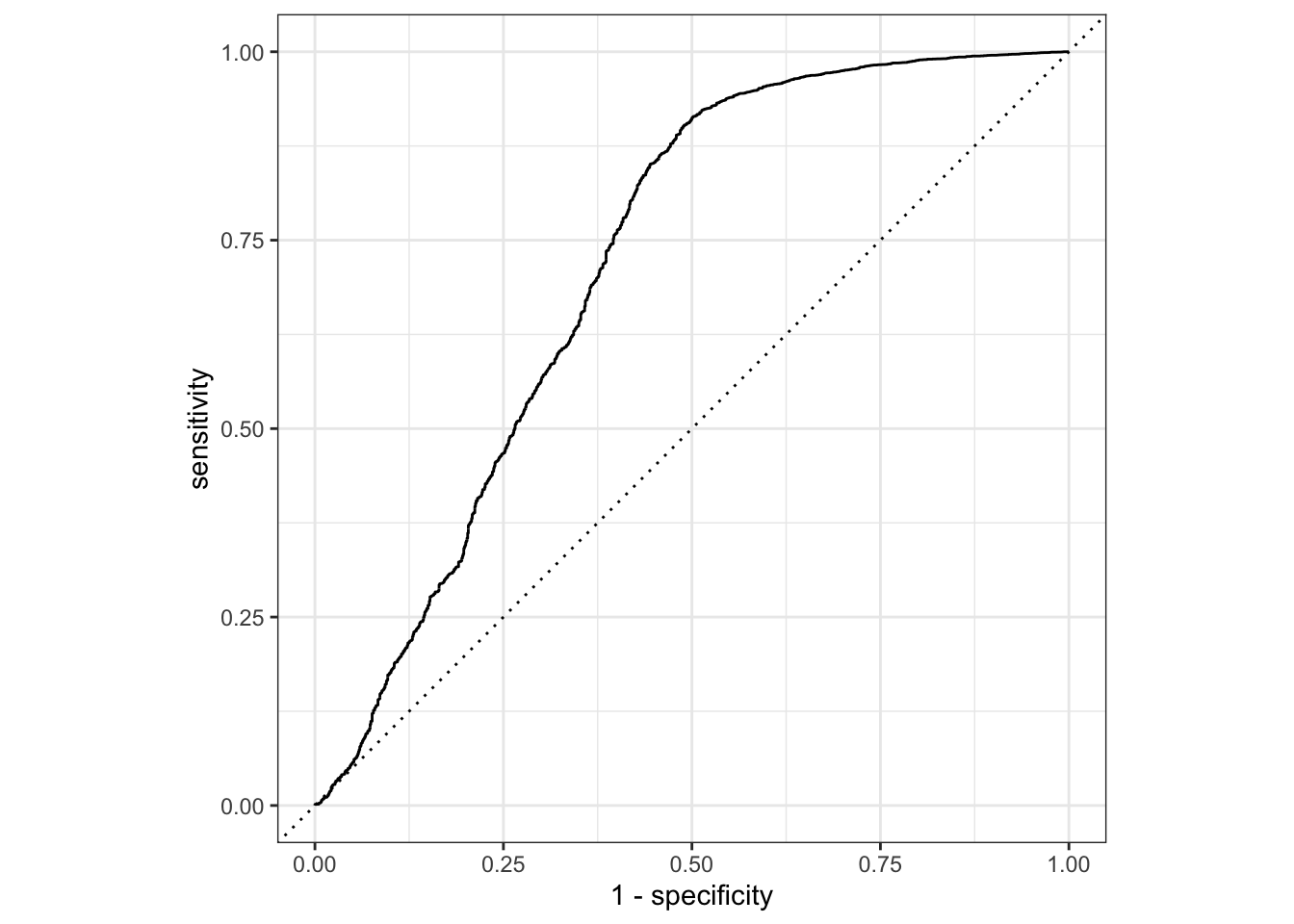

Computational engine: glmnet final_glmnet_fit = final_glmnet_wflow %>% last_fit(data_bank_marketing_split)

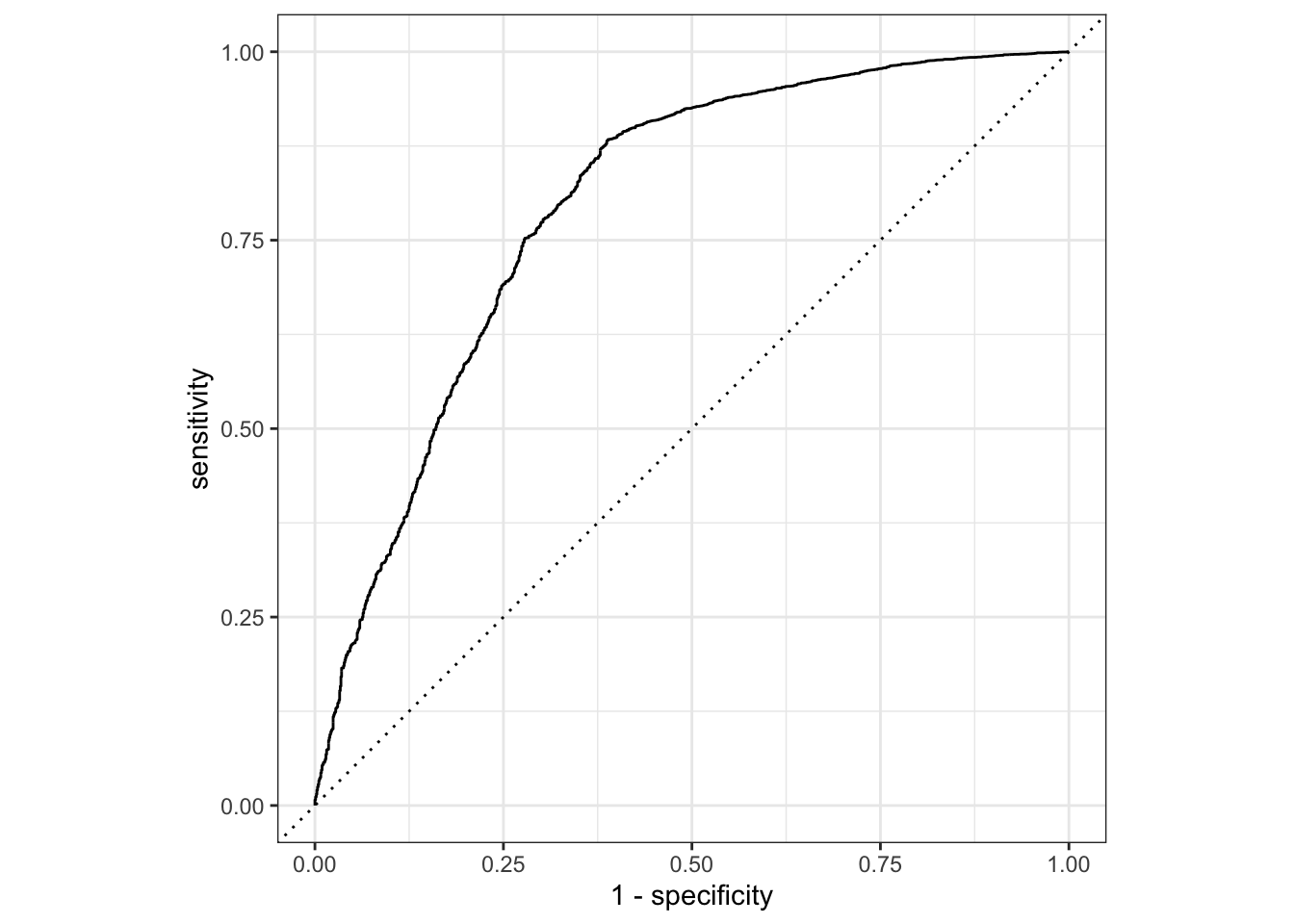

final_glmnet_fit %>% collect_metrics()# A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 accuracy binary 0.901 Preprocessor1_Model1

2 roc_auc binary 0.793 Preprocessor1_Model1final_glmnet_fit %>% collect_predictions()# A tibble: 10,297 × 7

id .pred_no .pred_yes .row .pred_class y .config

<chr> <dbl> <dbl> <int> <fct> <fct> <chr>

1 train/test split 0.970 0.0299 7 no no Preprocessor1_Mo…

2 train/test split 0.977 0.0225 18 no no Preprocessor1_Mo…

3 train/test split 0.968 0.0321 21 no no Preprocessor1_Mo…

4 train/test split 0.980 0.0201 22 no no Preprocessor1_Mo…

5 train/test split 0.970 0.0296 24 no no Preprocessor1_Mo…

6 train/test split 0.985 0.0155 30 no no Preprocessor1_Mo…

7 train/test split 0.977 0.0230 34 no no Preprocessor1_Mo…

8 train/test split 0.975 0.0255 35 no no Preprocessor1_Mo…

9 train/test split 0.969 0.0313 43 no no Preprocessor1_Mo…

10 train/test split 0.973 0.0265 52 no no Preprocessor1_Mo…

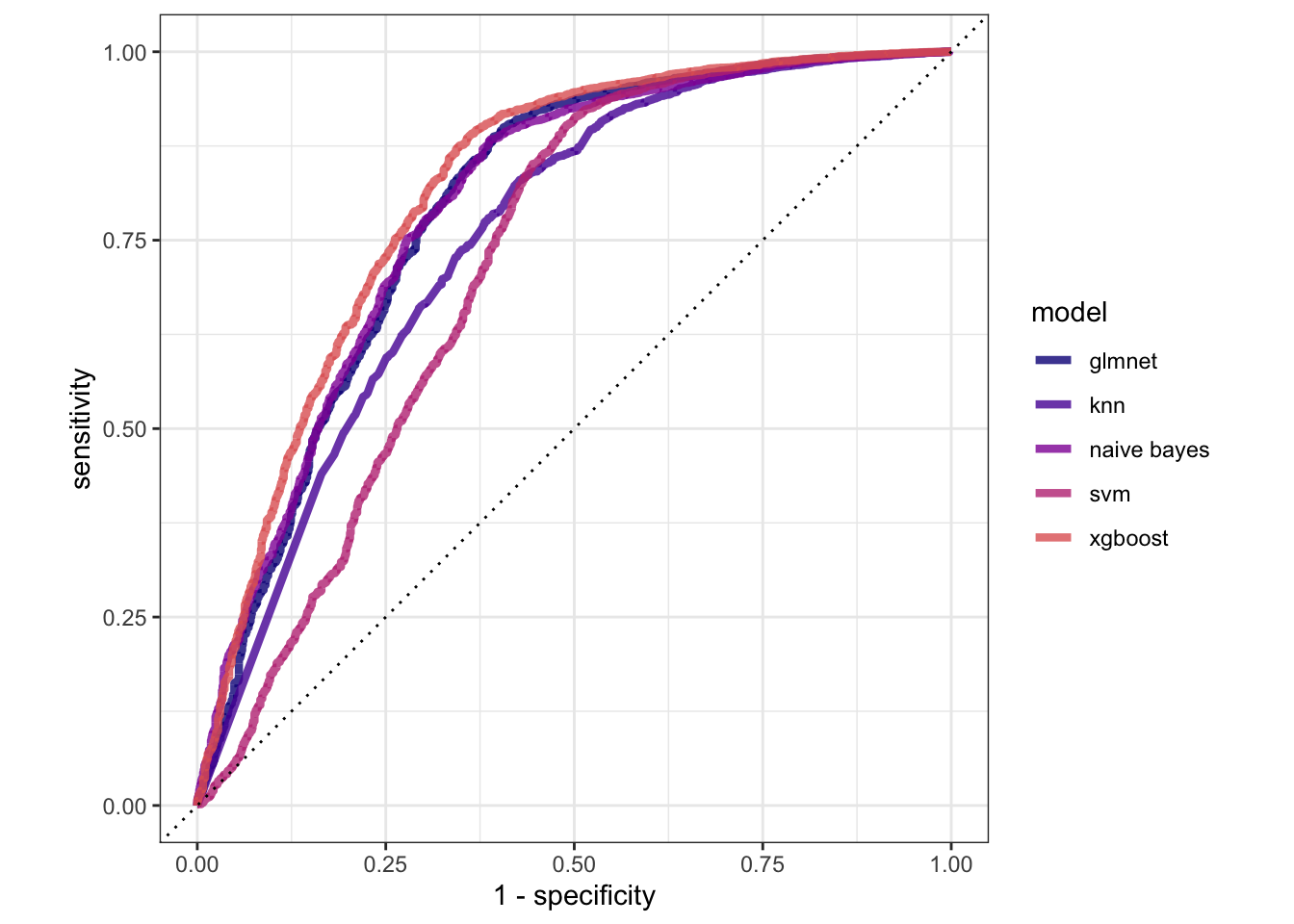

# … with 10,287 more rowsfinal_glmnet_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% autoplot()

glmnet_auc = final_glmnet_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% mutate(model = "glmnet")

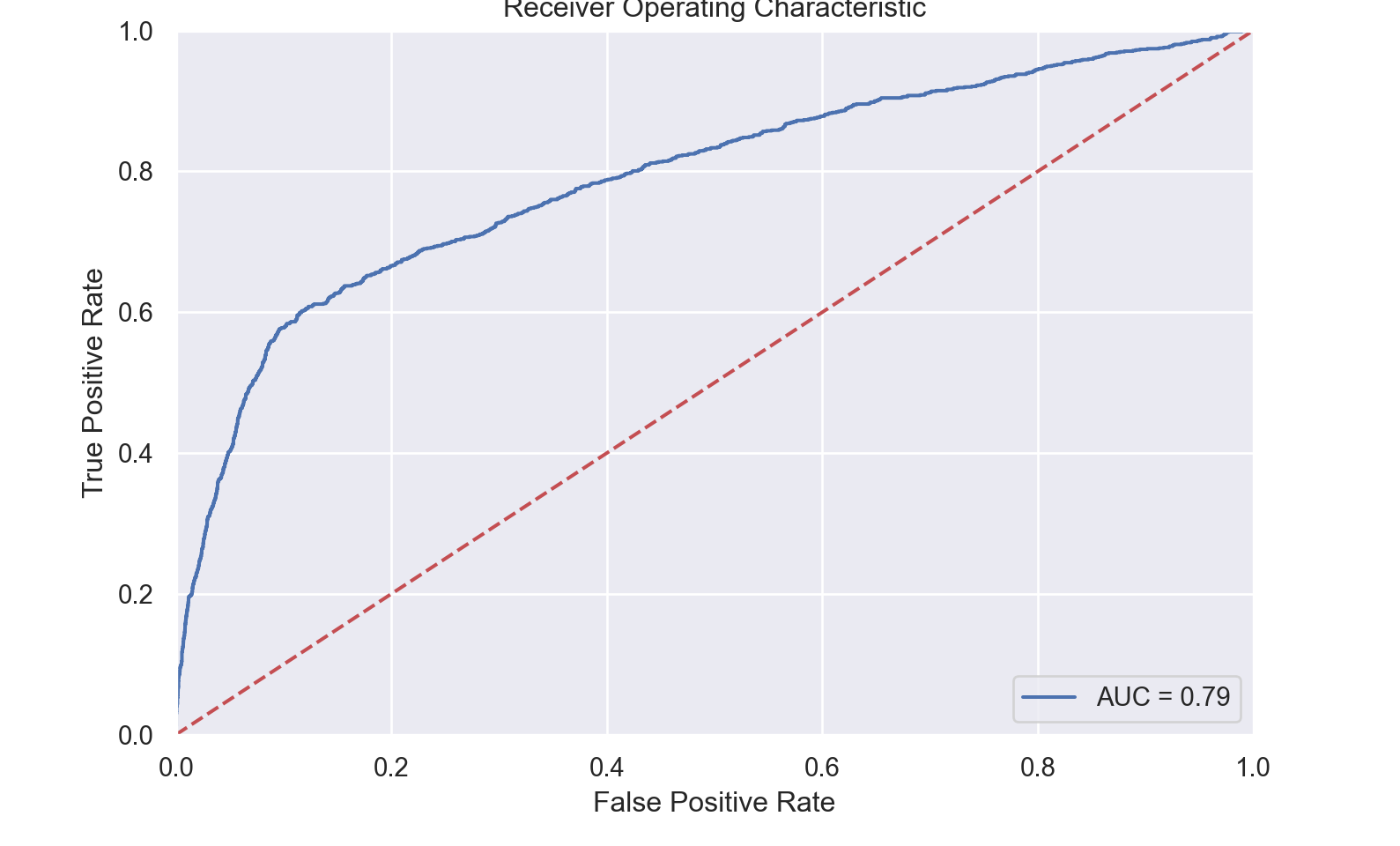

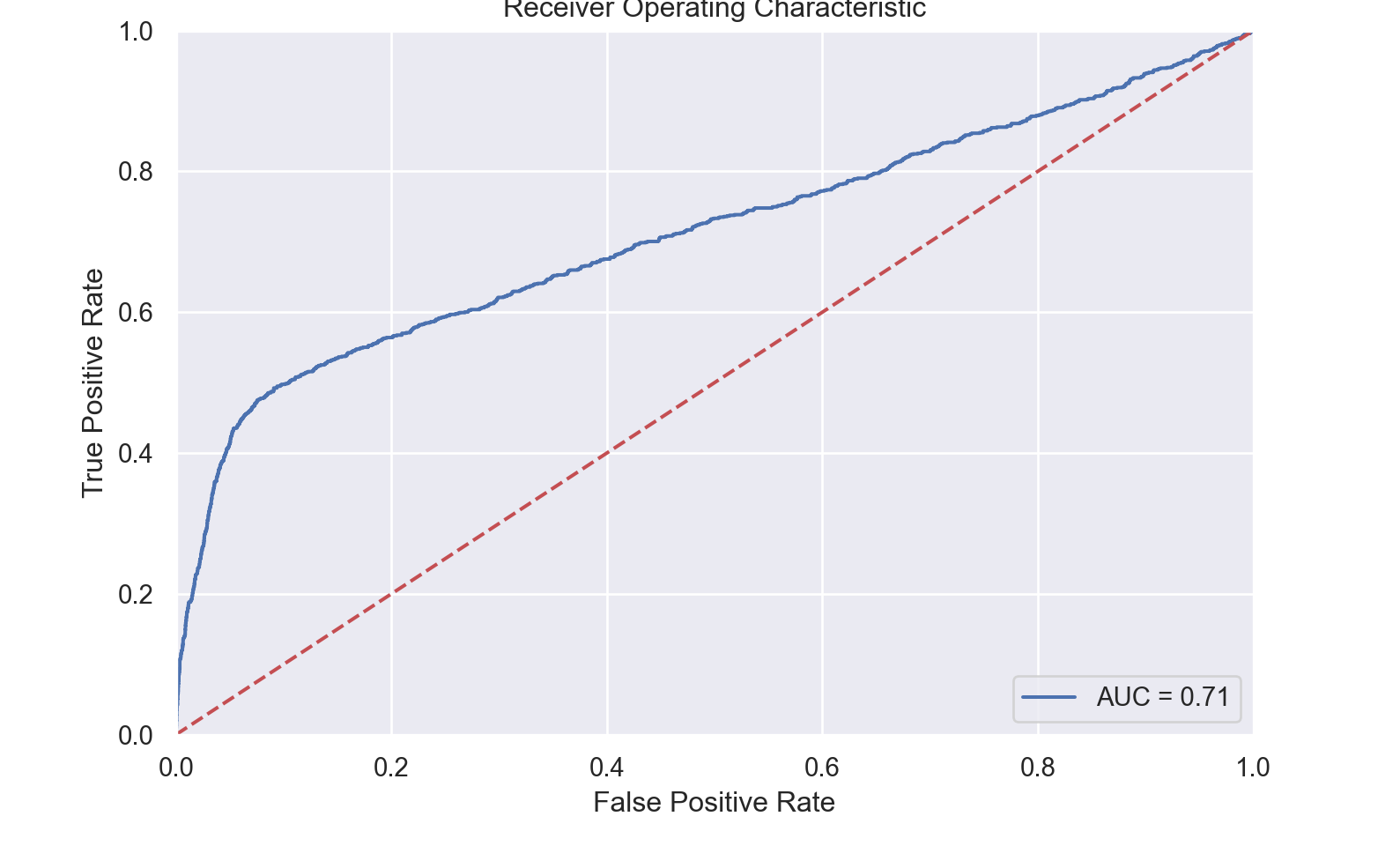

def roc_plot(X_test,Y_test, fitted_model, pos_label='yes'):

# calculate the fpr and tpr for all thresholds of the classification

probs = fitted_model.predict_proba(X_test)

probs_no = probs[:,1]

fpr, tpr, threshold = metrics.roc_curve(Y_test, probs_no, pos_label = pos_label)

roc_auc = metrics.auc(fpr, tpr)

plt.clf()

plt.title('Receiver Operating Characteristic')

plt.plot(fpr, tpr, 'b', label = 'AUC = %0.2f' % roc_auc)

plt.legend(loc = 'lower right')

plt.plot([0, 1], [0, 1],'r--')

plt.xlim([0, 1])

plt.ylim([0, 1])

plt.ylabel('True Positive Rate')

plt.xlabel('False Positive Rate')

plt.show()

return roc_auc

def grid_search_fit(pipe, param_grid, X_train, Y_train, X_test, Y_test, cv=10, scoring='roc_auc', plot=True, report=False):

grid = GridSearchCV(pipe, param_grid, cv=10, scoring=scoring)

grid.fit(X_train, Y_train)

fitted_model=grid.best_estimator_

score=grid.score(X_test, Y_test)

yhat=grid.predict(X_test)

if report:

print(metrics.classification_report(Y_test, yhat))

if plot:

roc_plot(X_test, Y_test, fitted_model, 'yes')

return (fitted_model, score, yhat)

model = LogisticRegression(penalty='elasticnet', solver='saga', max_iter=1000)

#model = SGDClassifier(max_iter=1000, penalty='elasticnet')

steps.append(("model", model))

param_grid = {'model__l1_ratio':np.arange(0,1,0.1)}

# param_grid = [

# {'penalty' : ['l1', 'l2', 'elasticnet', 'none'],

# 'C' : np.logspace(-4, 4, 20),

# 'solver' : ['lbfgs','newton-cg','liblinear','sag','saga'],

# 'max_iter' : [100, 1000,2500, 5000]

# }

# ]

pipe = Pipeline(steps)

grid = GridSearchCV(pipe, param_grid, cv=10, scoring='roc_auc')

grid.fit(data_bank_marketing_train, y_train)GridSearchCV(cv=10,

estimator=Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()),

('zv', VarianceThreshold()),

('model',

LogisticRegression(max_iter=1000,

penalty='elasticnet',

solver='saga'))]),

param_grid={'model__l1_ratio': array([0. , 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9])},

scoring='roc_auc')In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

GridSearchCV(cv=10,

estimator=Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()),

('zv', VarianceThreshold()),

('model',

LogisticRegression(max_iter=1000,

penalty='elasticnet',

solver='saga'))]),

param_grid={'model__l1_ratio': array([0. , 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9])},

scoring='roc_auc')Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()), ('zv', VarianceThreshold()),

('model',

LogisticRegression(max_iter=1000, penalty='elasticnet',

solver='saga'))])ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first', sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object')

OneHotEncoder(drop='first', sparse=False)

['age', 'campaign', 'pdays', 'previous', 'emp.var.rate', 'cons.price.idx', 'cons.conf.idx', 'euribor3m', 'nr.employed']

passthrough

MinMaxScaler()

VarianceThreshold()

LogisticRegression(max_iter=1000, penalty='elasticnet', solver='saga')

grid.best_params_{'model__l1_ratio': 0.6000000000000001}fitted_model=grid.best_estimator_

score=grid.score(data_bank_marketing_test, y_test)

#score

yhat=grid.predict_proba(data_bank_marketing_test)

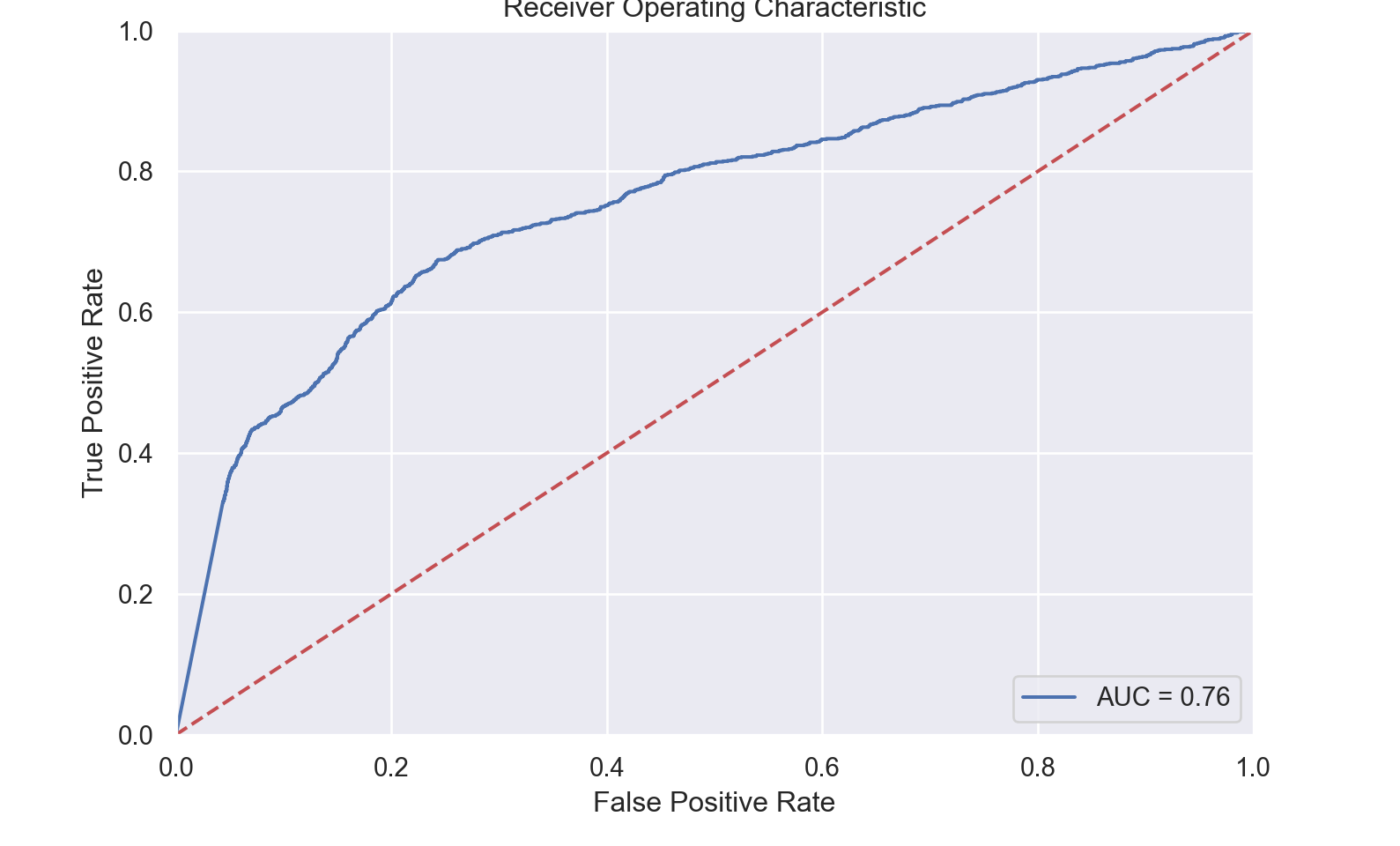

roc_plot(data_bank_marketing_test, y_test, fitted_model, 'yes')

#sgdclass_param_grid = {'model__alpha': [0.0001, 0.001, 0.01, 0.1, 1, 10, 100],

# "model__l1_ratio": np.arange(0.0, 1.0, 0.1)}0.7904608842023623

import MLJLinearModels.LogisticClassifier

LinearBinaryClassifier = MLJLinearModels.LogisticClassifierLogisticClassifiermodel = Standardizer |> ContinuousEncoder |> LogisticClassifierProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

logistic_classifier = LogisticClassifier(

lambda = 2.220446049250313e-16,

gamma = 0.0,

penalty = :l2,

fit_intercept = true,

penalize_intercept = false,

scale_penalty_with_samples = true,

solver = nothing),

cache = true)

#tuning = RandomSearch(rng=123);

tuning = Grid(rng=123);

# tuning=LatinHypercube(gens = 1,

# popsize = 100,

# ntour = 2,

# ptour = 0.8,

# interSampleWeight = 1.0,

# ae_power = 2,

# periodic_ae = false,

# rng=123)

r = range(model,

:(logistic_classifier.lambda),

lower=0,

upper=1,

unit=0.01)NumericRange(0 ≤ logistic_classifier.lambda ≤ 1; origin=0.5, unit=0.01)

s = range(model,

:(logistic_classifier.gamma),

lower=0,

upper=1,

unit=0.01)NumericRange(0 ≤ logistic_classifier.gamma ≤ 1; origin=0.5, unit=0.01)

tuned_model = TunedModel(model=model,

ranges=[r, s],

resampling=CV(nfolds=10),

measures=auc,

tuning=tuning,

n=200);

tuned_mach = machine(tuned_model, X_train, y_train);

fit!(tuned_mach);

yhat=MLJ.predict(tuned_mach, X_test);

rep = report(tuned_mach);

print(

"Measurements:\n",

" brier loss: ", brier_loss(yhat,y_test) |> mean, "\n",

" auc: ", auc(yhat,y_test), "\n",

" accuracy: ", accuracy(mode.(yhat), y_test)

)Measurements:

brier loss: 0.16162546559785088

auc: 0.769700437197346

accuracy: 0.9018290708967304

# LogisticModel = machine(LinearBinaryClassifierPipe, X_train, y_train);

# fit!(LogisticModel);

# fp = fitted_params(LogisticModel);

# fp.logistic_classifier

#keys(fp)

#rpt = report(LogisticModel)

#keys(rpt)

# fi = rpt.linear_binary_classifier.coef_table |> DataFrames.DataFrame

#ŷ = MLJ.predict(LogisticModel, X_test);

#

# print(

# "Measurements:\n",

# " brier loss: ", brier_loss(ŷ,y_test) |> mean, "\n",

# " auc: ", auc(ŷ,y_test), "\n",

# " accuracy: ", accuracy(mode.(ŷ), y_test)

# )

#

# #confmat(mode.(ŷ),y_test)

#

# e_pipe = evaluate(LinearBinaryClassifierPipe, X_train, y_train,

# resampling=StratifiedCV(nfolds=6, rng=42),

# measures=[brier_loss, auc, accuracy],

# repeats=1,

# acceleration=CPUThreads())

#show(iterated_pipe, 2)

# iterated_pipe = IteratedModel(model=LinearBinaryClassifierPipe,

# controls=controls,

# measure=auc,

# resampling=StratifiedCV(nfolds=6, rng=42))

#mach_iterated_pipe = machine(LinearBinaryClassifierPipe, X_train, y_train);

#fit!(mach_iterated_pipe);

#residuals = [1 - pdf(ŷ[i], y_test[i,1]) for i in 1:nrow(y_test)]

# r = report(LogisticModel)

#

# k = collect(keys(fp.fitted_params_given_machine))[3]

# println("\n Coefficients: ", fp.fitted_params_given_machine[k].coef)

# println("\n y \n ", y_test[1:5,1])

# println("\n ŷ \n ", ŷ[1:5])

# println("\n residuals \n ", residuals[1:5])

# println("\n Standard Error per Coefficient \n", r.linear_binary_classifier.stderror[2:end])

#confusion_matrix(yMode, y_test)

Naive Bayes

nb_recipe <-

recipe(formula = y ~ ., data = data_bank_marketing_train) %>%

step_rm(duration) %>%

step_dummy()

nb_spec <-

naive_Bayes(smoothness = tune(), Laplace = tune()) %>%

set_engine("naivebayes")

nb_workflow <-

workflow() %>%

add_recipe(nb_recipe) %>%

add_model(nb_spec)

#nb_params = extract_parameter_set_dials(nb_spec)

# nb_grid = nb_params %>% grid_latin_hypercube(size = 20, original = FALSE)

#

# nb_tune <-

# nb_workflow %>%

# tune_grid(

# data_folds,

# grid = nb_grid

# )

# nb_tune

# select_best(nb_tune, metric = "roc_auc")

final_params = tibble(

smoothness = 0.5923033,

Laplace = 0.4830422

)

final_nb_wflow <-

nb_workflow %>%

finalize_workflow(final_params)

final_nb_fit <-

final_nb_wflow %>%

last_fit(data_bank_marketing_split)

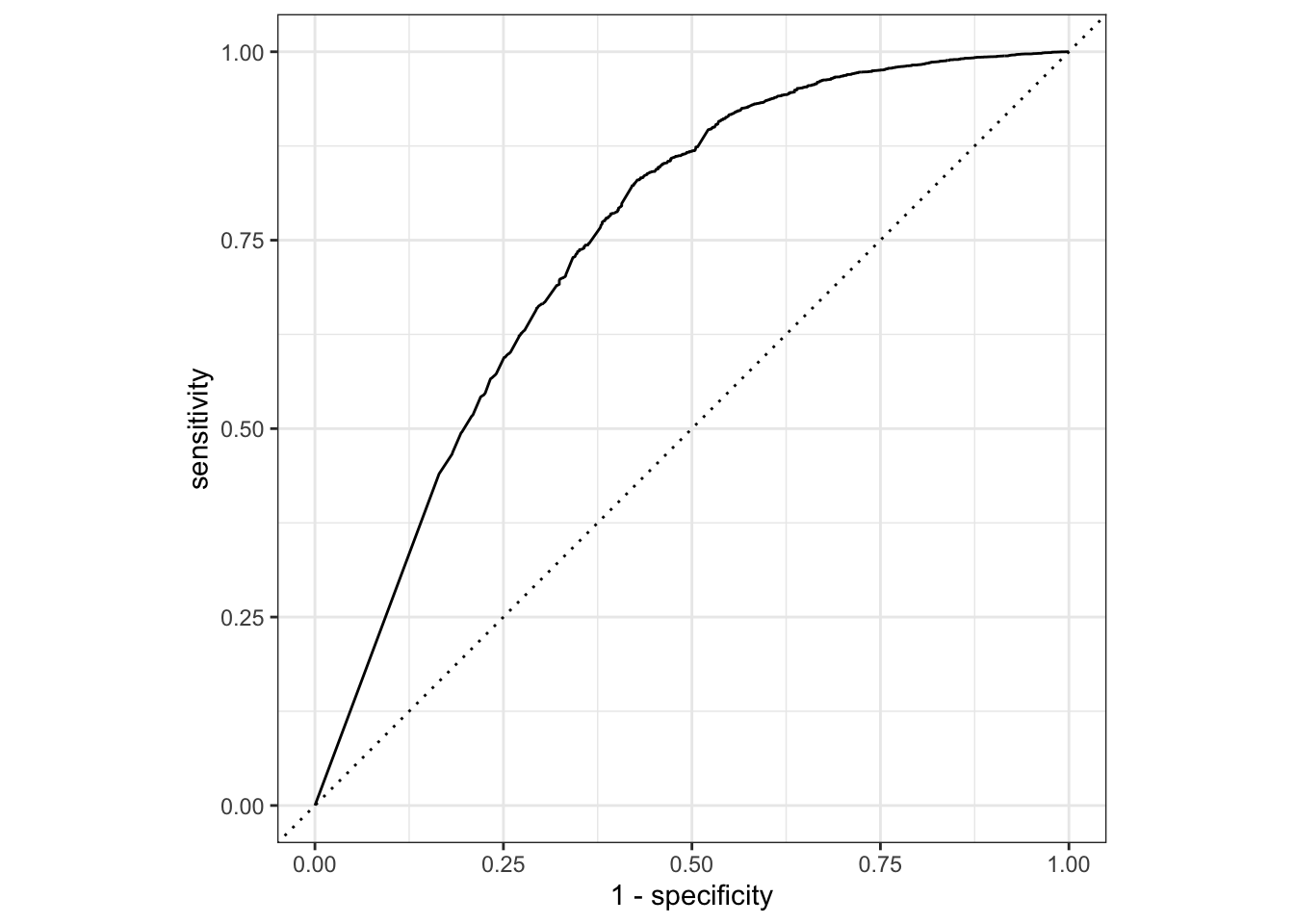

final_nb_fit %>% collect_metrics()# A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 accuracy binary 0.880 Preprocessor1_Model1

2 roc_auc binary 0.795 Preprocessor1_Model1final_nb_fit %>% collect_predictions()# A tibble: 10,297 × 7

id .pred_no .pred_yes .row .pred_class y .config

<chr> <dbl> <dbl> <int> <fct> <fct> <chr>

1 train/test split 1.00 0.00000488 7 no no Preprocessor1_…

2 train/test split 1.00 0.000000414 18 no no Preprocessor1_…

3 train/test split 1.00 0.00000451 21 no no Preprocessor1_…

4 train/test split 1.00 0.000000644 22 no no Preprocessor1_…

5 train/test split 1.00 0.00000345 24 no no Preprocessor1_…

6 train/test split 1.00 0.000000957 30 no no Preprocessor1_…

7 train/test split 1.00 0.00000110 34 no no Preprocessor1_…

8 train/test split 1.00 0.00000159 35 no no Preprocessor1_…

9 train/test split 1.00 0.00000488 43 no no Preprocessor1_…

10 train/test split 1.00 0.00000200 52 no no Preprocessor1_…

# … with 10,287 more rowsfinal_nb_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% autoplot()

nb_auc = final_nb_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% mutate(model = "naive bayes")model = GaussianNB()

model.fit(X_trans_train, y_trans_train)GaussianNB()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

GaussianNB()

model.predict_proba(X_trans_test)array([[9.99990953e-01, 9.04749432e-06],

[8.12354222e-01, 1.87645778e-01],

[9.99999789e-01, 2.10792883e-07],

...,

[9.99294556e-01, 7.05443805e-04],

[9.99995515e-01, 4.48497521e-06],

[7.16817215e-01, 2.83182785e-01]])roc_plot(X_trans_test, y_trans_test, model, 1)0.7567412601500412

import NaiveBayes

GaussianNBClassifier = @load GaussianNBClassifier pkg=NaiveBayes;

model = Standardizer |> ContinuousEncoder |> GaussianNBClassifier()ProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

gaussian_nb_classifier = GaussianNBClassifier(),

cache = true)

# Model training fails with error: nested task error: PosDefException: matrix is not positive definite; Cholesky factorization failed.

# Pre-processing to eliminate collinearity may be needed

# mach = machine(model, X_train, y_train);

#

# fit!(mach);

# yhat=MLJ.predict(mach, X_test);

# rep = report(mach);

# print(

# "Measurements:\n",

# " brier loss: ", brier_loss(yhat,y_test) |> mean, "\n",

# " auc: ", auc(yhat,y_test), "\n",

# " accuracy: ", accuracy(mode.(yhat), y_test)

# )

KNN

#use_kknn(y ~ ., data = data_bank_marketing_train)

kknn_recipe <-

recipe(formula = y ~ ., data = data_bank_marketing_train) %>%

step_rm(duration) %>%

step_string2factor(one_of("job", "marital", "education", "default", "housing",

"loan", "contact", "month", "day_of_week", "poutcome", "y")) %>%

step_novel(all_nominal_predictors()) %>%

step_dummy(all_nominal_predictors()) %>%

step_zv(all_predictors()) %>%

step_normalize(all_numeric_predictors())

kknn_spec <-

nearest_neighbor(neighbors = tune()) %>%

set_mode("classification") %>%

set_engine("kknn")

kknn_param = extract_parameter_set_dials(kknn_spec)

kknn_workflow <-

workflow() %>%

add_recipe(kknn_recipe) %>%

add_model(kknn_spec)

set.seed(66214)

# kknn_tune <-

# tune_grid(kknn_workflow, resamples = data_folds, size =10)

final_params <-

tibble(

neighbors = 14

)

final_kknn_wflow = kknn_workflow %>% finalize_workflow(final_params)

final_kknn_wflow══ Workflow ════════════════════════════════════════════════════════════════════

Preprocessor: Recipe

Model: nearest_neighbor()

── Preprocessor ────────────────────────────────────────────────────────────────

6 Recipe Steps

• step_rm()

• step_string2factor()

• step_novel()

• step_dummy()

• step_zv()

• step_normalize()

── Model ───────────────────────────────────────────────────────────────────────

K-Nearest Neighbor Model Specification (classification)

Main Arguments:

neighbors = 14

Computational engine: kknn final_kknn_fit = final_kknn_wflow %>% last_fit(data_bank_marketing_split)

final_kknn_fit %>% collect_metrics()# A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 accuracy binary 0.894 Preprocessor1_Model1

2 roc_auc binary 0.751 Preprocessor1_Model1final_kknn_fit %>% collect_predictions()# A tibble: 10,297 × 7

id .pred_no .pred_yes .row .pred_class y .config

<chr> <dbl> <dbl> <int> <fct> <fct> <chr>

1 train/test split 1 0 7 no no Preprocessor1_Mo…

2 train/test split 0.932 0.0682 18 no no Preprocessor1_Mo…

3 train/test split 1 0 21 no no Preprocessor1_Mo…

4 train/test split 0.932 0.0682 22 no no Preprocessor1_Mo…

5 train/test split 1 0 24 no no Preprocessor1_Mo…

6 train/test split 1 0 30 no no Preprocessor1_Mo…

7 train/test split 0.749 0.251 34 no no Preprocessor1_Mo…

8 train/test split 1 0 35 no no Preprocessor1_Mo…

9 train/test split 1 0 43 no no Preprocessor1_Mo…

10 train/test split 1 0 52 no no Preprocessor1_Mo…

# … with 10,287 more rowsfinal_kknn_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% autoplot()

kknn_auc = final_kknn_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% mutate(model = "knn")model = KNeighborsClassifier()

param_grid = {'model__n_neighbors':np.arange(0,20,1)}

steps[-1] = ("model", model)

pipe = Pipeline(steps)

grid = GridSearchCV(pipe, param_grid, cv=10, scoring='roc_auc')

grid.fit(data_bank_marketing_train, y_train)GridSearchCV(cv=10,

estimator=Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()),

('zv', VarianceThreshold()),

('model', KNeighborsClassifier())]),

param_grid={'model__n_neighbors': array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16,

17, 18, 19])},

scoring='roc_auc')In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

GridSearchCV(cv=10,

estimator=Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()),

('zv', VarianceThreshold()),

('model', KNeighborsClassifier())]),

param_grid={'model__n_neighbors': array([ 0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16,

17, 18, 19])},

scoring='roc_auc')Pipeline(steps=[('dummy',

ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first',

sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)),

('normalize', MinMaxScaler()), ('zv', VarianceThreshold()),

('model', KNeighborsClassifier())])ColumnTransformer(remainder='passthrough',

transformers=[('dummy',

OneHotEncoder(drop='first', sparse=False),

Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object'))],

verbose_feature_names_out=False)Index(['job', 'marital', 'education', 'default', 'housing', 'loan', 'contact', 'month', 'day_of_week', 'poutcome'], dtype='object')

OneHotEncoder(drop='first', sparse=False)

['age', 'campaign', 'pdays', 'previous', 'emp.var.rate', 'cons.price.idx', 'cons.conf.idx', 'euribor3m', 'nr.employed']

passthrough

MinMaxScaler()

VarianceThreshold()

KNeighborsClassifier()

grid.best_params_{'model__n_neighbors': 19}fitted_model=grid.best_estimator_

score=grid.score(data_bank_marketing_test, y_test)

score0.7583868296985286yhat=grid.predict(data_bank_marketing_test)

roc_plot(data_bank_marketing_test, y_test, fitted_model, 'yes')0.7583868296985286

import NearestNeighborModels

KNNClassifier = @load KNNClassifier pkg=NearestNeighborModels verbosity=0NearestNeighborModels.KNNClassifier

model = Standardizer |> ContinuousEncoder |> KNNClassifier()ProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

knn_classifier = KNNClassifier(

K = 5,

algorithm = :kdtree,

metric = Distances.Euclidean(0.0),

leafsize = 10,

reorder = true,

weights = NearestNeighborModels.Uniform()),

cache = true)

mach = machine(model, X_train, y_train);

fit!(mach);

yhat=MLJ.predict(mach, X_test);

rep = report(mach);

print(

"Measurements:\n",

" brier loss: ", brier_loss(yhat,y_test) |> mean, "\n",

" auc: ", auc(yhat,y_test), "\n",

" accuracy: ", accuracy(mode.(yhat), y_test)

)Measurements:

brier loss: 0.1816056976367755

auc: 0.7262961939438142

accuracy: 0.8910650696018129

#doc("KNNClassifier", pkg="NearestNeighborModels")

Support Vector Machine

svm_spec = svm_rbf(cost = 1, margin = 0.1) %>%

set_mode("classification") %>%

set_engine("kernlab")

base_rec = recipe(y ~ ., data = data_bank_marketing_train) %>% step_rm(duration) %>%

step_zv(all_numeric_predictors()) %>%

step_normalize(all_numeric_predictors())

svm_rec = base_rec %>%

step_dummy(all_nominal_predictors())

svm_data = prep(svm_rec, data_bank_marketing_train) %>% bake(new_data = NULL)

svm_wrkflw = workflow() %>% add_model(svm_spec) %>% add_recipe(svm_rec)

svm_wrkflw══ Workflow ════════════════════════════════════════════════════════════════════

Preprocessor: Recipe

Model: svm_rbf()

── Preprocessor ────────────────────────────────────────────────────────────────

4 Recipe Steps

• step_rm()

• step_zv()

• step_normalize()

• step_dummy()

── Model ───────────────────────────────────────────────────────────────────────

Radial Basis Function Support Vector Machine Model Specification (classification)

Main Arguments:

cost = 1

margin = 0.1

Computational engine: kernlab grid_ctrl <-

control_grid (

save_pred = TRUE,

parallel_over = "everything",

save_workflow = TRUE

)

final_svm_fit = svm_wrkflw %>% fit(data=data_bank_marketing_train)

final_svm_pred = final_svm_fit %>% predict(data_bank_marketing_test, type = "prob")

final_svm_pred = final_svm_pred %>% cbind(data_bank_marketing_test %>% select(y))

final_svm_pred$y = as.factor(final_svm_pred$y)

final_svm_pred %>% roc_curve(y, .pred_no) %>% autoplot()

svm_auc = final_svm_pred %>% roc_curve(y, .pred_no) %>% mutate(model="svm")# Cross validation\ grid search is not used for SVC as it is too slow due to the 40K+ observations and 19 features.

model = SVC(kernel='rbf', C=1, gamma = 0.1, probability=True)

# Remove the previous model; the pipeline in this case is used only for data transformation and not model fitting

steps.pop()

# transform train data('model', KNeighborsClassifier())X_trans_train = pipe.fit_transform(data_bank_marketing_train, y_train)

# transform y

label_encoder = LabelEncoder()

y_trans_train = label_encoder.fit_transform(y_train)

y_trans_test = label_encoder.fit_transform(y_test)

# model needs to be fit first due to 'prefit' option used for CalibratedClassifierCV

model.fit(X_trans_train, y_trans_train)

# CalibratedClassifierCV is used to find probabilities, and not for cross validationSVC(C=1, gamma=0.1, probability=True)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

SVC(C=1, gamma=0.1, probability=True)

calibrated_clf = CalibratedClassifierCV(model, cv = 'prefit')

# fit again to find probabilities

calibrated_clf.fit(X_trans_train, y_trans_train)CalibratedClassifierCV(cv='prefit',

estimator=SVC(C=1, gamma=0.1, probability=True))In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

CalibratedClassifierCV(cv='prefit',

estimator=SVC(C=1, gamma=0.1, probability=True))SVC(C=1, gamma=0.1, probability=True)

SVC(C=1, gamma=0.1, probability=True)

calibrated_clf.predict_proba(X_trans_train)

# transform test dataarray([[0.9119843 , 0.0880157 ],

[0.9120593 , 0.0879407 ],

[0.91198241, 0.08801759],

...,

[0.91272997, 0.08727003],

[0.9137733 , 0.0862267 ],

[0.91701637, 0.08298363]])X_trans_test = pipe.fit_transform(data_bank_marketing_test, y_test)

yhat = calibrated_clf.predict(X_trans_test)

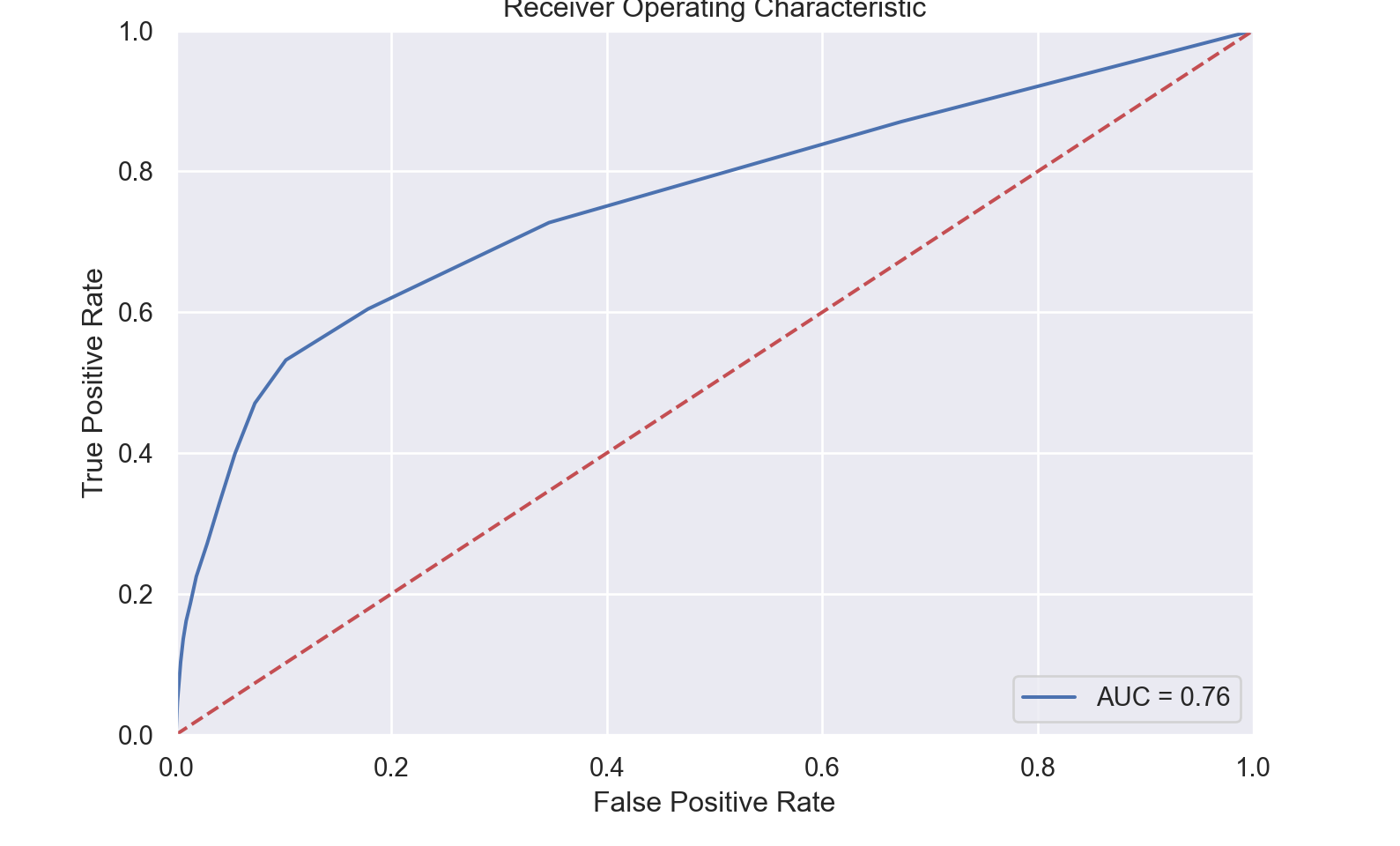

report=metrics.classification_report(y_trans_test,yhat)

print(report) precision recall f1-score support

0 0.91 0.99 0.94 9139

1 0.65 0.19 0.29 1158

accuracy 0.90 10297

macro avg 0.78 0.59 0.62 10297

weighted avg 0.88 0.90 0.87 10297roc_plot(X_trans_test, y_trans_test, model, 1)0.71219394910423

import LIBSVM

#doc("ProbabilisticSVC", pkg="LIBSVM")

ProbabilisticSVC = @load ProbabilisticSVC pkg=LIBSVM verbosity=0MLJLIBSVMInterface.ProbabilisticSVC

model = Standardizer |> ContinuousEncoder |> ProbabilisticSVC(kernel=LIBSVM.Kernel.RadialBasis, gamma = 0.1)ProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

probabilistic_svc = ProbabilisticSVC(

kernel = LIBSVM.Kernel.RadialBasis,

gamma = 0.1,

cost = 1.0,

cachesize = 200.0,

degree = 3,

coef0 = 0.0,

tolerance = 0.001,

shrinking = true),

cache = true)

mach = machine(model, X_train, y_train);

fit!(mach);

yhat=MLJ.predict(mach, X_test);

rep = report(mach);

print(

"Measurements:\n",

" brier loss: ", brier_loss(yhat,y_test) |> mean, "\n",

" auc: ", auc(yhat,y_test), "\n",

" accuracy: ", accuracy(mode.(yhat), y_test)

)Measurements:

brier loss: 0.16360023292036047

auc: 0.7202998911144449

accuracy: 0.901181612172224

XGBoost

xgboost_recipe =

recipe(formula = y ~ ., data = data_bank_marketing_train) %>%

step_rm(duration) %>%

## For modeling, it is preferred to encode qualitative data as factors

## (instead of character).

step_string2factor(one_of("job", "marital", "education", "default", "housing",

"loan", "contact", "month", "day_of_week", "poutcome", "y")) %>%

step_novel(all_nominal_predictors()) %>%

## This model requires the predictors to be numeric. The most common

## method to convert qualitative predictors to numeric is to create

## binary indicator variables (aka dummy variables) from these

## predictors. However, for this model, binary indicator variables can be

## made for each of the levels of the factors (known as 'one-hot

## encoding').

step_dummy(all_nominal_predictors(), one_hot = TRUE) %>%

step_zv(all_predictors())

xgboost_spec =

boost_tree(trees = tune(), tree_depth = tune(), learn_rate = tune(), loss_reduction = tune(), min_n = tune(), sample_size = tune()) %>%

set_mode("classification") %>%

set_engine("xgboost")

xgboost_workflow =

workflow() %>%

add_recipe(xgboost_recipe) %>%

add_model(xgboost_spec)

xgboost_param <- extract_parameter_set_dials(xgboost_spec)

set.seed(87274)

final_params <-

tibble(

trees = 1453,

tree_depth = 11,

learn_rate = 0.052975,

loss_reduction = 7.733554,

min_n = 26,

sample_size = 0.9654255

)

final_xgboost_wflow = xgboost_workflow %>% finalize_workflow(final_params)

final_xgboost_wflow══ Workflow ════════════════════════════════════════════════════════════════════

Preprocessor: Recipe

Model: boost_tree()

── Preprocessor ────────────────────────────────────────────────────────────────

5 Recipe Steps

• step_rm()

• step_string2factor()

• step_novel()

• step_dummy()

• step_zv()

── Model ───────────────────────────────────────────────────────────────────────

Boosted Tree Model Specification (classification)

Main Arguments:

trees = 1453

min_n = 26

tree_depth = 11

learn_rate = 0.052975

loss_reduction = 7.733554

sample_size = 0.9654255

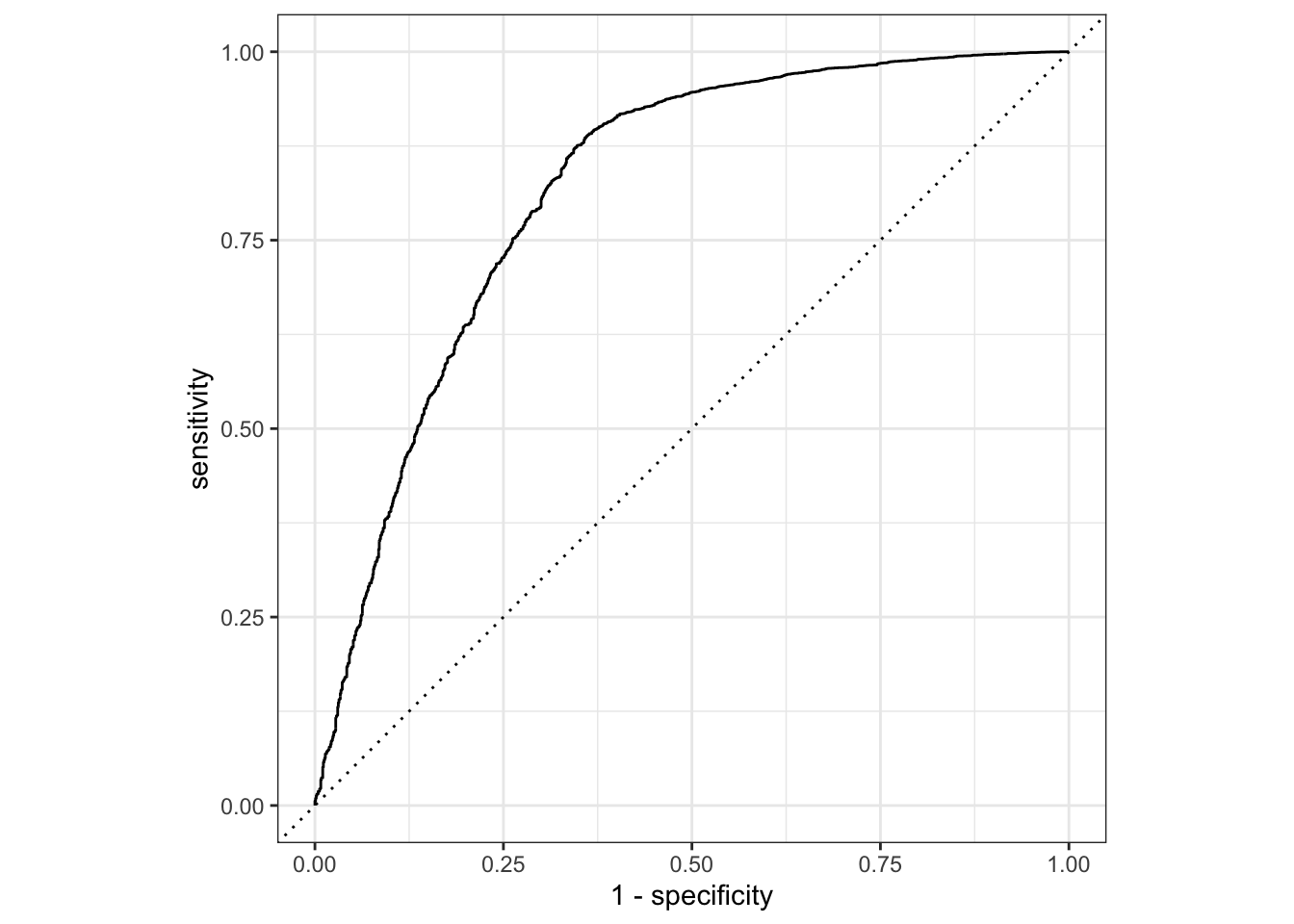

Computational engine: xgboost final_xgboost_fit = final_xgboost_wflow %>% last_fit(data_bank_marketing_split)

final_xgboost_fit %>% collect_metrics()# A tibble: 2 × 4

.metric .estimator .estimate .config

<chr> <chr> <dbl> <chr>

1 accuracy binary 0.901 Preprocessor1_Model1

2 roc_auc binary 0.816 Preprocessor1_Model1final_xgboost_fit %>% collect_predictions()# A tibble: 10,297 × 7

id .pred_no .pred_yes .row .pred_class y .config

<chr> <dbl> <dbl> <int> <fct> <fct> <chr>

1 train/test split 0.971 0.0286 7 no no Preprocessor1_Mo…

2 train/test split 0.973 0.0274 18 no no Preprocessor1_Mo…

3 train/test split 0.974 0.0257 21 no no Preprocessor1_Mo…

4 train/test split 0.978 0.0222 22 no no Preprocessor1_Mo…

5 train/test split 0.970 0.0305 24 no no Preprocessor1_Mo…

6 train/test split 0.979 0.0212 30 no no Preprocessor1_Mo…

7 train/test split 0.977 0.0230 34 no no Preprocessor1_Mo…

8 train/test split 0.976 0.0240 35 no no Preprocessor1_Mo…

9 train/test split 0.973 0.0267 43 no no Preprocessor1_Mo…

10 train/test split 0.979 0.0210 52 no no Preprocessor1_Mo…

# … with 10,287 more rowsfinal_xgboost_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% autoplot()

xgboost_auc = final_xgboost_fit %>% collect_predictions() %>% roc_curve(y, .pred_no) %>% mutate(model = "xgboost")

from sklearn.model_selection import StratifiedKFold

from xgboost import XGBClassifier

def grid_search_xgb(params, X, y, kfold, random=False):

xgb = XGBClassifier(booster='gbtree', objective='binary:logistic', random_state=2)

if random:

grid = RandomizedSearchCV(xgb, params, cv=kfold, n_iter=10, n_jobs=-1, scoring='roc_auc') #n_iter controls number of random combinations

else:

grid = GridSearchCV(xgb, params, cv=kfold,n_jobs=-1, scoring='roc_auc')

grid.fit(X, y)

print('Best params:', grid.best_params_)

print('Best score:', grid.best_score_)

#

#

st_Kfold = StratifiedKFold(n_splits=5, shuffle=True, random_state=2)

#

# #n_estimators is the number of trees trained, default is 100. 7 seems to be an optimum value.

# params={'n_estimators':[7,10]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #learning_rate shrinks the weights of trees for each round of boosting, default is 0.3. By lowering learning_rate, more trees are required to produce better scores. Lowering learning_rate prevents overfitting because the size of the weights carried forward is smaller. 0.05 seems to be an optimum value.

# params={'learning_rate':[0.01, 0.05, 0.075, 0.1, 0.2, 0.3, 0.4, 0.5]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #max_depth determines the length of the tree, equivalent to the number of rounds of splitting. default is 6. Limiting max_depth prevents overfitting because the individual trees can only grow as far as max_depth allows. 2 seems to be an optimum value.

# params={'max_depth':[1,2, 3, 5, 6, 8]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #gamma provides a threshold that nodes must surpass before making further splits according to the loss function, default is 0.There is no upper limit to the value of gamma. Anything over 10 is considered very high. Increasing gamma results in a more conservative model. 5 seems to be an optimum value.

# params={'gamma':[0, 0.1, 0.5, 1, 2, 5, 7]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #min_child_weight refers to the minimum sum of weights required for a node to split into a child. If the sum of the weights is less than the value of min_child_weight, no further splits are made.min_child_weight reduces overfitting by increasing its value. 4 seems to be an optimum value.

# params={'min_child_weight':[1, 2, 3, 4, 5]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #The subsample hyperparameter limits the percentage of training instances (rows) for each boosting round. Decreasing subsample from 100% reduces overfitting. 1 seems to be an optimum value:

# params={'subsample':[0.5, 0.7, 0.8, 0.9, 1]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

# #colsample_bytree randomly selects particular columnsaccording to the given percentage.colsample_bytree is useful for limiting the influence of columns and reducing variance. 0.7 seems to be an optimum value.

# params={'colsample_bytree':[0.5, 0.7, 0.8, 0.9,1]}

# grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

#

params={'n_estimators':[5,7,10,20,50],

'learning_rate': [0.05,0.1, 0.2, 0.3, 0.4, 0.5],

'max_depth': [2,4,6],

'gamma': [0.1,0.5,2, 5],

'min_child_weight': [3,4,5],

'subsample': [0.5,1],

'colsample_bytree': [0.5,0.7,1]}

# # ->grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold)

#

#

# #Output:

# #Best params: {'colsample_bytree': 0.7, 'gamma': 0.1, 'learning_rate': 0.1, 'max_depth': 6, 'min_child_weight': 4, 'n_estimators': 50, 'subsample': 1}

# #Best score: 0.800812151928098

#

#

params={'n_estimators':[20,50,75,100],

'learning_rate': [0.05,0.1, 0.15, 0.2],

'max_depth': [6,8,10],

'gamma': [0.1,0.2,0.3],

'min_child_weight': [3,4,5],

'subsample': [0.75,1],

'colsample_bytree': [0.7,0.8,1]}

#

# # ->grid_search_xgb(params, X_trans_train, y_trans_train, st_Kfold, random=True)

#

# # ->grid_search(params={'subsample':[0.5, 0.6, 0.7, 0.8, 0.9, 1],'min_child_weight':[1, 2, 3, 4, 5],'learning_rate':[0.1, 0.2, 0.3, 0.4, 0.5],'max_depth':[1, 2, 3, 4, 5], 'n_estimators':[2]})

# #Best params: {'subsample': 1, 'n_estimators': 75, 'min_child_weight': 3, 'max_depth': 8, 'learning_rate': 0.05, 'gamma': 0.1, 'colsample_bytree': 0.7}

# #Best score: 0.8013732623090342

#

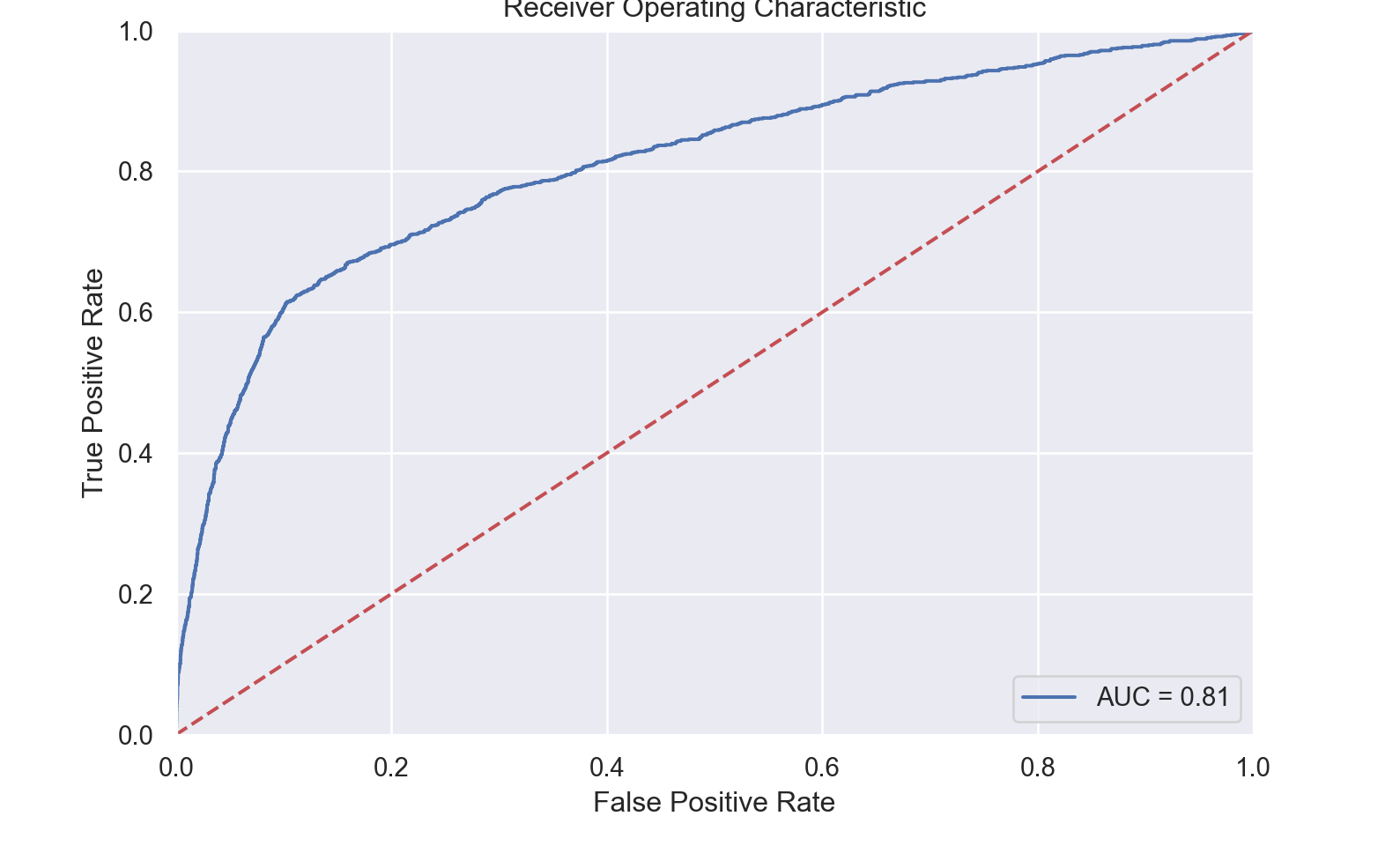

final_model = XGBClassifier(booster='gbtree',objective='binary:logistic', max_depth=8, learning_rate=0.05, n_estimators=75, subsample=1, min_child_weight=3, gamma=0.1, colsample_bytree=0.7, random_state=2, n_jobs=-1)

#

fitted_model=final_model.fit(X_trans_train, y_trans_train)

print ('ROC AUC Score',roc_plot(X_trans_test,y_trans_test, fitted_model, 1))ROC AUC Score 0.8105681566276057

XGBoostClassifier = @load XGBoostClassifier pkg=XGBoost verbosity=0MLJXGBoostInterface.XGBoostClassifier

model = Standardizer |> ContinuousEncoder |> XGBoostClassifierProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

xg_boost_classifier = XGBoostClassifier(

test = 1,

num_round = 100,

booster = "gbtree",

disable_default_eval_metric = 0,

eta = 0.3,

num_parallel_tree = 1,

gamma = 0.0,

max_depth = 6,

min_child_weight = 1.0,

max_delta_step = 0.0,

subsample = 1.0,

colsample_bytree = 1.0,

colsample_bylevel = 1.0,

colsample_bynode = 1.0,

lambda = 1.0,

alpha = 0.0,

tree_method = "auto",

sketch_eps = 0.03,

scale_pos_weight = 1.0,

updater = nothing,

refresh_leaf = 1,

process_type = "default",

grow_policy = "depthwise",

max_leaves = 0,

max_bin = 256,

predictor = "cpu_predictor",

sample_type = "uniform",

normalize_type = "tree",

rate_drop = 0.0,

one_drop = 0,

skip_drop = 0.0,

feature_selector = "cyclic",

top_k = 0,

tweedie_variance_power = 1.5,

objective = "automatic",

base_score = 0.5,

watchlist = nothing,

nthread = 1,

importance_type = "gain",

seed = nothing,

validate_parameters = false),

cache = true)show(model, 2)ProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

xg_boost_classifier = XGBoostClassifier(

test = 1,

num_round = 100,

booster = "gbtree",

disable_default_eval_metric = 0,

eta = 0.3,

num_parallel_tree = 1,

gamma = 0.0,

max_depth = 6,

min_child_weight = 1.0,

max_delta_step = 0.0,

subsample = 1.0,

colsample_bytree = 1.0,

colsample_bylevel = 1.0,

colsample_bynode = 1.0,

lambda = 1.0,

alpha = 0.0,

tree_method = "auto",

sketch_eps = 0.03,

scale_pos_weight = 1.0,

updater = nothing,

refresh_leaf = 1,

process_type = "default",

grow_policy = "depthwise",

max_leaves = 0,

max_bin = 256,

predictor = "cpu_predictor",

sample_type = "uniform",

normalize_type = "tree",

rate_drop = 0.0,

one_drop = 0,

skip_drop = 0.0,

feature_selector = "cyclic",

top_k = 0,

tweedie_variance_power = 1.5,

objective = "automatic",

base_score = 0.5,

watchlist = nothing,

nthread = 1,

importance_type = "gain",

seed = nothing,

validate_parameters = false),

cache = true)#models("xgboost")

XGBoostClassifier = @load XGBoostClassifier pkg=XGBoostimport MLJXGBoostInterface ✔MLJXGBoostInterface.XGBoostClassifier

model = Standardizer |> ContinuousEncoder |> XGBoostClassifierProbabilisticPipeline(

standardizer = Standardizer(

features = Symbol[],

ignore = false,

ordered_factor = false,

count = false),

continuous_encoder = ContinuousEncoder(

drop_last = false,

one_hot_ordered_factors = false),

xg_boost_classifier = XGBoostClassifier(

test = 1,

num_round = 100,

booster = "gbtree",

disable_default_eval_metric = 0,